Well, we told you volatility was coming … and we got it in spades last week!

The immediate cause is Omicron and the Federal Reserve’s hawkish turn. But the real problem is excessive valuations and leverage.

Even when the market eventually recovers, those two threats can cause a SHARP correction, just as they did during the dot-com bust.

Should you be running for the hills or buying the dip?

Ted Bauman and Clint Lee explain the scenario and recommend two ETFs that will not only survive a pullback … they’ll outperform! Get the whole story in today’s Your Money Matters.

Beneath the Stock Market’s Surface

In recent Your Money Matters videos, we’ve discussed hedging your portfolio against a possible market correction. We’ve reiterated that having a “Plan B” is the best way to defend against these sharp movements in the market.

Because let’s face it, the market was already uneasy even BEFORE the Omicron variant and news about the Fed.

In a Bloomberg article, Peter Atwater, president of Financial Insyghts, said: “The bodies have piled up so deep and among so many crowd-favorites that folks can no longer step over the problem,”

That’s why Ted and Clint are helping you find a way through with the right stock picks and sectors that can help you flourish when others buckle under the pressure.

Click here to watch this week’s video or click on the image below:

VIDEO TRANSCRIPT

Angela: I hope you are a subscriber to our YouTube channel. If not click that button below because we’ve been talking about hedging strategies against volatility. And sure enough, here we are … we record these on Fridays and what a volatile week it has been.

Just today the payroll was a huge miss. We’ve got the Federal Reserve suddenly hawkish, and I hate to say it, but there’s still a pandemic out there that likes to wreak havoc on the stock market every so often.

So I’m seeing these comparisons now about how the current market looks a lot like it did before the dot-com bubble burst. And essentially what that means is we’re seeing that the Dow is ending up one day, the Nasdaq down, and vice versa. It’s just not moving in sync and it’s just another sign of an unhealthy market.

So Ted, what I’d like to know, what everybody watching would like to know: is this the beginning of the end or is this just another great opportunity to buy the dip?

Ted: Well, it’s not the beginning of the end because the stock market never ends. I think that’s the most important thing to remember, no matter what happens. The thing is just, you’ve got strategy and you’ve got tactics. Strategy is you’re trying to make money. Tactics is you need to be intentional about it. And that means sometimes you need to pay attention to what the market is telling you and adjust your portfolios accordingly. Right now, I think what the market is telling us is that the era of super-high valuations, where investors are prepared to ignore these insane multiples of 10 or 20 times forward sales and all that, is maybe coming to an end. Because it depends on the artificial fuel from the Feds.

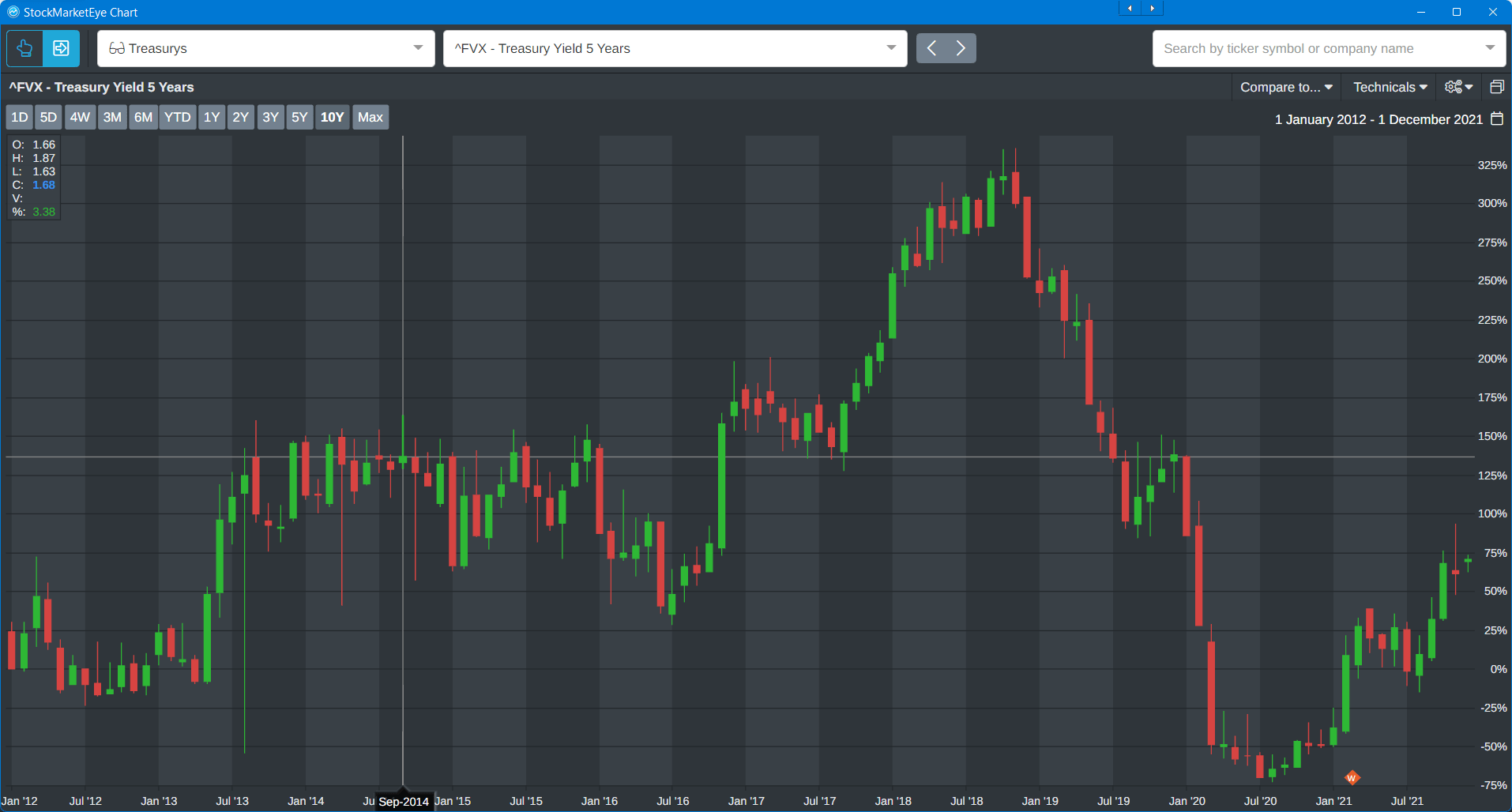

So, let’s quickly look at a couple of things that are going on. The first thing I want to show you is the five-year Treasury yield.

I’ve taken this back over a 10-year period, because I specifically wanted to point out that aside from that big spike in 2017, 2018, 2019, five-year yields were pretty stable during the mid-teens. And we’re probably heading back up to that kind of a level.

And if you recall, it wasn’t really until sort of late 2019 or kind of mid 2019 and into the pandemic, when a lot of these growth stocks took off like a rocket. You remember that just before the COVID crash, stocks had reached new heights. There’s clearly a relationship between these kind of midterm treasury yields and the appetite or the willingness of people to pay for future earnings. If we’re heading back up towards that level, in other words, the kind of levels that we saw back in those days, which is around the kind of the 1.6 yield on the five year, then basically we could be back to that sort of scenario and that’s really important for investors to be aware of because you just don’t want to buy into stocks at high valuations if that’s where we’re headed.

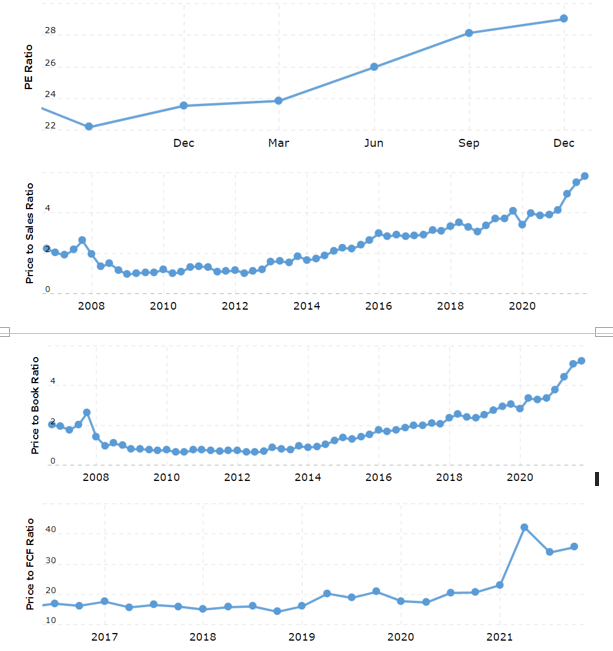

The second thing I want to show you is just how absurd things are looking, particularly in the Nasdaq.

This is the Nasdaq composite, which obviously contains a lot of firms, not just the big ones, but some smaller ones too.

The top panel shows P/E ratios since the beginning of the year. They just keep marching higher. Second panel shows price-to-sales, and I’ve put this over a longer term, because I just wanted to illustrate that they started to drift higher around 2014, and then they’ve really taken off this year. So even though there’s been a slow upward drift of price-to-sales, they’ve gone ballistic this year.

Next panel is price-to-book, which is another critical measure, same pattern. There’s been a slow upward drift, but the rate of change has gone up. And then finally price-to-free cash flow, which is my personal favorite because I like companies that earn cash because cash lets you do things. Look at 2021, I mean, it spiked, fell back and then it started to take back up again.

Bottom line here is that where the Big Tech companies and the small tech companies reside i.e., the Nasdaq, we’re seeing that multiples are historically stretched.

That’s the one thing, but here’s this the second thing, and this is even more important.

Multiple expansion is one way that stock prices go up, right? People are willing to pay more for future earnings. But if you have a situation where people have kind of bet that earnings are going to go up by willingly paying higher multiples, and then they go down, you’re setting yourself up for pretty brutal correction unless the Fed comes back and rescues the market again, and I think they’ve said they’re not going to do that.

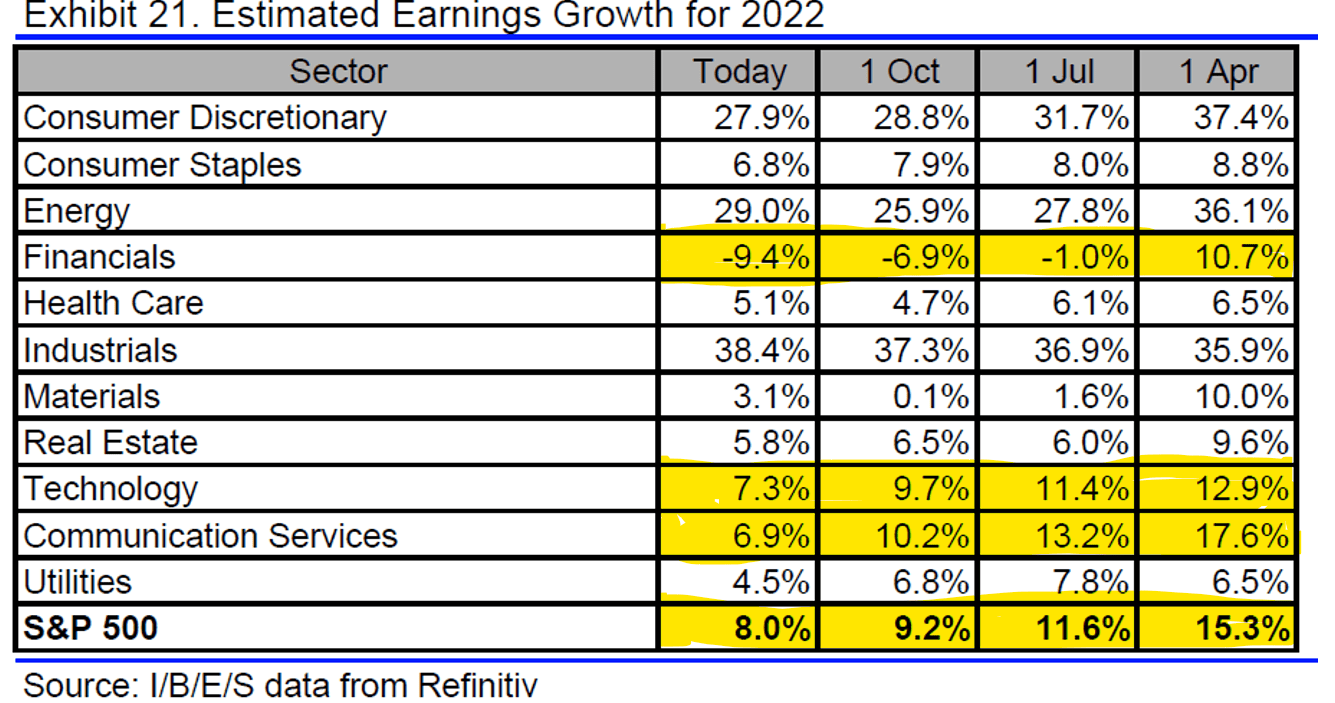

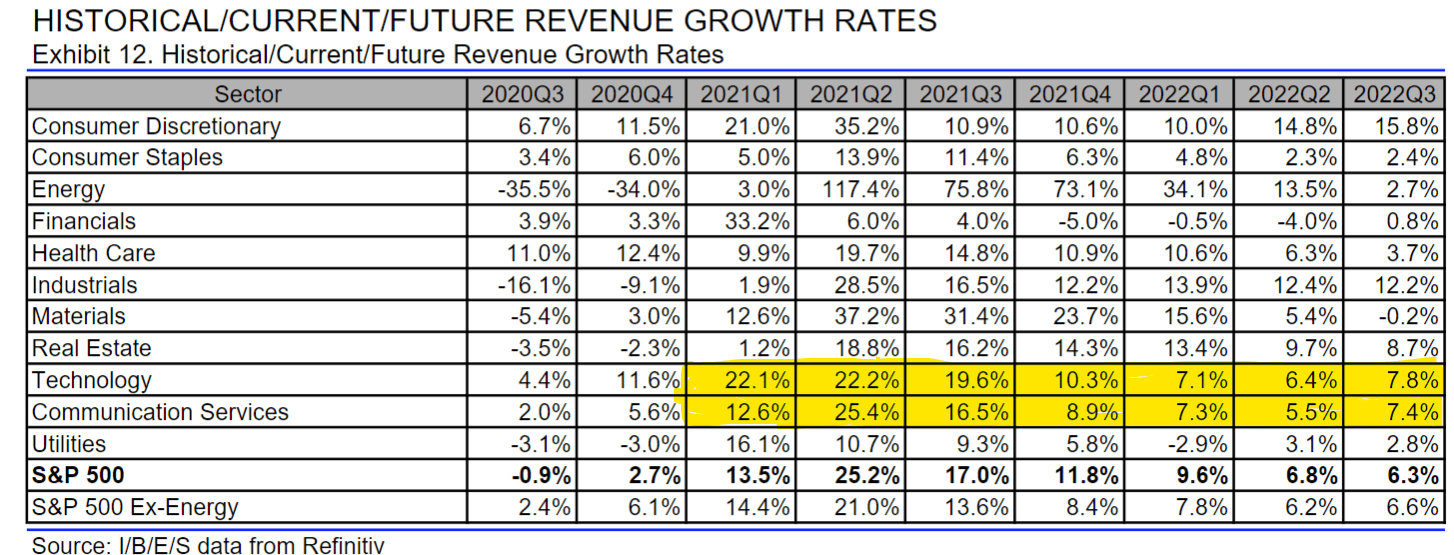

So here’s a chart that shows forward estimated earnings growth for selected sectors for next year:

I’ve highlighted the ones that are really set up for the most brutality. One is Financials. And I think that’s probably because you’d think that, with rising interest rates, banks and what not could get higher spreads on their loans, etc. But I think it’s also because of concerns about credit yields, particularly high yield, junk bonds and all that. There’s a lot of nervousness there.

But the key one is technology and communication services, which is where a lot of these high-flying, high valued companies are. The estimates have halved since the beginning of this year. I mean, in April, people were thinking that, in communication, you’d get 17.6% earnings growth next year. Now it’s down to 6.9%. Overall the estimations have almost been cut by 50% since April this year.

The next thing I want to just show you is again forward earnings estimates, and I’ve zeroed in on technology and communication.

In the first quarter of this year, people were talking about 22% in technology, but it’s dropping down to just half that in this quarter, and then even lower going into 2022.

The basic message here is that, to the extent that people have bid up multiples, because they believe earnings growth is going to be more rapid … now earnings estimates from the people who really have a lot at stake here, the big investment houses, are saying that earnings are actually going to be slowing. That’s led to a scenario that I think it was Bloomberg said, “It’s a Tarantino scenario.”

Here are the guys from Pulp Fiction:

What they were saying basically is that while the stock market has been rising overall, while the party’s been going on in the front of the building, in the back these guys have been taking out some of high-flyers and basically executing them. That’s what’s been happening to some of these stocks.

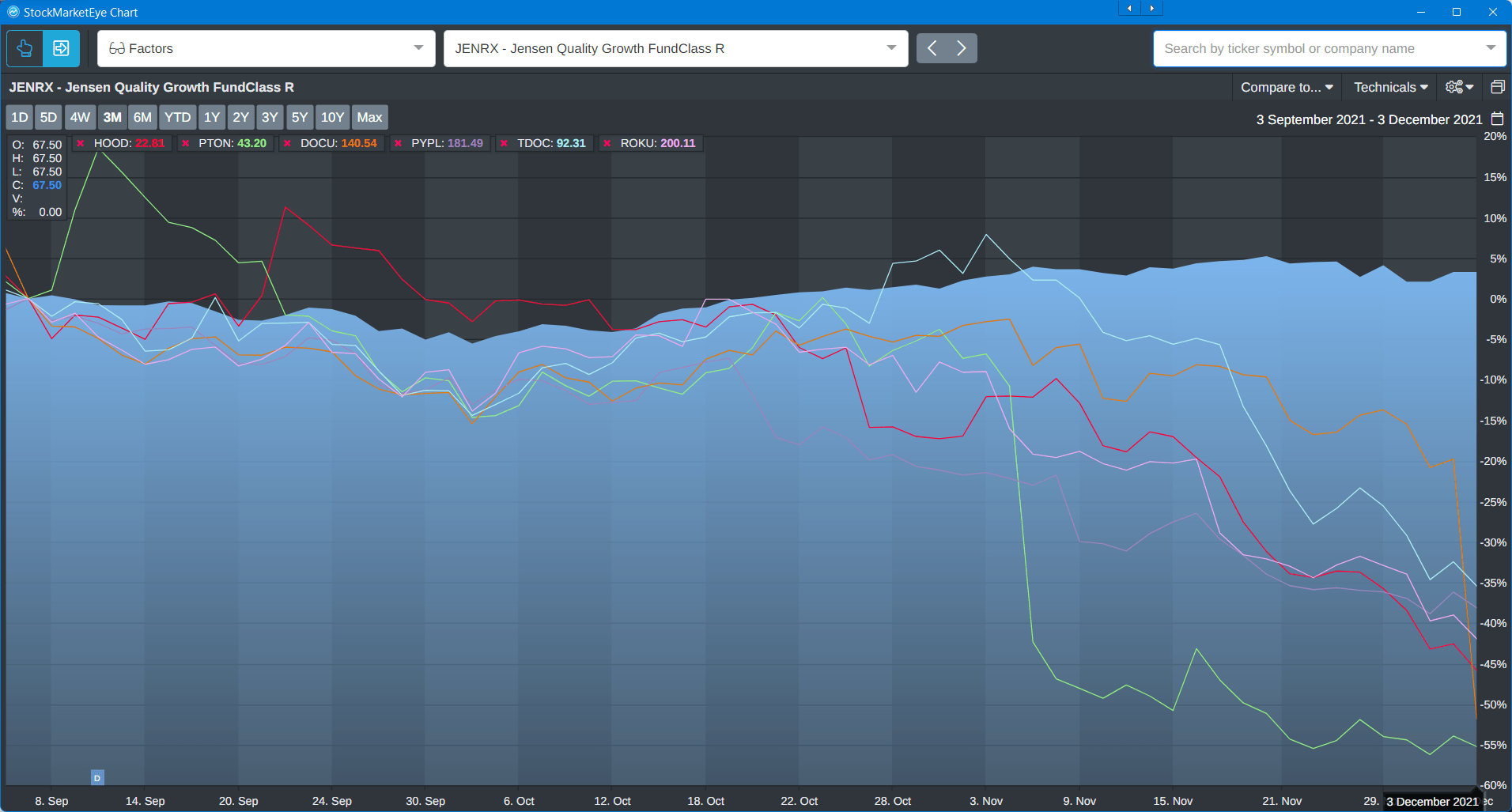

Here’s a chart I put together showing this:

The mountain is a quality growth fund, which basically is a proxy for quality companies. The ones that return good cash flows, the things that I like, that have good robust earnings that don’t tend to vary a lot. But look at some of the ones that the guys have taken out back and shot. Robinhood, Peloton, DocuSign, PayPal, Teledoc, Roku, all of them. I mean, some of them just absolutely being crushed in the last couple of months and the drop picked up considerably at the beginning of November, but it’s slaughter out there.

What that’s telling me is that there’s just no justification for buying these companies right now, unless you can get them at the lowest possible dip, when their multiples get reasonable. Sure, maybe. But they’re not reasonable yet, you still have some so way down to go.

But there’s a couple of other things and I just wanted to mention.

You mentioned Omicron and all that. What chairman Powell is saying is that this could lead to higher inflation because of the supply side, right? If China, for example, keeps trying to shut down their entire economy, if Omicron gets loose in there, then we’re going to have supply side constraints, we’re going to have more shortages, and that means that people are going to bid up the prices of goods and we’ll have inflation.

But that means if the Fed tightens to try to contain that, we’re going to get a downturn, right? Because you’re tightening not because the economy is necessarily going too fast, but because we just can’t get the stuff. Some people would call that a policy mistake. But right now, with inflation as it is, they aren’t saying that much choice.

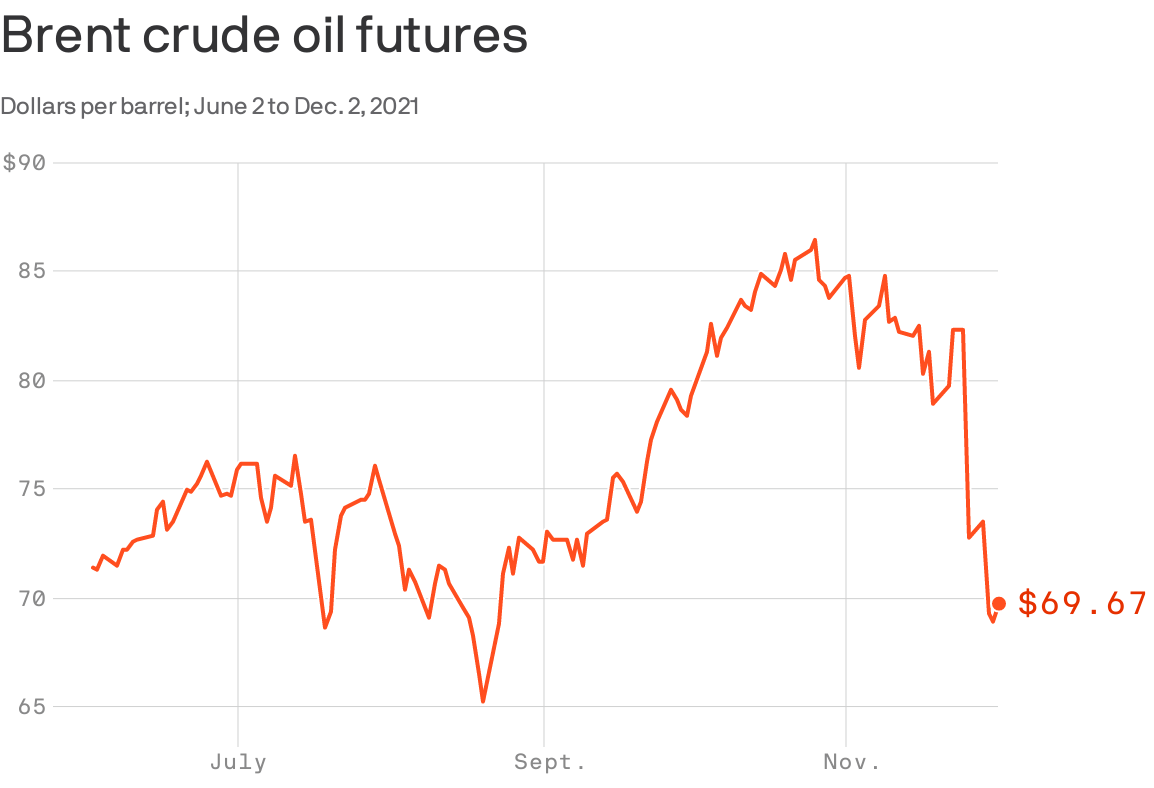

So in those situations, what investors want is cash. Just one last chart just to show that expectations of growth if the Fed does tighten. This is what’s happened to the oil price, which is a good proxy for expectations of growth.

It just fell off a cliff a couple of weeks ago. And that’s going to feed through to make consumers happier, but I think it’s an indication that markets think that the global economy is going to slow.

Last point, a lot of today’s retailer investors are leveraged, and they have no experience of what happens when the Fed tries to tighten to control inflation. Never seen it. They were in diapers when the Fed did this before. The best evidence of this is that right now, the average retail investor, has just 46 cents in equity in their trading accounts for every dollar of margin balance that they hold. That’s the worst that it’s been since the dot-com bubble.

In the old days, experienced investors would’ve listened to what the Fed was signaling and say, “Well, I’m going to dial that back in anticipation.” They haven’t done that. In fact, they piled into the options market in an insane way. I mean, I forget the multiple, but trading in Tesla options, call options at something like five times the volume of trading in the S&P 500. This is basically a party where investors … they’ve never been to a party like this before, and they’re not sure how it can end.

Now, I’m not suggesting it’s going to end in a disaster, but better safe than sorry.

Angela: Now, Clint. I want to ask you … so I know before these things happen, there are always things that we can look out for. Are there any indications, any charts we can look at, any clues we could take in to know if the growth outlook is going to hold up or if it’s going to deteriorate?

Clint: Yeah. There are several kinds of market-based indicators that I would follow, that I would point out, because it just goes back to Ted’s point about valuations and to justify where they are. I mean, companies, indexes, whatever, need to grow into those valuations.

So far this pullback can start to get worse if that growth scare starts to worsen. What I want to look at is areas of the markets, especially looking outside of stocks. Stocks are incredibly volatile, a lot of ups and downs that can be very emotional. I want to look at areas that fall outside the stock market, but that are still leveraged to that outlook for growth.

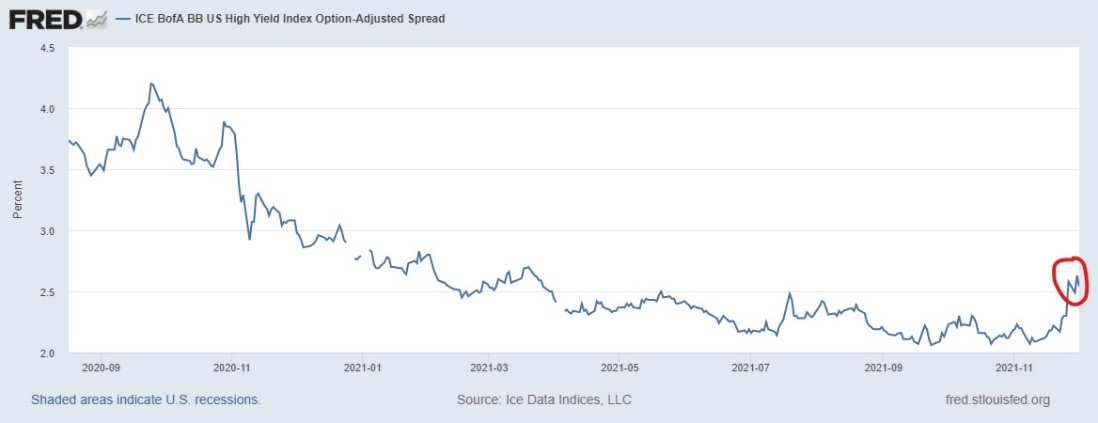

One area — probably the most important area — that I’m watching right now, personally, is with high yield spreads. High yield investors are lending money to these lower quality, financially struggling companies, that’s why they have to borrow at higher rates.

And so high yield investors, junk bonds, whatever you want to call them, they’re extremely sensitive to the prospect of getting their money back. When they see those prospects dimming, that’s when they start to demand more compensation to win. And so that’s really what a spread is, it’s how much of additional compensation above a risk-free asset like a Treasury that high yield investors are demanding.

I want to show one chart, just as an example of this. A growth scare that we had back actually in 2018, this was the last time that the Fed was starting to tighten. We saw a bear market in stocks, the S&P fell just shy of 20%, but here’s what Double-B bonds, that’s kind of the first trench of high yield. Here’s what that looked like back then.

What I’m highlighting with the red line on here, when we climbed above sort of that 2.6% level. That’s when you really start to see the growth scare kind of kick in, and that’s when you really start to see the volatility and the downside pick up in stocks. And so, what does this spread look like today? That’s the next chart I have here.

This is that same spread just looking back over the past year. And so, here’s what’s different with this pullback that we’ve seen so far relative to the others in 2021. This line had continued to stay pretty contained. I mean, you had some bump ups every now and then, but no meaningful jump. But this time around what I’m circling on red on here, we’re starting to break above some key level.

So we’re at that 2.5% level right now. This is one thing that I’m watching that tells me that growth scare looking forward is starting to intensify. Now, couple other areas that I would look at as well: Ted flagged oil. I would definitely watch commodity markets right here.

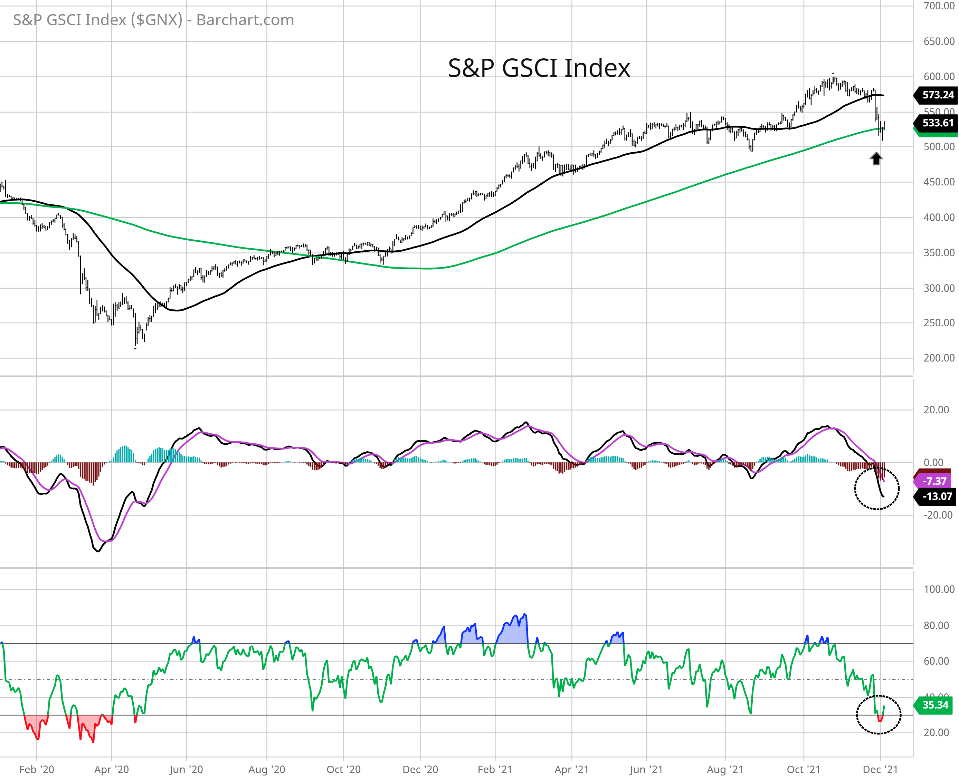

Here’s a chart of the S&P GSCI index, this is a broad base index of commodities:

And we’ve seen the dip, absolutely, but I mean, just look at this. Look at the uptrend that we’ve had over a year now. So right now, what I would watch with this index, it’s pulled back to the green line on here, that’s the 200-day moving average, for me to signal this as sort of a red flag for the growth outlook as if we were to break below that 200-day moving average and start to take out some key price levels on here like the 500 level.

Now, one thing I would point out when using an index like this is that oil does usually feature pretty prominently, tends to be heavy weight in a lot of these indexes. And oil can be manipulated, whether it’s through cartels like OPEC or the U.S. releasing some of its strategic reserve.

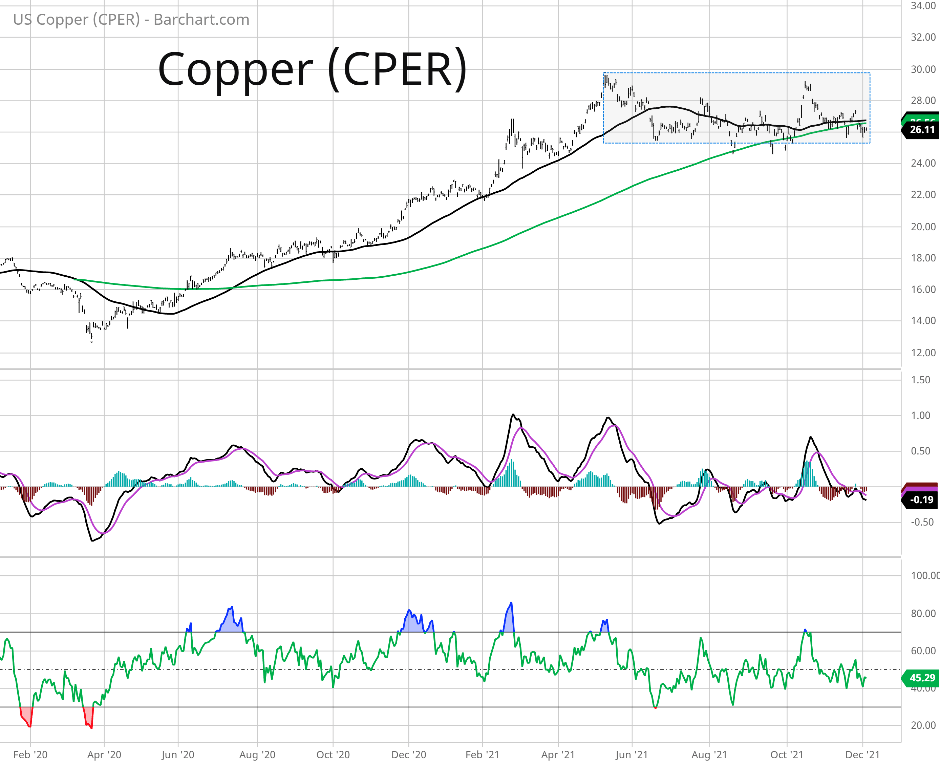

So one of the things I like to look at in the commodity space are metals, especially metals that have a broad industrial use across many end markets. I would look at copper to that end. Here’s a chart of the CPER ETF that tracks copper going back over a year now:

And so far, this is not flagging the growth scare to me. Copper’s been trading in sort of this range that I’m highlighting with a box on here since May or June timeframe. If we were to start to break down below this box that would be my warning signal for a growth scare being reflected in copper prices.

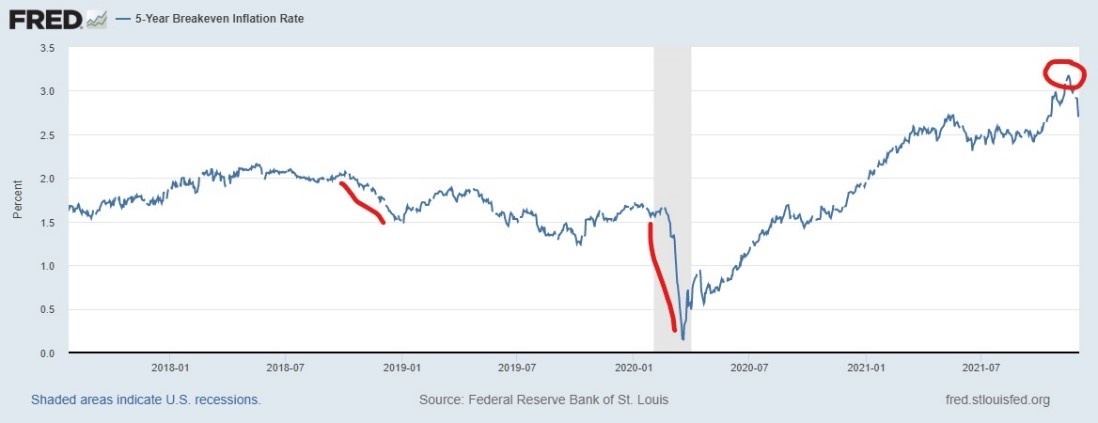

And then the last metric I want to point out is with inflation expectations. So the growth outlook heavily influences what investor are expecting for inflation. We can track those expectations with something called inflation break evens, it’s pretty simple. You can take a normal five year Treasury security and then take one that’s indexed to inflation, a tip security. And the difference between the two should be your implied expectation for what inflation looks like over the next five years.

So, here’s that rate going back.

I took this back to 2018, because I want to show a couple other growth scares on here. So the first red line on the left, that’s in 2018 when we had that growth scare, and then you had the big dip in 2020 as well. Since then, we peaked around the 3% level. And we’ve pulled back some, we’ve retraced, just a little bit of that.

What I would look for on here is if we started to dip back below that 2.5% level that we saw earlier in this year. That would tell me that the growth concerns or are starting to intensify, that weigh on the inflation outlook. These are the thing that I would track to see if that deteriorating outlook is really going to start to hammer stock prices here.

Angela: Well, it looks like this uncertainty isn’t going anywhere, anytime soon. But obviously it is impossible to time the markets and the solution is never going to be to just completely get out of the game. So let me ask you, what sort of companies might you look for in this sort of scenario?

Ted: Well, I mean, I’ve been saying all summer that really the critical thing is to look for quality. Quality basically just means companies where you know that there’s going to be earnings, and there’s going to be relatively stable earnings. Those are companies that are established, they have moats, they have a strong market position. There’s no doubt that no matter what happens, they’re going to survive.

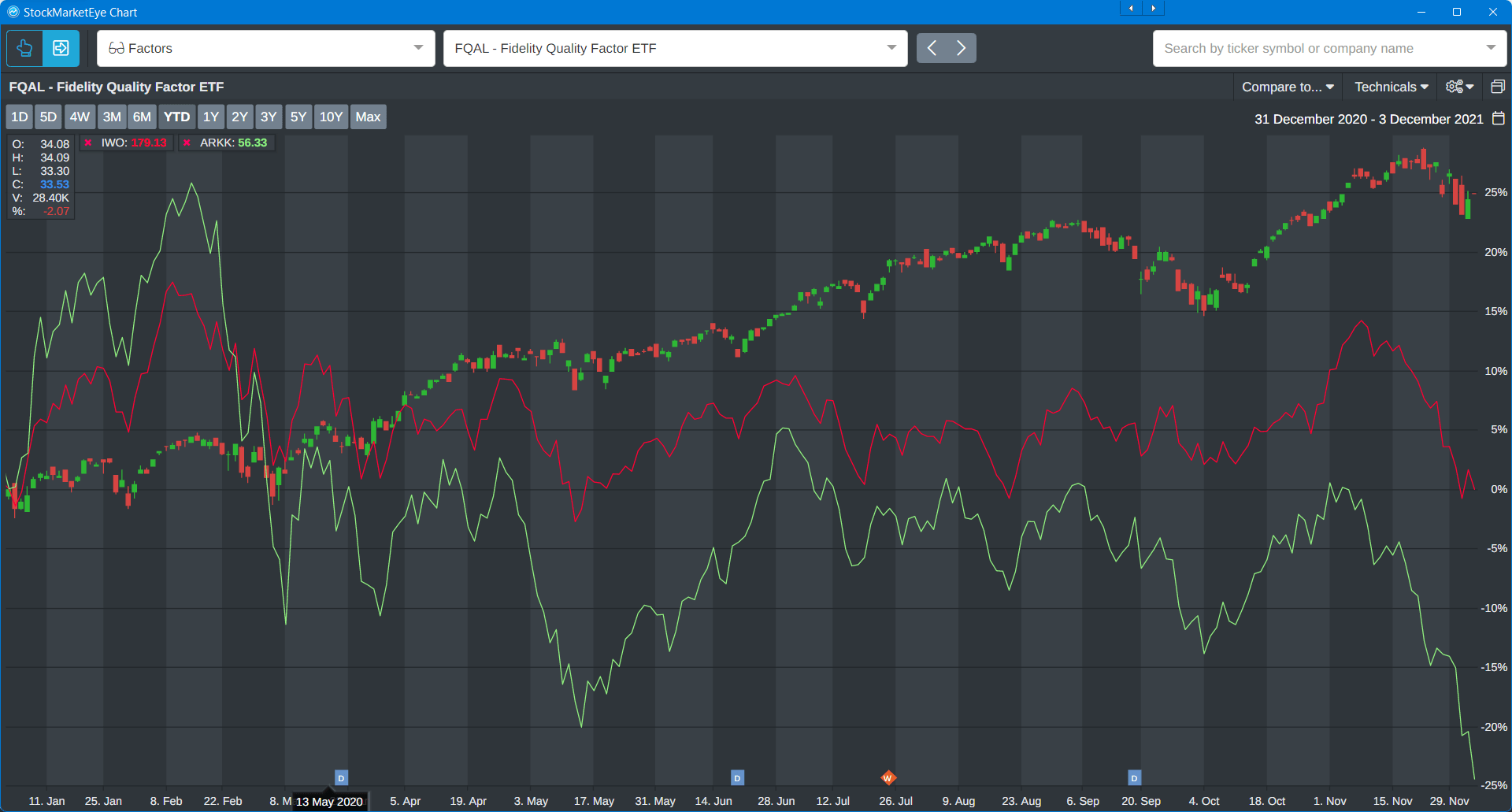

Just to prove that, here’s a chart that I put together showing FQAL, which is the Fidelity Quality Factor ETF, going back to the beginning of this year, compared to IWO, which is the Russell 2000 Growth ETF, in other words, the small cap growth stocks. And then ARKK portal Cathie Wood, everybody’s been picking on it. But this is why they’ve been picking on it:

Because you can say that the future’s bright, and it remains bright. But right now, if you want to keep your money and grow it, you want, all year you’ve wanted, to put your money into quality. And it’s true that if you already hold some of these stocks, you don’t necessarily want to sell them and lose all your money, but it’s going to take a while for them to bounce back and you just need to accept that.

So if you want to rebalance your portfolio, get back into quality.

Now, if you go to a place like Yahoo!Finance or Seeking Alpha, and you look at the holdings for FQAL, it’s not going to surprise you. They’re the companies that everybody would think of as quality. They’re established, they have earnings, those earnings are not going anywhere. That’s where you want to be.

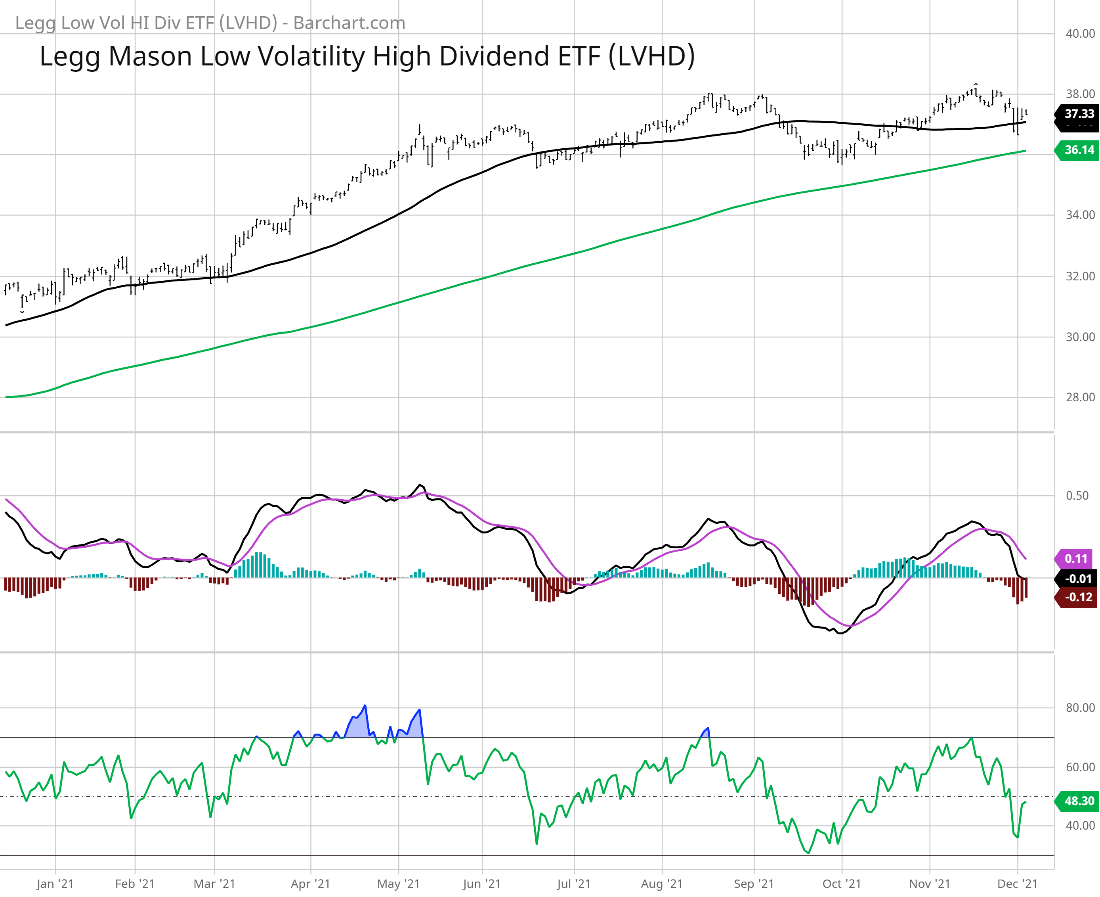

Clint: Yeah. Along the same lines too, you can look at LVHD, I’ll show a chart right here:

This is the Legg Mason. It’s a low volatility, high dividend ETF. And somewhat Ted was talking about, this is one that goes through, looks for companies that have low volatility in terms of both their stock prices, but also low volatility with their earnings. So it means they have stable earnings. Historically, it’s about a 2.7% dividend yield. You can see on the chart here.

This has also held up better as you would expect than the overall markets during the recent pullback that we’ve had. And then, yeah, same thing. I mean, just go, you can look at the ETF, but then go look at the holdings and see what types of companies are in here. I mean, you’ll see that these are some staple names or names that have that mode or dominate their end market and so they have that more stable earnings profile.

Angela: And as a final option, of course, you could always join The Bauman Letter, because Ted I know you’ve made a number of recommendations these last few months, this last year. Companies that can withstand this sort of uncertainty.

Ted: Well, yeah. And just on that score, at the beginning of the year, it wasn’t clear where things were going to go. And we’ve had a couple of stocks, just like everybody else, that were flying high. We did tell people to take profits on them at the time. But they fallen since then. And that’s just the way things work. And they are clustered in that growth future earning scenario. But all this year, we’ve been just going over and over again, looking back at companies that have definite prospects and that means definitely making money no matter what happens. And one of the big things obviously is infrastructure. So keep your eye on that, we’ve got news on that score.

Angela: Clint and Ted, thank you very much. Thank you all for watching. Please leave us comments, let us know what you think, and we’ll see you next week.

Good investing,

Angela Jirau

Publisher, The Bauman Letter