Traders and economists often say the most expensive words in the English language are “this time is different.” These words often explain bubbles and mistakes. In 1999, traders believed that because of the Internet, “this time is different.” In 1929, traders believed that because of new technologies like radio and the automobile, “this time is different.” The same was true of canals in the 1790s, railroads in the 1840s and countless other manias.

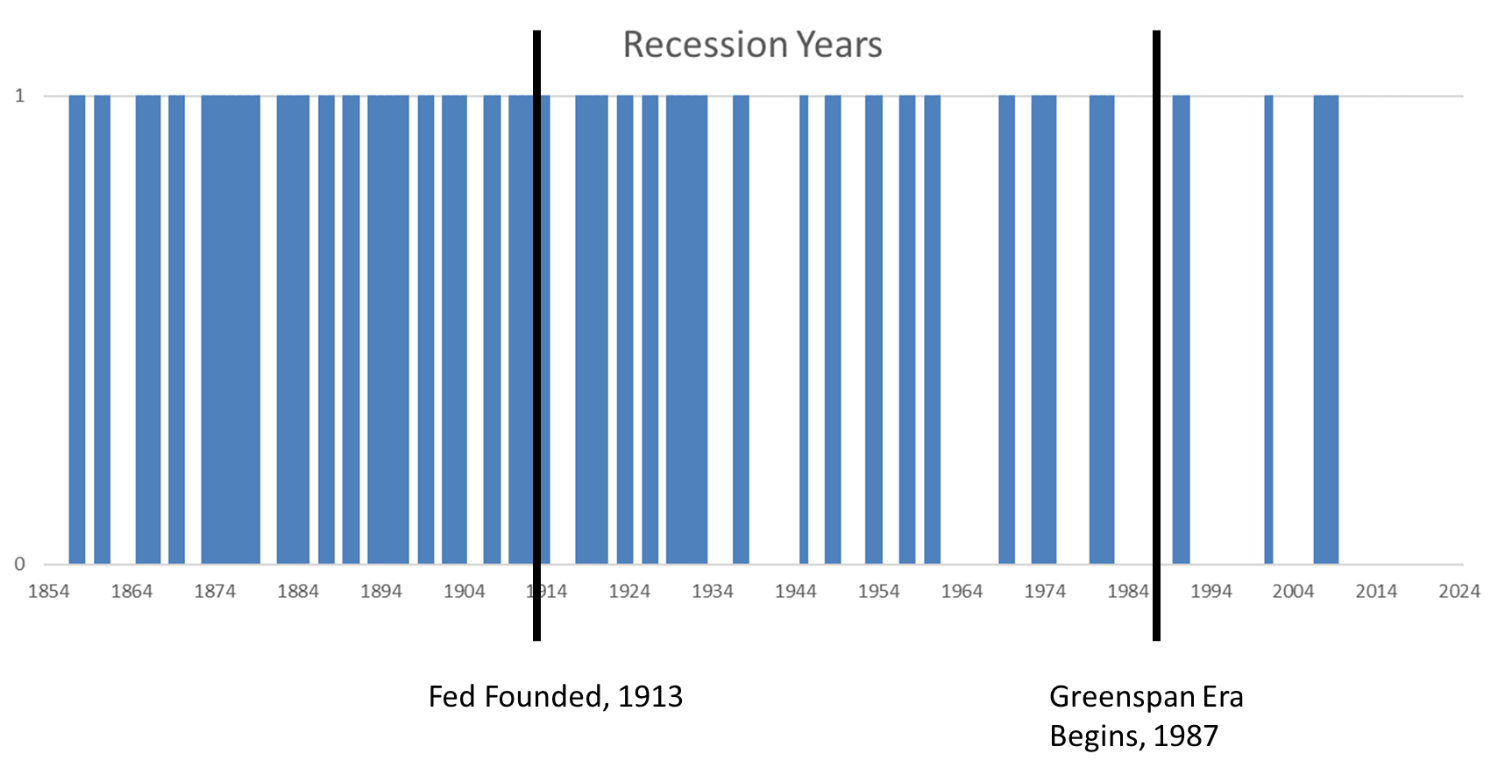

After these bubbles, there was always a crash. That’s when economists like to say that “this time is never different.” But sometimes, like now, there are noticeable differences from the past, which accumulate over time. The chart below shows that recessions are now rather rare, although they were common in the 19th century. In the chart, a blue bar indicates a recession occurred that year.

(Source: the National Bureau of Economic Research)

The National Bureau of Economic Research reports on recessions going back to 1854. There were recessions in at least one month in 65% of all years in the 19th century. That number fell to just 22% in the 21st century. Maybe this time is different.

Politicians realized they needed to do something after the Panic of 1907. That year, stock prices fell 50%. In that recession, the economy contracted by 11%, and unemployment more than doubled, jumping from under 3% to 8%. For comparison, stock prices fell about 55% in the most recent recession, the economy contracted by 4.3% and unemployment doubled to a high of 10%.

After the Panic of 1907, Congress passed the Federal Reserve Act in 1913. The Fed took time to find its footing. Its policies probably made the 1929 downturn even worse.

The Fed took about 70 years to reach its goals. There was some progress, and the frequency of recession years fell to 46% over that time. But the Fed really made its impact after 1987, when Alan Greenspan became chairman. Greenspan drove the Fed to a more active role in the economy, and recession frequency fell to 19% since Greenspan changed course.

Partly because of Greenspan, this time is different. New technology, like the Internet of Things, is part of the story. But the bigger story might be that Fed policies have dampened the business cycle and reduced the number of recessions. These policies also dampen recoveries, however.

Investment rules have changed. In the future, we should expect few bear markets and weak recoveries. This will prevent the economy from overheating, which means inflation and interest rates should stay low.

It’s a new era for the economy. Investors need to understand that and adapt to what the future holds.

Regards,

Michael Carr, CMT

Editor, Peak Velocity Trader