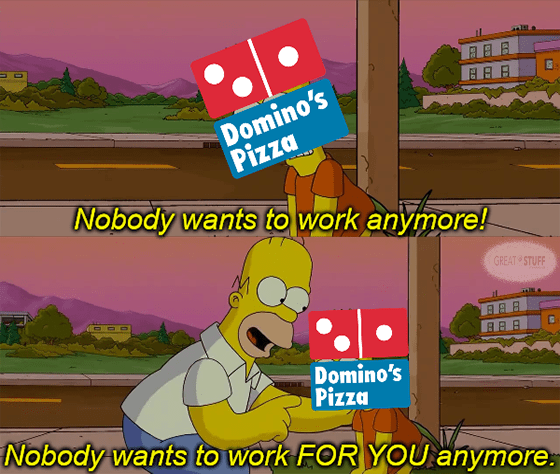

Domino’s Doesn’t Deliver

Great Ones, some of y’all are probably gonna think I’m a raging liberal after today’s write-up on Domino’s Pizza (NYSE: DPZ). What I am or am not isn’t the point. Still, I want you to remember one thing: I didn’t say it.

Say it? Say what? What was said?! Tell me!

We’ll get to that in a minute.

Last Friday, pizza purveyor Domino’s offered up its quarterly report … and it was bad.

The company has clearly forgotten it’s ‘80s slogan of “Avoid the Noid!” because this report had Noid all over it.

Eeew!

Exactly. I’m still washing my hands after just reading it.

Citing “a number of headwinds,” Domino’s net income plunged 22% to $91 million, or $2.50 per share. Revenue, meanwhile, rose about 3% to $1.01 billion. Wall Street expected earnings of $3.06 per share on revenue of $1.02 billion.

So Domino’s missed both Wall Street’s top- and bottom-line expectations … but we all know how messed up those expectations have been this year.

So, what really drove DPZ’s 8% drop on Friday?

Sales at company-owned stores, or “comps.” Domino’s comps fell 3.6% in the U.S., ending more than a decade’s worth of growth stateside. On that front, far and away the biggest driver for declining U.S. comps is Domino’s labor situation.

According to CEO Ritch Allison:

In short, Domino’s is so understaffed that it lost six days of U.S. business last quarter because it couldn’t staff its stores.

Now, before you go all “People just don’t want to work!” — let’s hear from the analysts at Stifel:

We believe Domino’s employment proposition for would-be delivery drivers has deteriorated compared to many of the benefits now offered by third-party services. In addition to providing fully autonomous scheduling, many third-party companies also offer aggressive financial incentives to attract delivery drivers— particularly at peak times —and assign no additional responsibilities beyond delivering the order.

We believe Domino’s staffing issues will persist until it improves its attractiveness to drivers, which could require significant investments and time.

Did you catch that? Stifel just said the quiet part out loud: Domino’s doesn’t pay its workers enough.

Remember, I didn’t say it. Stifel did.

It’s not that people don’t want to work. It’s that people don’t want to work for you, Domino’s. From DoorDash to Uber Eats, delivery competition is heating up massively.

Why would you deliver pizza for Domino’s when you can make more delivering that same pizza by working at DoorDash? (And, anecdotally, get “free” pizza on occasion … from what I hear of some DoorDashers.)

Basically, Stifel is saying that Domino’s delivery pay isn’t up to par with its competitors, and that to bring pay and compensation up to those levels will take significant investment — aka money.

As part of its research note, Stifel cut its price target from $425 to $345, while maintaining its hold rating.

After hearing Domino’s solution to its staffing issues, I don’t think Stifel was hard enough on the company.

That solution: Have you pick up your own damn pizza … and give you a $3 tip for doing so.

Personally, I tip my delivery driver 20% … which is often way more than $3. In fact, $3 probably wouldn’t even cover gas for me to go pick up my order. But then, I live in the sticks, so that’s not true for everyone.

The bottom line here is that Domino’s is still operating like it’s 2019. It is not. The labor market has changed. You’d think that losing the equivalent of six days’ worth of sales due to being short-staffed would prompt some bean counters to take a closer look and maybe pay their delivery drivers more.

Instead, however, Domino’s is shifting that responsibility to you … and giving you a paltry $3 bucks for the trouble. On that note, I agree with Stifel. This isn’t going to work until Domino’s gets serious … and that’s gonna be costly for both investors and Domino’s.

Avoid the Noid, indeed.

How To Make Up To 10 Years’ Worth Of Gains — In A Single 48-Hour Trading Window

You make the trade on Monday … relax for 48 hours … and then close it on Wednesday. It couldn’t be any simpler.

Yet the profits using Adam O’Dell’s new two-day trading strategy are out of this world. With top-performing trades like 519% in two days … 440% in two days … 400% in two days…

To get the details, go here now.

Going: Up To The Spirit In The Sky

Spirit in the skyyyy!!!

That’s where I’m gonna go when I … umm … don’t have the budget to fly JetBlue? Yeah, let’s run with that.

Prepare yourself — you know it’s a must — you’ve got a friend in Great Stuff. So you should already know that Spirit Airlines (NYSE: SAVE) and Frontier Group (Nasdaq: ULCC) were set to merge together like a budget airline Voltron.

That is, until JetBlue Airways (Nasdaq: JBLU) fancied itself a better suitor for Spirit. With $3.6 billion in cash at the ready, JetBlue was all set on adding Spirit’s budget fleets and routes to its offerings … but JetBlue seemed to forget that Spirit is, well, its own free spirit.

And today, Spirit rejected JetBlue’s “unsolicited offer,” accepting Frontier’s $2.9 billion bid instead. As far as Spirit is concerned, management thinks a merger with fellow budgeteer Frontier will be more likely to pass antitrust approval than a larger merger with JetBlue.

JetBlue even sweetened its offer with a $200 million “breakup fee” in case regulators ended up blocking the deal, but nope, Spirit is gung-ho on merging with Frontier. (In fact, I think this is the most excited anyone’s ever been about picking Frontier.)

Are y’all getting flashbacks to the antitrust anxiety of the Kansas City/Canadian National Railway tie-up of years’ past? No? Just me? Fine…

Going: Apple Pays (Yeah, Right)

Alright, show of hands, Great Ones! Any of you use Apple Pay?

WOOOOT! Yeah, this Apple fanboy right here!

Now let me see all y’all Google Play fans out there!

*crickets*

That’s what I thought. And I’m not even gonna bother asking about you Visa tap-to-pay users out there … all three of you. Anyway…

If you Apple (Nasdaq: AAPL) users thought it was hard finding tap-to-pay alternatives to Apple Pay, welp, it’s not just you. There are no alternatives — that’s the Apple way. And Apple’s “don’t give users options” attitude just earned the company another antitrust complaint in the EU.

The EU argues that Apple’s throwing its weight around to make Apple Pay the dominant payment option on iOS, simply by not letting competitors have access to a phone’s NFC transmitter. If other apps literally cannot send the tap-to-pay info … Apple Pay pretty much wins by default, no?

For its part, Apple is flabbergasted: “Apple Pay is only one of many options available to European consumers for making payments, and has ensured equal access to NFC while setting industry-leading standards for privacy and security.”

Aw, how consumer-friendly of Apple. So … who’s actually right?

If the EU’s investigation proves that Apple is, in fact, blocking competition via its iOS technology, then “such a conduct would be illegal under [the EU’s] competition rules.” And Apple would certainly never skirt the law to hold its dominance … right?

Gone: Bittersweet EV Dreams

Speaking of deliveries…

That was like, five whole minutes ago, Great Stuff!

No, no — it’s not just pizza that’s headed to your door. Which one of you ordered some Chinese electric vehicle (EV) deliveries on the side? Because I think only half of your order showed up…

Delivery figures for China’s top EV makers are out and … they’re not great, I’ll say that.

Nio (NYSE: NIO) delivered 5,074 vehicles — down from the 10,000 it delivered in March and much lower than 7,100 vehicles in April 2021.

Li Auto (Nasdaq: LI) faced a similar sales drop-off and only delivered 4,167 vehicles in April — far short of the 11,000 deliveries Li made in March. And it still pales in comparison to the 5,500 deliveries Li had in April 2021.

XPeng (NYSE: XPEV) fared a bit better, as it was the only EV maker that saw year-over-year growth in deliveries. But as far as reaching Wall Street’s delivery expectations goes … Li, Nio and XPeng all have a long, long way to go.

So what’s the hubbub, bub? Surprise: It’s COVID.

Again?!?!

What do you mean “again?”

COVID has been the problem for Chinese EV makers for over two years now and it’s still a literal plague on EV makers’ productivity.

This is why Tesla (Nasdaq: TSLA) investors were justifiably worried about the company’s Shanghai plant closure. The threat of continued COVID closures is real. For Tesla, the disappointing numbers from Nio, Li and XPeng could be a grim preview of delivery reports to come.

Editor’s Note: Biggest Breakthrough Since The Discovery Of Oil

A tiny Silicon Valley company is using AI to unleash the largest untapped energy source in the world.

I’m not talking about oil, gas, wind, solar, hydro, nuclear … or anything you’ve likely heard about before. Yet this breakthrough is set to help launch an era of cheap, abundant electricity the likes of which the world has never seen.

Ah … get a big whiff of that great, glorious smell.

No, it’s not buttery, garlic-y pizza that you’re smelling — it’s a fresh tray of delicious earnings reports, hot out of the oven and ready for trading.

Let’s see what Wall Street cooked up this week, courtesy of Earnings Whispers over on Twitter:

Last week might’ve been all about Big Tech, but this week? Well … this week we’re more focused on the average American consumer. (That’s you, by the way.)

Right off the bat, you and your fellow Great Ones should be looking at AMD’s (Nasdaq: AMD) earnings on Tuesday afternoon — especially if you’re personally invested in the Great Stuff Pick.

With Intel’s (Nasdaq: INTC) meh-worthy report already in the books, the bar has been set for AMD’s report. Will AMD keep crushing Intel on the data center fight? And how are AMD’s consumer sales shaping up?

Options traders expect at least a 9% move from AMD in either direction, and a big beat might send AMD skyward … depending on the market’s appetite for growth this week.

Also reporting on Tuesday is Airbnb (Nasdaq: ABNB), which will be worth a watch for any of you in travel-related stocks. With airlines reporting massive surges in passenger traffic, how will that translate to booked stays at Airbnb?

The options market expects ABNB stock to move 9% in either direction, and I’d be willing to wager that it could move more than that, given how other travel stocks have taken off recently.

Then you have DraftKings (Nasdaq: DKNG) and Fubo (NYSE: FUBO) … two sides of the sports gambling storm. Subscriber/user count is the name of the game here, and Fubo’s already trying to add in some sportsbook action to supplement its income.

Meanwhile, DraftKings has been beaten into a pulp like it tried to ignore a bookie amid the growth stock sell-off. Options traders expect DKNG stock to move about 12% after earnings, and it’ll all come down to DraftKings’ profitability.

Elsewhere, I’m looking at Etsy (Nasdaq: ETSY), which is expected to rally or crash 15% on its report.

Given how online sales have tapered off recently, I’d expect Etsy to fall … and seeing as how Etsy recently hiked its pay cut from sales on the platform, it might be hurting for cash more than ETSY investors realize.

As with AMD and the rest of the growth stock herd, the biggest problem is how the market will react … as Wall Street has been selling practically everything lately, especially tech-related firms like these.

Which reports are you looking forward to most, Great Ones? Send me your thoughts at GreatStuffToday@BanyanHill.com. Otherwise, here’s where else you can find us:

- Get Stuff: Subscribe to Great Stuff right here!

- Our Socials: Facebook, Twitter and Instagram.

- Where We Live: GreatStuffToday.com.

- Our Inbox: GreatStuffToday@BanyanHill.com.

Until next time, stay Great!

Regards,

Joseph Hargett

Editor, Great Stuff