Many investors are worried about inflation.

But I’m concerned about a much deeper trend with serious long-term implications.

It stretches all the way back to the beginning of COVID-19’s supply chain disruptions, a “Bullwhip Effect” that could rip through retailers and portfolios. And today, I’m showing you how you can avoid it …

Click here to watch this week’s video or click on the image below:

Transcript

Hello everyone. It’s Ted Bauman here today, editor of Big Picture Big Profits and of The Bauman Letter. I’m not in my office today. I’m actually down near our head office in Florida. I’m doing some special filming today. Today, I want to talk about the microeconomics of the retail sector and why that could lead to a very surprising outcome.

In the next couple of months. Something that is counterintuitive, something that could actually upend a lot of what’s going on in the policy world with respect to interest rates, and that is inflation. Inflation, at least at the retail level could be set to reverse dramatically. And here’s why.

Let’s talk about something called the bull whip effect. It’s something that retail purchasing managers know all about work like this. When there’s a drop in customer demand retailers under stock. They don’t keep as much stuff in stock as they normally do, because remember carrying stuff in stock is costly. That means that you’ve got capital that could be doing something else that is being tied up in a warehouse. So it’s effectively losing money.

The second step is that when wholesalers see that retailers are slowing down their purchases because of slow consumer demand, they under stock themselves, right? In other words, they don’t keep as much in stock. So the wholesalers also cut back on their purchasing. And finally, when manufacturers get those market signals from wholesalers, they cut back production.

Now, eventually the reverse occurs. Eventually consumer demand comes back and retailers quickly order more goods. But the problem is that wholesalers and producers don’t have those goods in stock. They maybe don’t have the raw materials even to make them, so you get shortages. That leads to price increases.

Eventually production will ramp up to levels that actually exceed consumer demand. And you end up with an oversupply. That’s what’s done as the bull whip. You start with an overshoot in one direction and you end up with an overshoot in another direction. Now these violent swings and the availability of goods lead to pretty dramatic changes in price levels. Because retailers typically will increase prices in times of shortage and decreased them in times of oversupply.

Now, what happened during COVID? Well, first thing happened was that supply chains from Asia were cut. We remember old pictures of all the ships out there in off of Long Beach and Los Angeles waiting to get into the country. This was partly a consequence of the over-ordering that happened among retailers in the Western markets of the United States and Europe. Because they immediately started putting in orders for more inventory thinking, well if there’s going to be shortages, I want to get to the head of the queue.

Now, so they ordered a whole lot of stuff. That led to basically a pipeline of supply, which built up. And we had lockdowns. Now, that led to a drawdown of inventories as people were staying at home, but they were buying stuff to kit out maybe their new work from home gear or whatever they were doing. But in both cases, you end up with a scenario where people rapidly emptied the shelves. But purchasing managers put a lot of stuff on order that couldn’t be supplied right away.

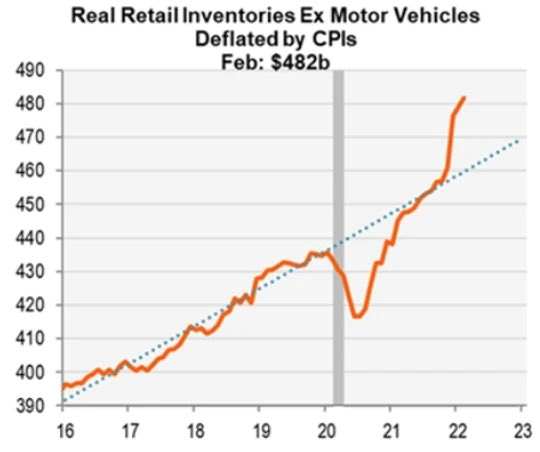

Now, when that happens, you end up with a scenario where suddenly you get a change in inventories that can lead to a dramatic change in prices. Here is a chart of retail inventories without motor vehicles that are adjusted for inflation:

And what it shows you is that retail inventories were basically changing along with economic growth and population growth and demand up until COVID. All of a sudden, boom, they fell dramatically. They gradually recovered, but then they overshot.

So what we’re seeing right now is a scenario where a lot of retailers are in the second half of the bull whip effect. Now, what that means for us in practice is that although we saw dramatic price increases in a lot of consumer sectors during 2021, particularly starting in May when the first half of the bull whip effect happened. Now, we are rapidly moving into the second phase. And that means that plunging or that you’re getting basically a change in retailer strategies towards their inventory.

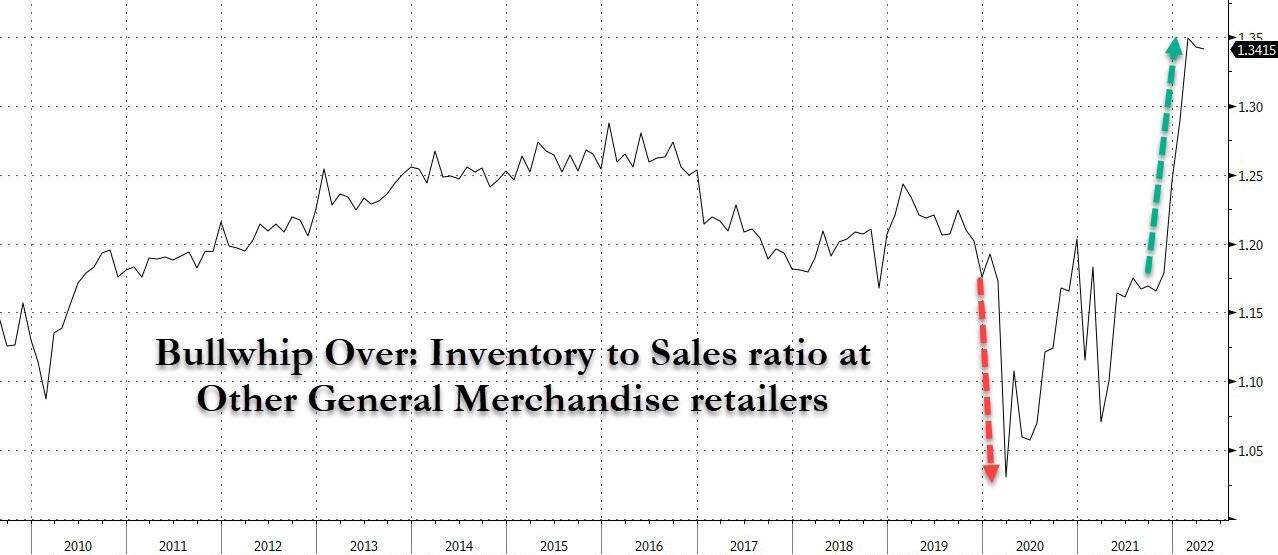

Now, one of the things to consider is what’s called the inventory to sales ratio. Now that’s an important metric for any retail company, like a Walmart or a Target. And the idea there is that you want to carefully manage the ratio between your inventory and your sales. Because if it gets too high, that means you’re looking at an economic cost by carrying all that inventory. So in order to target getting your inventory to sales ratio back to the normal level, you then need to find a way to liquidate a lot of that inventory.

So the bottom line message here is that we had the first half of the bull whip effect, which was a sudden shortage of goods leading to over ordering, which then led to a dramatic oversupply of good, which then leads to an excessive inventory to sales ratios. Now, we can see this in terms of the leading indicator, which is often transports. When you see a decline in transport stocks, you just see a decline in shipping activity. That means that retailers are starting to cut back their orders.

Here’s a chart that shows ships at anchor in the approaches to Southern California’s major ports:

And you can see that starting in January this year, it’s fallen precipitously. It’s not quite back to where it was before COVID, but we are seeing a dramatic drop in shipping. And that’s an important factor. The next chart shows the inventory-to-sales ratio, which is the second clear indicator of what’s happening:

The inventory to sales ratio is normally in a range of about 1.2 to 1.25. It fell dramatically during the first phase of COVID. But look what’s happened now, it’s risen far beyond the normal level. Now, what that means is that we can expect retailers to start liquidating those inventories through major discounting programs to burn that inventory off as quickly as they can.

In fact, what some people are saying is we’re about to see the mother of all liquidation sales as these big retailers have to unload this stuff. Because remember of the carrying cost of inventory is an economic cost. There’s the opportunity cost of keeping inventory on your books. I mean, basically that money could be doing something else. All that lost interest income from having them in the bank or whatever else is an economic cost.

It also stops you from buying new inventory. You can’t stock up on winter goods if your warehouses and your shelves are crowded with summer goods. So the first thing that we’ve seen as a symptom of this is a crashing of the stock prices of freight companies. You see truckers and railroads all seeing their freight or their share prices fall dramatically as an indication that shipments of goods to retailers are actually moving into reverse.

Now that’s not so much the case for commodities, things like agricultural commodities, industrial metals, ores and things like that because that bull whip effect takes a lot longer. But we will eventually see something similar happening.

Now, the key thing here is that if we do see an across the board attempt to reduce inventories as the second half of the bull whip effect, what we’re going to see is a dramatic fall in prices. We’re going to see sales all over the place as these retailers try to reduce their inventory to sales ratio through a de-stocking.

Now, the chances are that the scale of this will be far beyond anything that we’ve seen in the past. Just like everything has been amplified by COVID, we will also see this bull whip effect amplified. Now, the big difference from an investment perspective comes into looking how this affects the quarterly reports of big retailers.

We know that big retailers have been hammered recently by rising input costs by the fact that what they spent on those inventories led to a squeeze on their margins in the last quarter of last year, which has led to a big fall in their share prices. Both Walmart and Target suffered terribly, double digit drops in their share prices.

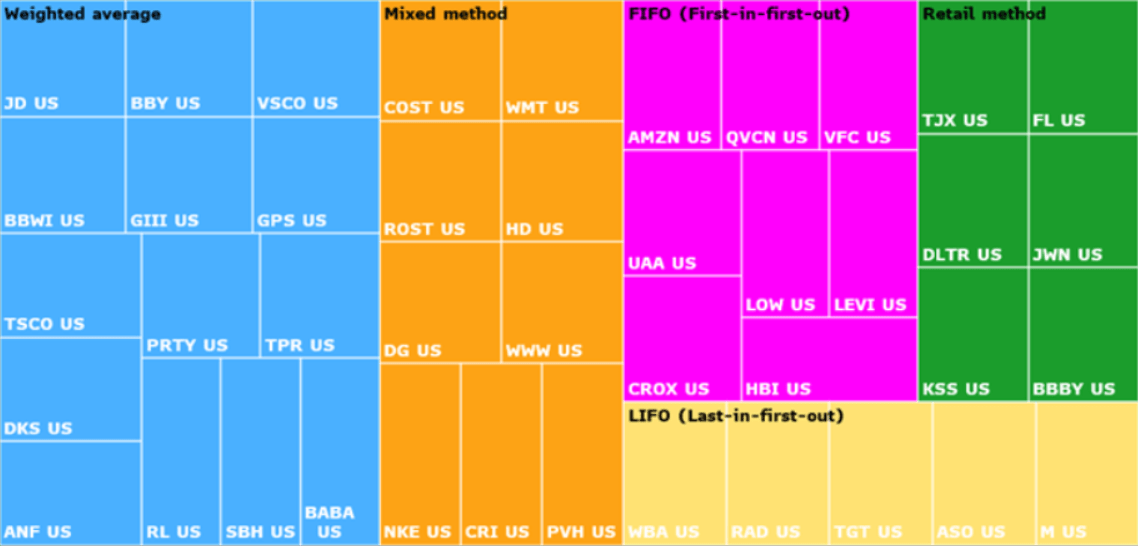

The thing is though that there are different ways to account for that inventory, depends on your accounting protocols. Something that companies adopt formally. In other words, once they adopt on an accounting protocol for inventory, they’re basically stuck with it until they change it.

There are three ways to do it. The one is called last in first out. Now in that method that assumes that the retailers draw on their newer inventory first. So the cost of the newer goods that they brought in are the first to be expense as cost of good sold. So other things being equal, if the stuff that came into Walmart and Target was the high price stuff, the stuff whose wholesale prices went up because of COVID shortages, that means that their margins are going to get even more squeezed than companies who do the opposite.

That’s first in, first out. That assumes that retailers draw on older inventory before tapping the new stuff. So that means that older goods for which they might have paid lower prices, get expensed before the newer goods that they bought at higher prices. That means that on balance, their margins get squeezed less. And that means that their quarterly reporting looks better. And so their stock price doesn’t get hit as much.

Now, there are some companies that use an average cost method or method rather, and that uses a weighted average of all inventory purchase. And that kind of nets it all out. Now, here’s a chart that shows the companies that tend to use, or that are committed to use the different types of retail management strategies:

But the critical thing here is that a lot of companies, particularly Target are committed to using the last in first out method, which accounts for the dramatic hit that they took on the quarter. Because basically they’re committed to an accounting method that forces them to expense the highest price inputs goods that they got.

Now, other companies like Walmart on the other hand, do the opposite. They expense the stuff, the oldest inventory that they have in stock, which makes their margins not look so bad. Now, the whole point of all of this is twofold. The first is that we are about to see, I think, a dramatic reversal in retail inflation. It won’t be across the board. There are still some things that are going to be more expensive, particularly food stuffs because of the impact on global markets of the war in Ukraine.

But ordinary retail goods, the kind of clothing, household items, a lot of non-food staple goods, those things are going to start falling in price quite dramatically. And that’s going to lead to a pullback in CPI. Now that’s going to lead to the second effect, which is that some companies are going to show better quarterly results in the next quarter than they did in the first quarter. Because the cost of their inventories are going to be falling as supply chains unclog.

But those that are committed to a last in first out approach are still going to probably have squeeze margins next reporting quarter because of that accounting protocol. So if you can figure out which companies use which protocol, you can short the stocks of those that are likely to continue to see a squeeze. Because they expense the most recently bought stuff, the stuff at higher prices first. And you could short those stocks around the time of their, or even use options, put options against them because they are likely to see another quarter of margin compression because they’re committed to expensing that more expensive stuff.

The other hand, companies that do the opposite are likely to do better. So maybe buy and call options on those stocks would be an important consideration. So there’s an options play there if you dig into the way that different retailers account for their sales. The last thing of course is that this could throw a spanner into the feds plan.

If we see a big pullback in retail inflation towards the end of this year, it could lead to a pause or a slowdown in interest rate hikes, which would be really good for the market. Because the market still has the muscle memory of essentially relying on low federal reserve interest rates as a justification for momentum and for risk on attitude. If that shifts, even if it’s just a temporary shift or a shift that’s driven by different factors like the inventory stuff I’m talking about, that could still lead to a brief mini boom in the stock market.

So the message here today is if you look under the hood, things are always more complicated than they appear. And that’s where the opportunities arise. So have a look at how those retailers deal with their inventories. Get ready for the next quarter reporting. And get out your options trades, you might be able to make some money. This is Ted Bauman signing off. Next week I’ll be reporting to you from Cape Town, South Africa, where I will be for the next two months. Take care.

Kind regards,

Ted Bauman

Editor, The Bauman Letter