“What just happened?”

Plenty of punch-drunk investors are asking themselves that question after Monday’s market carnage.

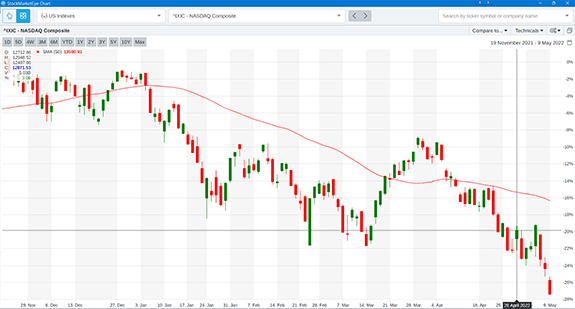

For one thing, the end of the 13-year bull market has been confirmed. The Nasdaq crossed into bear territory in late April:

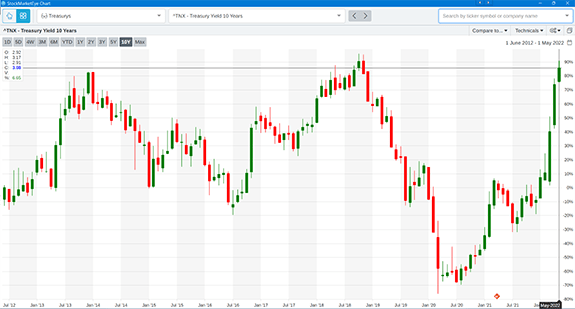

For another, the Federal Reserve’s hawkish turn has caused bond yields to spike:

But those are just symptoms.

Something else is going on … something so BIG that it will define the next era of the stock market.

That’s why now is such a critical time to take a few steps back and look at the Big Picture…

To Know Where You’re Going, Look Where You’ve Been

At the simplest level, “what just happened” is that stocks went down…

A lot.

Going one step further, we can say that stocks went down because bond yields went up.

Again, a lot.

But to really understand why stocks and bonds have fallen so hard and so fast, we need to understand why they went up so much in the first place.

The chart below shows the technology-heavy Nasdaq. I’ve included a 20-month moving average and a long-term trendline:

The extra lines illustrate something important about the last 12 years or so: Something was making stock prices go up faster than they had before.

A lot faster.

One factor was the emergence of mass-market technology companies like Amazon (Nasdaq: AMZN), Alphabet (Nasdaq: GOOGL) and Apple (Nasdaq: AAPL).

But even those stocks wouldn’t have done as well as they did if it hadn’t been for the Federal Reserve’s easy-money policies.

The Fed adopted quantitative easing (QE) after the subprime crisis as a temporary fix to protect the financial system.

But after the bond market’s “taper tantrum” of 2013, the temporary fix became a new market paradigm. It had four key features:

- Extremely low interest rates and abundant liquidity made borrowing money to invest in stocks and bonds almost costless. That led to an unprecedented bull market in both.

- The economy grew slowly because the government fiscal response to the subprime crisis was so meager. That made growth stocks attractive since nothing else was “growing.”

- In the absence of fiscal stimulus, the Fed continued QE longer than planned. The idea was that the “wealth effect” of rising stock and housing prices would stimulate consumer spending and boost the economy, since Washington, D.C. wouldn’t.

- Investors got used to all of the above and began to behave accordingly.

Taken together, those four features shaped the performance of every investment you or I, or anyone else made right up until the end of 2021.

Then everything changed.

The Price Is Right, Until It Isn’t

One of the biggest challenges facing every investor is figuring out the “right” price of an asset.

The problem is that there isn’t any such price. It all depends on the context.

For example, during 2020 and 2021, investors poured gobs of money into new companies that promised disruption, fast growth and huge future returns.

It made perfect sense at the time.

Until it didn’t.

The Renaissance IPO ETF (NYSE: IPO) is a great example of this phenomenon.

As the name suggests, the fund gives you access to emerging companies just as they make their initial public offering (IPO) to the investing public. The fund took off like a rocket in April 2020.

At market close yesterday, it had round-tripped all the way back down to where it started:

That’s just one example of the broader trend.

IPOs, special-purpose acquisition companies, crypto, meme stocks — everything that “only went up” for the last two years — are now crashing hard.

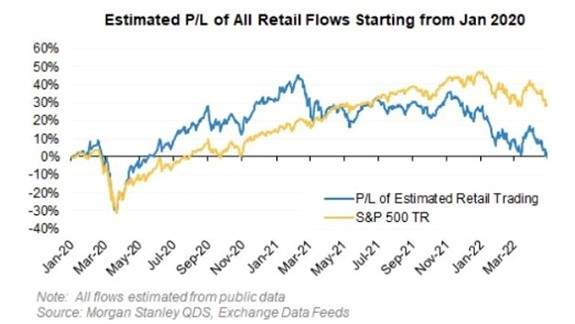

In fact, Morgan Stanley estimates that retail investors have lost all the profits they made since the beginning of 2020:

Does that mean that all those investors were mistaken?

That the prices they paid for their investments were “wrong?”

Not at all.

Those investing decisions made sense at the time.

But things have changed … and after Monday, I’d say they’ve changed decisively.

Say Goodbye to “the Bezzle”

In 1955, economist John Kenneth Galbraith observed that in bull markets, investors experience a “net increase in psychic wealth.”

It’s “psychic” because it only exists in the mind. The feeling reflects rising prices, not underlying value. He called this “the bezzle.”

Galbraith went on to note that the bezzle quickly dissipates when “money is watched with a narrow, suspicious eye” — for example, when asset prices are collapsing.

We’ve just experienced the mother of all bezzles. It wasn’t “wrong.” It was just the natural response to the market paradigm.

That paradigm has changed.

But don’t take that as bad news. The bezzle isn’t the only way to invest.

Fortunately, I know exactly the right way to invest in this new market paradigm.

Kind regards,

Ted Bauman

Editor, The Bauman Letter