Imagine that the value of your stock portfolio and your home both drop by 30%.

Would you spend less money?

The technocrats whose decisions shape the stock and housing markets think so.

The theory of the “wealth effect” says that people feel more financially secure when asset values are rising. That makes them more likely to spend.

Ergo, if you want people to spend less, asset prices must fall.

That’s a risky proposition.

But with inflation running at the hottest pace in four decades — and with the gridlocked federal government about as effective as a wet paper towel — the Federal Reserve is taking that risk.

As I’ll show you in just a moment, this gamble could have devastating consequences for Americans’ hard-earned wealth. But you don’t have to take it on the chin.

Here’s how to make your wealth increase … even if the Fed does its worst.

Fixing a Fragile Economy With a Hammer

Prices rise when too much money is chasing too few goods.

That’s why COVID stimulus + supply chain disruptions = record inflation.

Now the bureaucrats who set the rules for our economy want to reverse that.

Since they can’t fix supply chains with policy measures, they’re trying to reduce the amount of money in the economy … aka “financial tightening.”

The quickest way to do that is to raise taxes. That’s certainly what I would prefer.

Tackling inflation that way would cause a lot less harm to owners of stocks and property … i.e., you and me. That’s because it wouldn’t require a big rise in interest rates.

We both know that’s not going to happen. Voters in our “have your cake and eat it too” economy wouldn’t stand for it.

That leaves interest rate hikes as the only politically workable way to address inflation.

But rate hikes are an extremely blunt tool. They reduce demand in two ways:

- By making it more expensive to invest in businesses. That leads business owners to cut spending on materials and labor. As millions of such decisions filter throughout the economy, it leads to a general slowdown, removing inflationary pressure.

- By reversing the wealth effect. Households whose stock portfolios and property values are falling are less likely to splurge, even if their incomes don’t change.

Basically, rising interest rates combat inflation by making people poorer.

Chemotherapy for Inflation

There’s just one problem with trying to engineer a reverse wealth effect.

It only works for households with wealth.

Thirty-five percent of Americans don’t own a home. Half of U.S. households don’t own any stocks. And 5% of the population owns 75% of stocks.

That means the burden of the wealth effect falls on a fraction of the population.

Since you’re reading this newsletter, that fraction probably includes you.

It gets worse.

The uneven distribution of U.S. wealth means that to bring inflation under control, the Fed has to raise interest rates a lot higher than it would otherwise.

In other words, since a reverse wealth effect doesn’t affect households who don’t hold wealth, it has to be really severe for those who do.

Raising taxes would be like proton therapy for the cancer that is inflation. It would be precisely targeted and leave most assets relatively unharmed.

Using the wealth effect is like old-fashioned chemotherapy … indiscriminately killing good cells and bad.

Sometimes the treatment is worse than the disease.

The Wealth Effect in Action

A lot of pain has already happened.

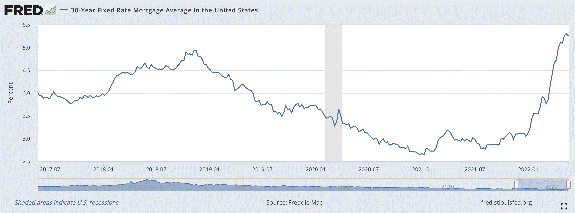

Mortgage rates have skyrocketed in anticipation of higher interest rates. That’s causing a rapid fall in house sales, as well as falling prices:

In the stock market, 70% of S&P 500 stocks and 85% of Nasdaq stocks are below their 200-day moving averages. As I explained in my article last week, that’s primarily through “derating,” i.e., a fall in price-to-earnings ratios as investors refuse to pay inflated prices for future earnings:

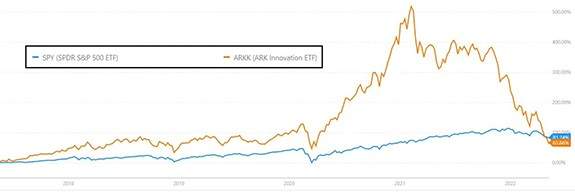

Now, I don’t know how many investors own the poster child for overpriced stocks, the Ark Innovation ETF (NYSE: ARKK). But given that its current value is below that of the S&P 500, it’s a pretty safe bet that those who do are suffering a particularly nasty reverse wealth effect:

Perhaps such people would be happier to know that by losing so much value in their stock portfolios, they’re contributing a great service to the U.S. economy.

Somehow, I doubt it.

Keep Your Own Wealth Effect in High Gear

Amidst rising interest rates, war in Europe and other calamities, The Bauman Letter‘s Endless Income portfolio has delivered outstanding positive returns while markets sank over the last six months.

It’s doing that by (a) exploiting opportunities to buy high-quality assets at sane valuations and (b) locking in high income flows by “buying low and yielding high.”

I started deploying that strategy in the second quarter of 2021. That gave my Endless Income portfolio a big jump on the current situation.

But with the Fed relying on the wealth effect to tame inflation, more high-quality stocks will see their prices decline below sane levels, offering great opportunities.

Eventually, the market will realize that and bid those prices back up.

My job is to find those opportunities before that happens and tell my readers about them.

Your job is to protect your wealth by grabbing them when I do.

Kind regards,

Ted Bauman

Editor, The Bauman Letter