When you hear a stock is up an enormous amount in a short period, your gut tells you it’s not going to last long.

It seems overbought.

Investors are going to be looking to sell and take profits.

After it dips, maybe then you’ll buy some.

Even Wall Street sees it this way.

When a stock rallies past these analysts’ price targets, or to a point that feels too far too fast, they list it as a hold.

They don’t tell you to buy more and jump in with both feet.

But sometimes your gut is wrong. And Wall Street is wrong. This creates one of our favorite things in Winning Investor Daily … a mispricing.

You see, strong stocks, the ones that can make a difference in your portfolio, often see those kinds of continuous moves higher. But Wall Street just leaves them on hold.

Unique companies with massive growth potential don’t tend to fall much after a massive run, such as 160% in just nine months. That means that larger companies with big run-ups are likely to keep heading higher while the analysts on Wall Street ignore them.

This gives us an opportunity.

Better yet, after a sell-off in March, the stock we’re looking at today has soared nearly 400% to hit new all-time highs.

I’m talking about Square Inc. (NYSE: SQ), the payment processing company.

In my latest Bank It or Tank It video, I’m breaking down everything you need to know about this stock, including what its recent rally means for the coming months.

A lot of people own shares of this company or have it on their radar.

I’ll tell you exactly what to expect from Square today.

Click below to watch my latest video:

Bank It or Tank It: Square Inc. Stock Analysis

- Square is a popular stock on fire this year.

- It’s ripped higher and boasts phenomenal results since the coronavirus-related crash.

- Take a look at the fundamentals, sentiment, and the technicals to see if you should “Bank” or “Tank” Square.

This week, we’re covering a very popular stock. One that has been shooting sky-high over the last couple of months: Square (NYSE: SQ), the payment giant.

We’re going to dive into everything you need to know about this stock today by taking a look at the fundamentals, sentiment, and the technicals to figure out if this is a stock that you want to bank on going higher over the next 12 months, or if it’s one that’s going to be on my Tank It list for today.

This stock has been on fire here in 2020. It’s up over 180%.

And it’s up 350% since the coronavirus pandemic-related crash earlier in the year. So, this is a stock that’s just been ripping higher and had phenomenal results for the third quarter of the year. Something to keep in mind though, Square’s revenue surged — up about 140% just from a year ago.

Year over year, it had a massive jump. And that really had to do with more trading volume in bitcoin. But it only delivers a little bit of profit, which was up 34% over the same time period.

When you strip out the bitcoin trading profits, this is a company that is still seeing growth, but not at that incredible rate.

Revenues from its gross payment volume from merchants rose just 9%, slightly below expectations due to a hit on restaurants and small businesses – its main merchants.

The company’s seeing growth in its Cash App, which is more consumer to consumer. And that’s really helped Square smooth this process out going through a pandemic.

That’s also great news for the company, because it’s going through a period that is putting a lot of small businesses underwater. Square is by no means a small business anymore, but when you look at some of its competitors, it’s still a relatively small company.

But Square is seeing strength by being innovative, getting in on different industries by allowing bitcoin trading, and skimming a little bit of profit off of that.

Square is out front in cutting-edge technology, using some of the latest financial instruments to make the best of its platform.

Let’s take a look at the fundamentals…

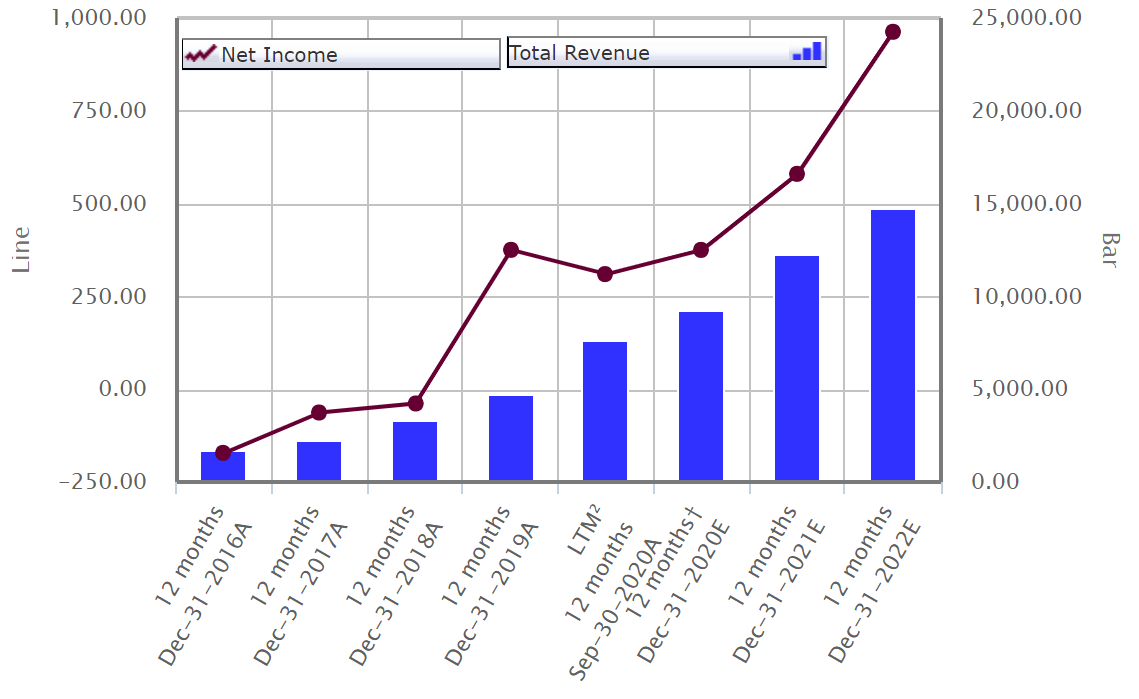

Square — Key Stats

Pulling up the key stats for Square, total revenues are the blue bars on the chart (right-hand side); and the line on the graph is net income (left-hand side).

This chart shows its performance since 2016, and how the company’s expected to perform in 2021 and 2022.

You can see that Square has a little bit of a dip here in 2020, ever so slight, for actual earnings for September 30. But 2020 expected for December is a little higher. Then, it’s off to the races in 2021 and 2022 expectations for earnings.

What I like about seeing this is that there’s no massive dip here. It’s just a slight pullback in earnings and we don’t really see it reflected in the revenues at all.

The revenues are on a steady climb higher.

And when you look at the third-quarter results, the revenues that it’s seeing in its bitcoin department is helping to keep that expected smooth path higher. Because when you strip out the revenues from bitcoin, Square is seeing much slower growth.

Again, this revenue doesn’t translate into as much earnings, but it is making its financial statements much nicer.

When you look at what happened in 2020, considering Square is a platform for payments in small businesses, this is a company that’s really thriving during an extremely difficult time period.

And Square is doing well, partly because of these other areas that it’s in.

So this chart is very promising to me.

I like that we’re seeing a steady uptrend in net income and in revenues. As revenues continue to climb, it’s going to pull net income higher as it continues to focus more on being profitable, instead of just finding more sales.

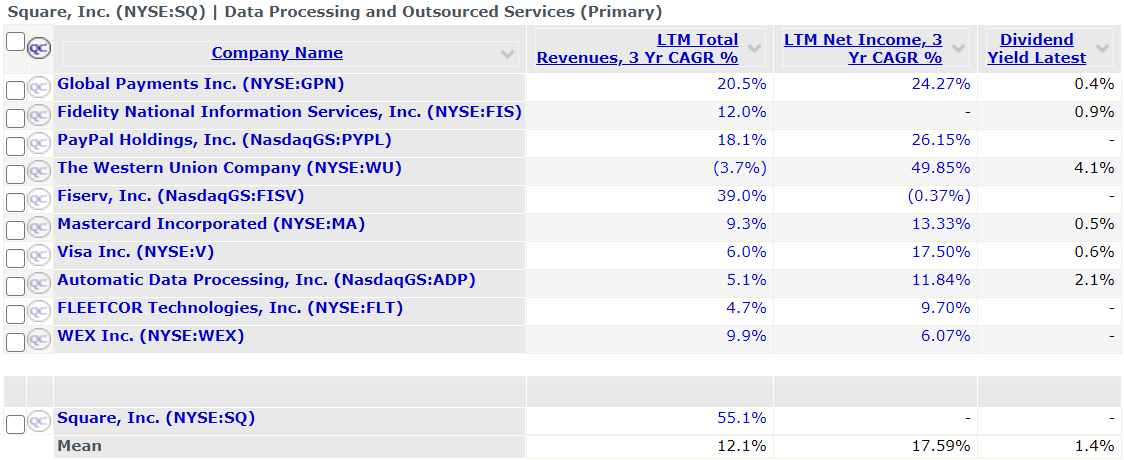

Comparable Analysis

Now, let’s do a quick comparable analysis to some of the other payment companies in the industry, and we want to see how Square matches up.

Here’s a chart with some of these bigger companies that are in the data processing and payments industry. The main one to point out is going to be: PayPal (Nasdaq: PYPL). I think that’s Square’s biggest direct competitor, because PayPal is heavily involved with the consumer aspect of this industry.

My wife and I use PayPal when we want to send money to friends and family. It’s the easiest thing to do. All of our friends and family have PayPal, but that’s the area that Square’s just starting to dip its toes into with Cash App.

Square is getting more involved in direct deposits and person-to-person payments, for more ease, providing another growth avenue. On the payment side, where small businesses or restaurants accept your payments on mobile devices, like an iPad, Square’s competing with Mastercard and Visa, because it’s trying to work its way into all these platforms and disrupt the payment industry.

With Cash App, Square essentially has its own card it collects fees from, too, even though Visa is the brand on it.

Look at how massive those companies are: $451 billion for Visa, $334 billion for Mastercard, and even $225 billion for PayPal.

Square, is just an $80 billion company. It’s very small compared to the giants in the industry. And that’s really where it’s targeting. It’s a disruptor with a lot of clients at this point, coming in and creating new products.

Small businesses were hurt during the pandemic. But they’re going to bounce back, and they’re going to continue to thrive, build more clients, and expand their platforms even more in the coming year.

So, the fact that Square is a smaller company just means there’s a lot more growth to be had … even after the 400% rally that we’ve seen since the bottom during the pandemic-induced sell-off.

When you look at short interest, this just gives us an idea of how many people are looking to short their shares. For Square, 5.7% of total shares outstanding are people betting on the stock to go lower.

The only company on here that’s higher is Western Union. And its whole business model was getting completely disrupted by PayPal and Square. So, that’s a company that’s really falling behind and seeing big short interest.

But with PayPal, Mastercard and Visa, there aren’t many people looking to short those stocks because they’re already large and established. Square is borderline. It’s definitely a growing company becoming very large that hasn’t quite gotten over the hump yet.

And when you include the fact that it’s a smaller company with this enormous growth over the last couple of years, that’s why we’re seeing a higher percentage of shares being sold short at this time.

The price to earnings ratio is 271 times earnings for Square. And that’s enormous. It’s the highest on the list.

When you look at PayPal, it’s at 72 times earnings, which is extremely high for a large stock like that. But even Mastercard and Visa are still 50 and 43 times earnings. So, this is an industry that’s generating high price-to-earnings ratios, but Square takes the cake.

It’s a little alarming, which is why we’re seeing a higher short-interest ratio. But when you look at the market cap, it’s still a small company in this industry with massive growth potential. So that 271 times price-to-earnings ratio is going to change. Square is just now starting to find its profitability.

As it becomes more profitable in the coming years, that price-to-earnings ratio is going to get trimmed lower as it finds some stability and a nice profit margin to continue to ride from there.

Let’s flip over, and we’re going to take a look at total revenues, the compound average annual growth rate over the last three years, and net income.

Square only has total revenues at 55%. That means over the last three years, it’s averaged a 55% growth rate each and every single year. And its net income was negative. But you can see that its revenue growth is the highest on the chart. It crushes, PayPal, Visa, and Mastercard.

Net income doesn’t show up, because Square is still a younger company, but I love that revenues are growing at a very fast rate. The dividend yield shows that PayPal is a large-cap stock, but it doesn’t pay dividends yet.

Mastercard, Visa and Western Union got so big that their growth slowed, and they turned to dividends to try to please investors. Once you turn it into income, you’re turning away from the growth model.

Right now, Square is fully invested in finding growth. And that’s going to benefit the stock over the next several years as it continues to find innovative industries to dive into and find more profit opportunities.

Analyst Rating

Now, I always like to look at the analyst community and see what they have the stock rated.

Right now, according to S&P Capital IQ, there are 36 analysts that cover the stock, and overall, the recommendation is a whole 2.31.

This just dips into the outperform rating, as anything at 2.5 or above falls into a hold. So it’s not a strong buy on their list and once we take a look at this chart and you see the stock, you know somebody should be fired over having this company listed near a hold.

Since this is an average out of 36, that means about half of these analysts actually have the stock at a worse rating than 2.31. And just the way it’s been ripping higher, if that was your job, and this is how you rated the stock, you clearly missed it, and you should not be covering this company.

So on the sentiment aspect, it’s a slight buy right now, but the stock is ripping higher. So that just tells you that Wall Street was behind the curve a bit on this company.

The Technicals

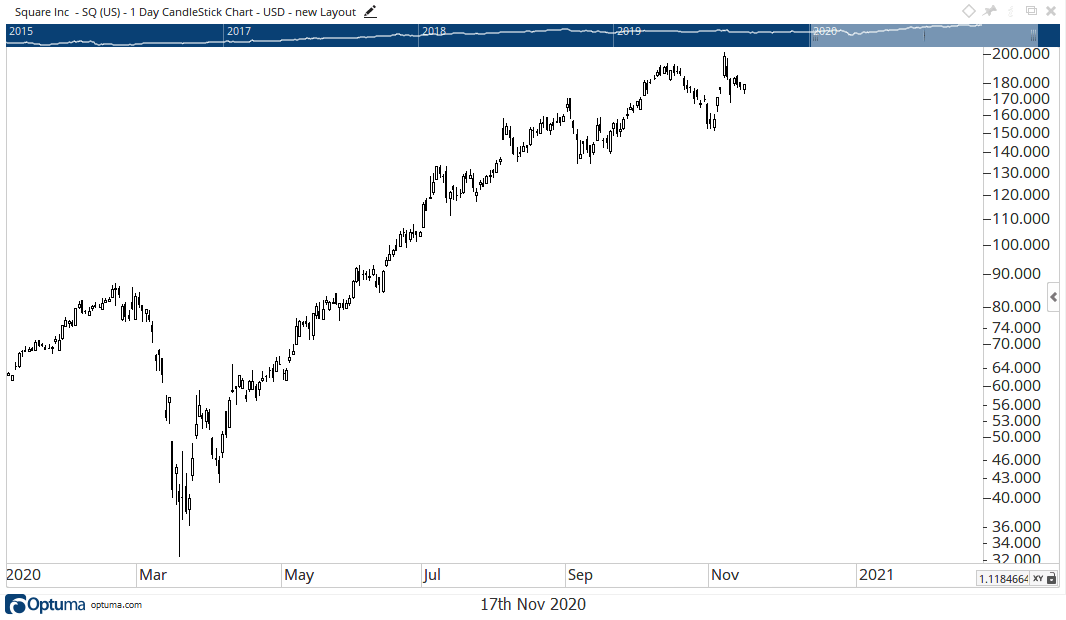

We’ll take a look at Square’s share prices, just in 2020. This is the year-to-date price chart and it shows the massive rally the stock has seen this year – despite the pandemic.

Shares are up 180% and that includes a 50% crash in March.

From the lows, shares have rallied more than 400%, those are Tesla-like numbers. You just don’t see stocks surge that much on any given year. But Square did in an extremely volatile market.

Part of that is bitcoin, and some of that is hype. But just because of the fact that Square has bitcoin, it’s seeing more growth in its Cash App. And that’s what’s helping it during this volatile period in the market.

It’s not having to rely so much on cash flows from businesses. It’s consumers are using the Cash App, using their cards for spending and sharing money and collecting fees that way.

To keep it simple, what I like about this chart is that the stock is making higher highs and higher lows – the No. 1 indicator of an uptrend.

At this point, nothing else matters. The stock is heading higher and we can expect it to do so until the rally begins to break down. It’s that simple.

Thanks to the massive run that we’ve seen in the stock and how shares have just ripped higher, this stock is on my Bank It list.

As long as this stock is in an uptrend and growing revenues at this incredible pace, how can you bet against it? Shares are set to march higher from here.

Triple-Digit Gains Almost Every Month

It’s rare to find a stock that moves nearly 400% in six months. Especially when it’s one the size of Square.

But, when it comes to trading options, you can spot many 100%, 200% or even 400% moves every year.

That’s why options are my favorite way to trade in the market.

I use them to find triple-digit gains — at a rate of almost ten per year. That’s nearly once every month … and practically impossible when trading stocks. But, with options, gains like this are nearly as common as a full moon.

I know options can be overwhelming to beginners.

New lingo, broker limits and a different risk/reward profile compared to stocks… It can be a lot of information.

A lot of investors simply aren’t comfortable with them.

Because of all this, I’ve also started a new weekly newsletter. I want to walk you through everything there is to know about options.

Every Friday, we’ll dive into option concepts to reveal how simple they are to use. At the end of the day, my goal is to make sure you can take advantage of the gains they unlock in the stock market.

This isn’t another sales pitch in your inbox, this is just straightforward options education.

To get it, all you have to do is sign up for my Weekly Options Corner.

It comes at no cost to you. The sole purpose of it is to allow everyone who wants to trade options to get the knowledge and confidence they need to do so.

Click here to join my Weekly Options Corner and master the trading of options.

Regards,

Chad Shoop, CMT

Editor, Quick Hit Profits