This week, we received an email with an excellent question:

Hello Chad, Mike, and everyone else,

I’ve been really enjoying True Options Masters. It has taught me some valuable ideas as I continue learning about options.

One thing I’m curious about, and think may be an interesting topic, would be to understand why some of my calls (more than 30 days out) are posting gains while the stock is in the red that day, and vice versa (negative gains but stock is in the green).

I know there so many different factors that play into the price of an option, but I thought time and price were the major components.

Thank y’all for all y’all do!

— John B.

I appreciate your question, John. And everyone else’s.

We try to answer every question in our mailbag sections when we get a good batch, and utilize key questions like these in our daily newsletters.

This email is an example of why we need your questions. We are engrossed in the markets all day and forget that not everyone is as familiar with markets as we are. As a result, we can take certain aspects of option trading, like pricing, for granted.

Options pricing is definitely a topic we haven’t covered in detail. So that’s what we’ll do today…

The price of an option does depend upon the price of the underlying stock, and the amount of time before the option expires.

But the most important factor in the pricing models is the implied volatility of the stock.

Implied volatility is calculated based on the recent price action in a stock. Technically, it shows how large a price move is expected in the stock before the option expires.

However, volatility changes with every new trade. So the actual price move is rarely equal to the calculated value.

But even though the calculation isn’t accurate, it is a factor in the price models, and it does determine an option’s price.

These pricing models are complex, and I don’t want to overwhelm you with the math involved.

So to explain how the factors affect an options price, I’ll summarize each one’s impact.

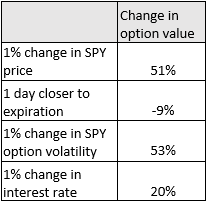

I analyzed an option in SPDR S&P 500 ETF (NYSE: SPY). It’s an at-the-money call expiring in one month, the $441 September 6 call to be precise:

The values shown assume that all other factors remain the same — that is, the price rises 1% while volatility remains unchanged.

That is unlikely to be the case since volatility will change as prices change. But I used this simple approach to highlight two important points.

One is that, for this option, the most important factor is the change in volatility. That is almost always the case. Price is the second most important factor. Time is a relatively minor factor.

The second is that interest rates are an important but often overlooked factor. If the Federal Reserve increases rates, the value of options will experience large changes. This change will happen the day the Fed announces the change.

Now, to answer your question, John…

The reason your call options are gaining while the value of the underlying security is falling, is likely due to the volatility that security is experiencing. When stocks are volatile, this increases the amount option buyers are willing to pay for the ability to buy the stock at certain prices. And as we see in the table above, volatility has a significant impact on options pricing.

Options prices are tricky to understand. And, for the most part, there is no need for most traders to dig into this arcane financial theory. Chad and I do this for you.

We will also explain more about these kinds of concepts in upcoming issues.

Regards,

Michael Carr

Editor, One Trade