Everyone is blaming the Federal Reserve for the current conditions of the market.

I mean, who else is in charge of rate hikes?

But perhaps the Fed isn’t solely responsible.

In today’s episode, Ted Bauman discusses the one psychological factor that’s also crushing growth stocks and crypto coins.

Click here to watch this week’s video or click on the image below:

Transcript

Howzit, everyone? This is Ted Bauman here, editor of Big Picture, Big Profits and of The Bauman Letter, with your Friday video. Well, today, I’m going to talk about the state of the stock market. No surprise there, it’s not good. Here’s a chart that shows what’s been going on for the last, really, we’re getting onto a six-month timeframe now:

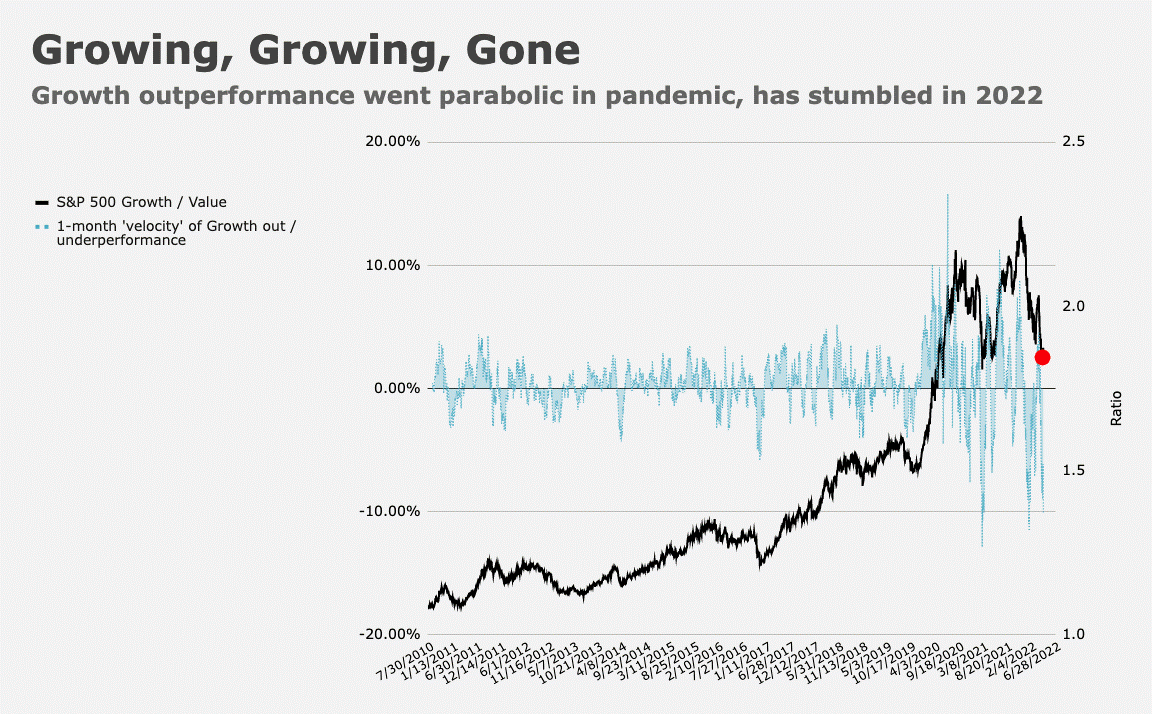

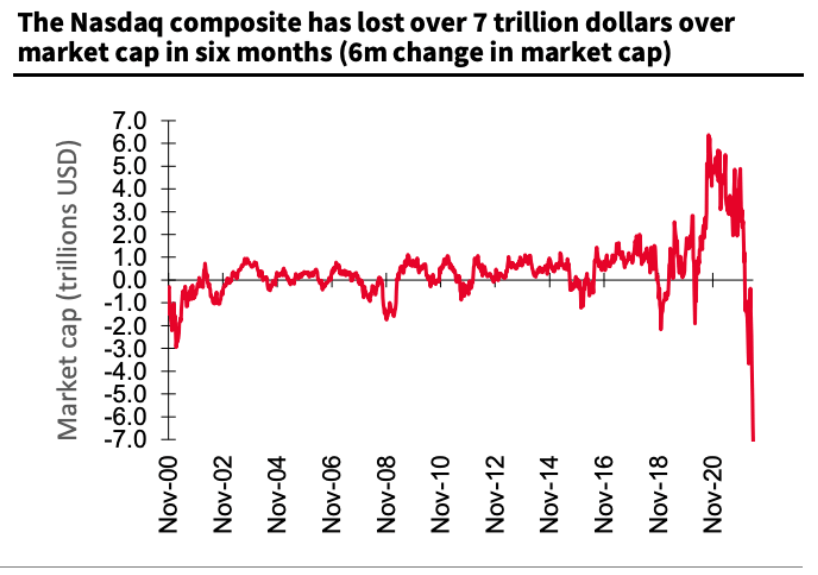

But basically, what’s happened is that everything that was so good about the period after the COVID crash is all over. I mean, here’s a chart that shows that if you take the S&P 500, you separate out the growth stocks, you divide them by the value stocks, the higher the line goes, the better growth is doing. The lower the line goes, the better value is doing, at least comparatively, and you can see that things are really, really bad. And that has led to this. This is the Nasdaq:

It has lost over $7 trillion in market cap over the last six months and, actually, this is a little bit dated. I think it’s probably higher. I know that if you go beyond the Nasdaq and if you include the S&P 500 and all the non-tech stocks, it’s closer to $9 trillion. Folks, $9 trillion, is a hell of a lot of money for anybody, and so it’s not just the Fed that’s withdrawing liquidity from the markets, it’s the markets themselves that are giving up liquidity.

Remember, market cap is just an unrealized gain. It’s not real money, but it makes people feel wealthy, and when they feel wealthy, they spend money. We’re going to come back to feelings just now, but let’s just have a look at some of the specific assets and how they’ve done recently here. Again, this is Goldman Sachs’ basket of non-profitable U.S. tech companies, which really drove a lot of the gains. I mean, basically, people were speculating on companies that had a good story to tell about their future and this is where they are. They’re back to where they were in 2019:

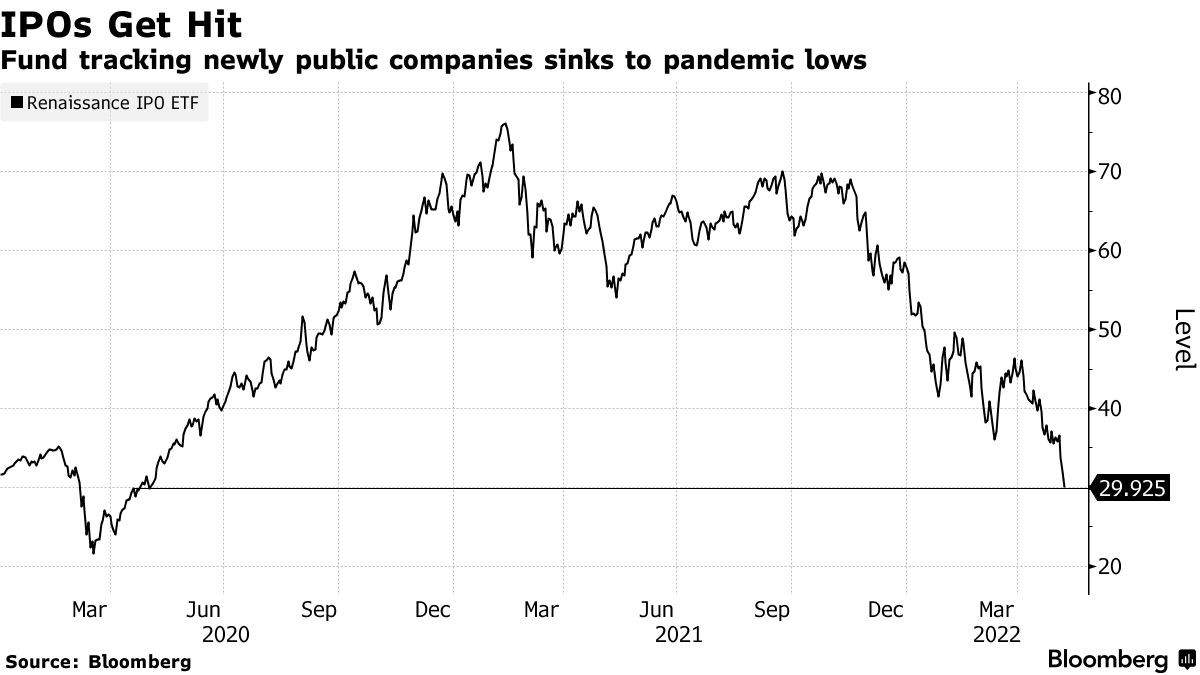

So, we’ve basically erased all the gains of the last two years and people are starting to call this the second dot-com bubble. It’s not really fair, because it’s not dot-com, but it’s very similar. This is IPOs, IPOs getting killed:

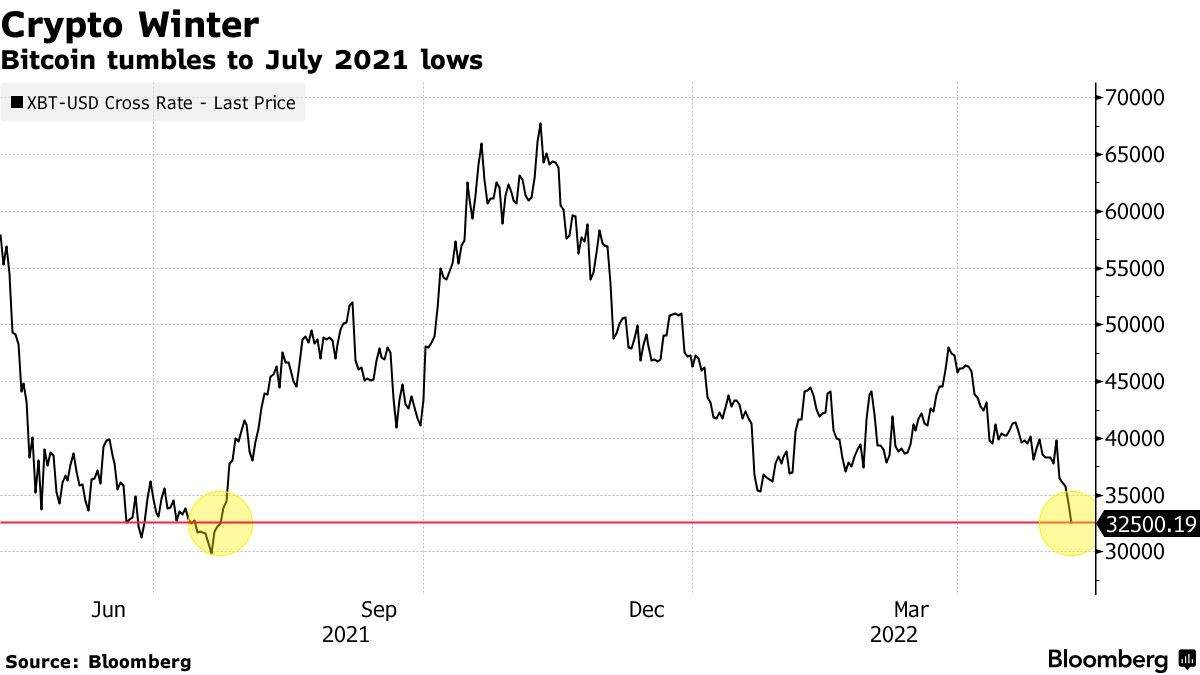

Obviously, when the market is frothy like it was, people launch new stocks because it’s a good time. When stock prices are going up, you increase the supply of stock. That means IPOs. Not so much now, folks. Again, we are back to where we were before COVID started. We’re back to late 2019, in that space. Now, I’m not going to talk in detail about crypto. Somebody said, “I don’t want to hear you talk about crypto.” Fine, whatever, but I can’t help but mention that the market cap of all cryptocurrencies has fallen from $3 trillion in November to $1.15 trillion yesterday, and that’s a $1.85 trillion wipeout. So add that to the fallen stocks.

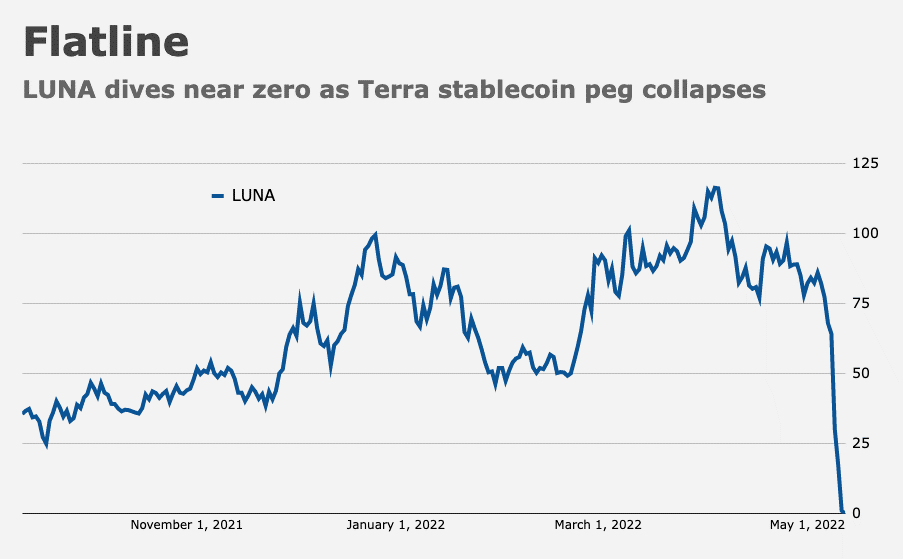

Here’s the chart that shows you the damage. This is just bitcoin. It’s not as long as that, but, basically, we’re back to where we were in July of last year. There was a big run-up in September, October. That’s all over now. We’re back down. In fact, this chart is also a little dated. I think bitcoin is below 30,000, if I’m not mistaken. But the big news, of course, in the crypto space is Luna. Luna is down to near zero. This is a big deal if you care about crypto because it just shows you that a lot of the belief that goes into the crypto space is starting to evaporate. And make no mistake, folks, all of this is driven by pure belief. There is no asset base behind something such as Luna or Terra (UST) and this is what happens when belief fades:

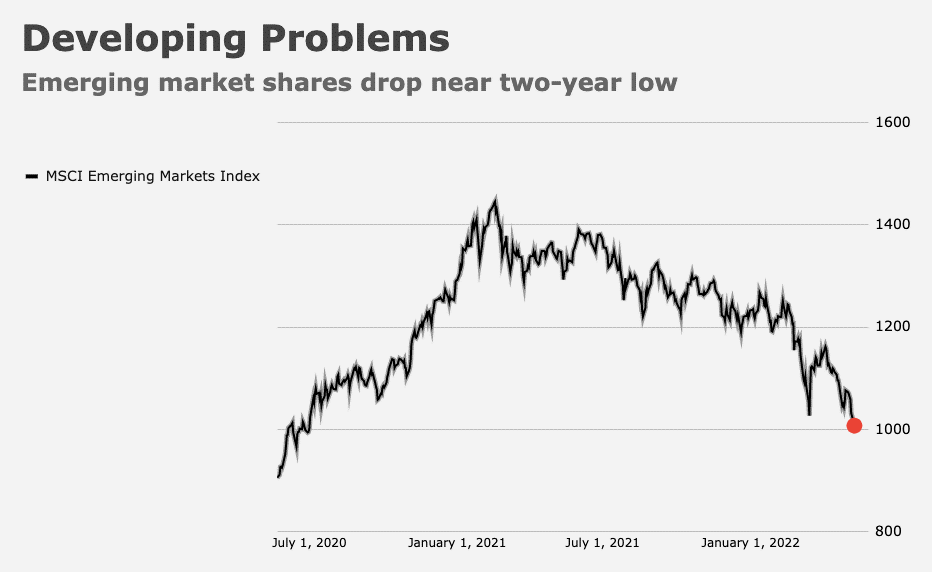

Now, the problem is that you can’t look elsewhere for security. Here is the developing markets picture, also down. We’re back to where we were in mid-2020:

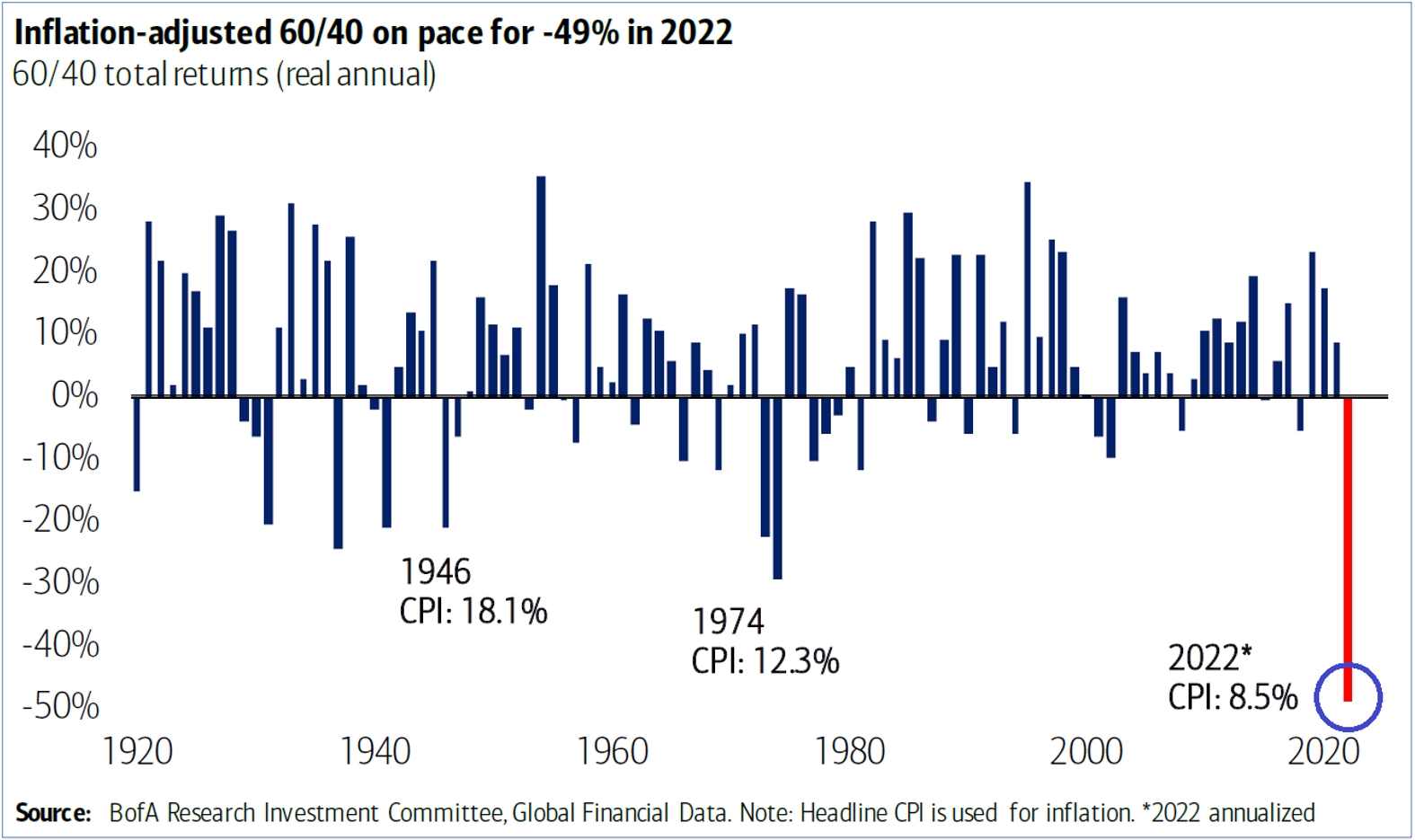

There it’s taking strain. Obviously, the increasing value of the dollar vis-à-vis other currencies is not helping them, especially more heavily indebted countries. And, of course, bonds are not helping. Here is the bond market:

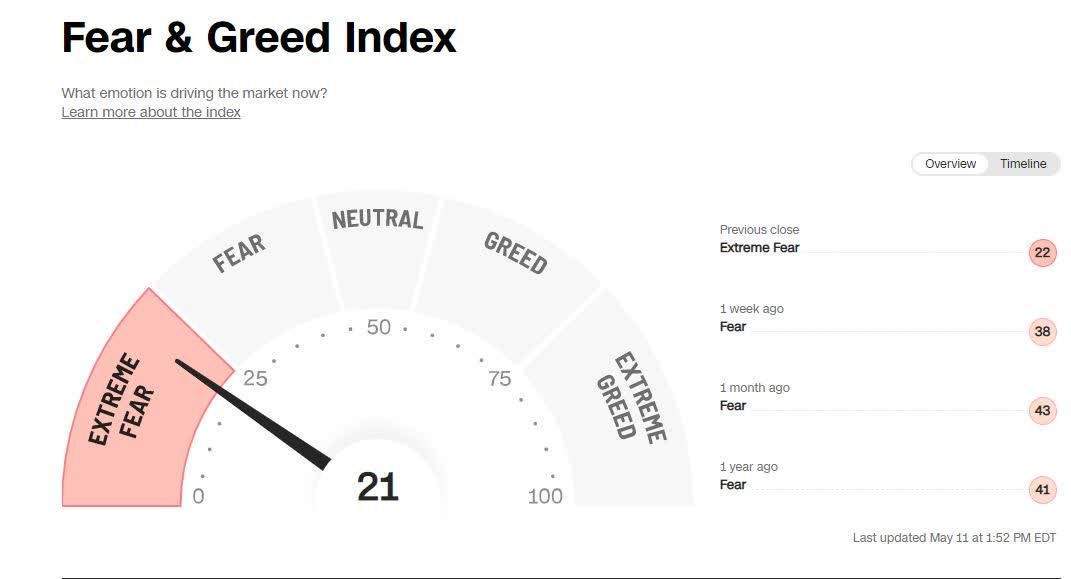

And, well, it’s not the bond market directly. Basically, what it is, it’s an inflation-adjusted picture of the 60/40 portfolio, which just goes to show you that what happens is, when you get a dual boom, a bull market, in stocks and bonds at the same time, which is something that’s not supposed to happen, but did happen because of the Fed’s QE policies. When it’s all over, they both fall hard, so there’s no place to hide. Now, all of this has led to a mood of extreme pessimism in the markets. Here is CNN’s Fear and Greed Index:

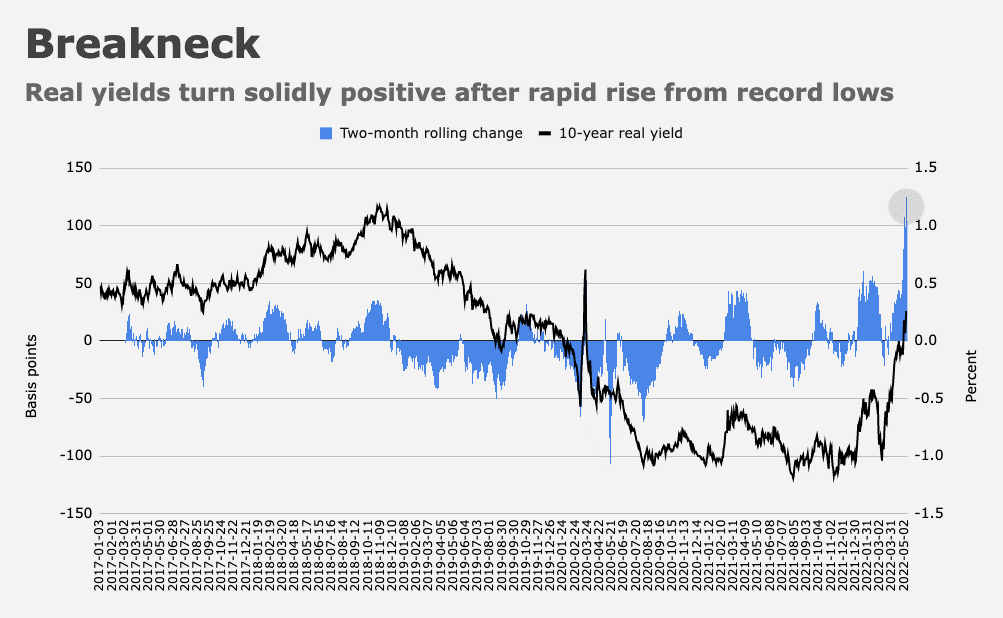

We are in extreme fear territory. Now, everybody is blaming the Fed for this. Everybody is saying that this is all about rising interest rates in response to inflation. And I’ve said so myself, and that certainly is a huge part of it. But as I’m going to explain, it’s not just about the Fed. There’s more going on than just the Fed. But to see why the Fed’s actions are so important, let’s look at a couple of charts that illustrate the basic relationships. This chart shows 10-year real yields:

Now, real yields are basically the difference between what the 10-year Treasury is delivering right now in terms of yield and what the market expects inflation to be in 10 years, and that gives you a measure of the market’s expectations for real yields. Now, one of the things you’ll note is that we’re still way below real yields as they were back in 2017, ’18, and ’19, and one of the big reasons for that, obviously, is that inflation expectations are higher. But so was the yield on the 10-year Treasury. So it’s not so much the yield itself that’s driving all this, it’s the expectation that the yields are not going to fall again.

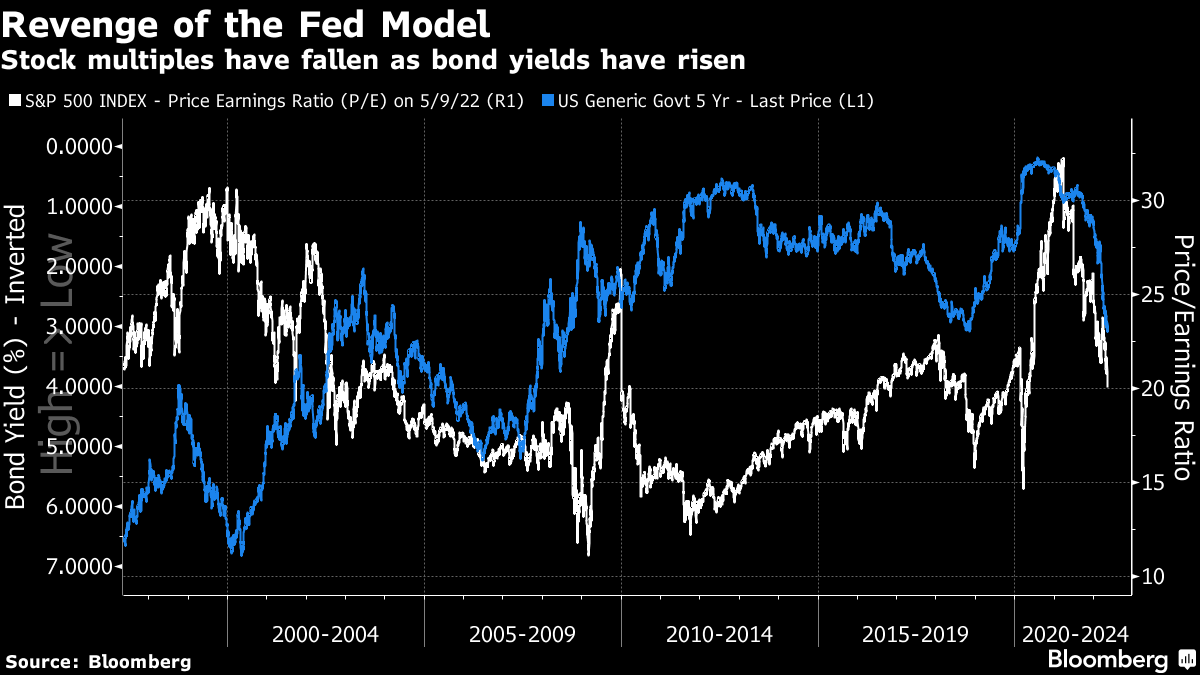

It’s the realization, basically, that the party’s over, that the Fed is taken away the punch bowl after 13 years of quantitative easing, and it doesn’t care what the stock market thinks. In fact, it wants the stock market to fall because of that wealth effect that I mentioned earlier. You take $9 or $10 or $12 trillion out of asset markets in terms of lost theoretical value, unrealized gains, people are going to stop spending money. That leads to a decline in inflation. Although, of course, the people who own all that stuff are not exactly the ones who spend money in the real economy, are they? They’re all very, very rich people, generally, who’ve lost all this money. Now, this is consistent with a long-term model or long-term relationship. Here’s a chart that shows the relationship between five-year yields and the PE ratio on the S&P 500:

Now, generally speaking, that the two tend to move in tandem when yields fall. And if you’ll note on the left-hand side, it’s an inverted axis, which means that the higher the blue line, the lower the yield. When yields are falling, the stock market rises. When yields are rising, the stock market falls. Now, there was there’s one big difference, and that is, really, the period between 2010 and 2019. And, in that case, real yields were holding fairly steady, not really falling, going sideways, and the stock market still rose. That’s the weird situation where you had a bull market in both bonds and stocks. That’s the consequence of QE, and now that we’re seeing that QE removed, we’re seeing both fall. We’re seeing bonds fall, which causes their yields to rise, so that bright blue line is falling, and so are stocks. And so, ultimately, what this all means is that, like I said, the party’s over, basically. People always made fun of me when I was cautious about the rise in stocks after the COVID crisis.

And I’m not going to reinvent history and say that it turns out that I was right. “Ha, ha, ha.” What I was wrong about was, I did not at that point realize that people would be so shall, I say sanguine? In other words, they were so willing to bet their fortunes on something as ephemeral as Fed policy. But I have a good reason to suspect that a lot of other people fell for the same thing, because I was looking at it from the perspective of history and history teaches two things. One is it teaches that these kinds of speculative bubbles that are driven by external factors do pop eventually, but they also teach that the motivation behind those bubbles, the things that drives them, tends to be the same everywhere. And when those things turn in the opposite direction, you get the opposite of the bubble. You get what you could call, like what happened before the Big Bang in the beginning of the universe, contraction. Anyway, we’re not there yet. I think we still have a ways to go and here’s why. Here’s a chart that shows growth stocks:

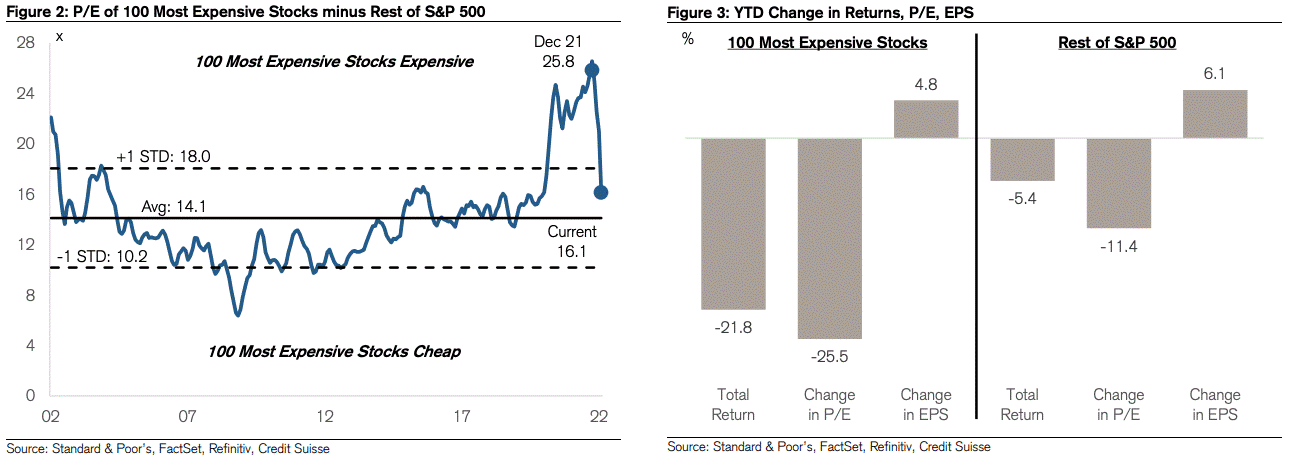

This is, again, a chart that shows the ratio between growth and value, the forward PE spread. They’ve fallen a lot. In other words, the spread between the PE ratios on growth stocks versus value stocks is still high. It’s falling pretty rapidly, that red arrow, but it’s still high. It’s still way above the 25-year average, so what that tells us is that we need movement in two directions to bring us back to the long-term average. We need PE ratios on growth stocks to fall and we need PE ratio on value stocks to rise. No prizes for guessing which kind of stocks I’d recommend you buy right now. Here’s another way of looking at that. Here is, on the left hand side, we see the PE ratio of the 100 most expensive stocks in the S&P 500 minus the rest of the S&P. So it’s a proxy for market divergence, the outperformance of those 100 most expensive:

Now, the long-term average is around 14.1. We’re currently at 16.1, which means the most expensive stocks have fallen hard, and as we know, that includes Alphabet, Apple, Google, Meta, all of them, Netflix, for example, they’ve all taken a big, big dip. But part of it is also because value stocks have risen, particularly in the energy space. But the key thing is that we’re still not back to the long-term average of 14.1. On the right hand side of the chart, you can see what’s driving all of this. As I’ve explained earlier, it’s really the overpriced growth/tech/long duration stocks. Since the beginning of the year, their change in price-to-earnings ratio has fallen dramatically. We’ve seen a 25.5% decline in the PE ratio of the most expensive stocks leading to a huge de-rating and a total return of over 20%. In fact, it’s probably higher today. This chart is a couple days old. And by contrast, the rest of the S&P 500, we’ve seen also a de-rating, but less than half of that are the most expensive stocks, so the total return in those stocks is a lot less.

Now, one thing I’d mention is that when we get a big turnaround in the stock market like this, selling tends to be indiscriminate. One is because people need to raise cash to meet margin calls and other fancy financial reasons, but the other reason is simply that people panic and they decide to sell everything and go at cash, even the stocks that are worth holding onto like value stocks, and that’s why we’ve seen a decline in them, but eventually that’s going to change. Now, here’s the key thing for today. Everybody blames the Fed. I blame the Fed, A, for inflating the bubble and for deflating it. When I say blame, I don’t mean like they did the wrong thing. I just mean that they are the proximate reason why all this happened. And now that The Fed is signaling that they want to go back to “normal conditions: with the Fed running the show and not the stock market, it’s going to be tough.

But there’s another factor here and that is people’s experience, their expectations. One of the things I like to say is that if you were, let’s say 15 years old when the stock market crashed in 2009, you would now be in the prime of your working life, and if you’re a Wall Street guy or girl, that means that you’re still going to be on Wall Street and everything that you’ve experienced for the last decade or more has all been based on The Fed’s previous paradigm, the QE paradigm. Now that we’re moving to QT, what are they going to do? They’ve never experienced this. Now, that has a profound impact on the way people make decisions. If you take a big financial risk and it pays off, you might take another one. And if that pays off, you might take an even bigger risk the next time. And if that pays off, you’re going to start thinking you’re a genius like the guy from that sports betting site, who said, “Stocks only go up,” you think you’re a genius. Well, not so much now.

You’re not a genius, you’re just a risk taker, and really the trajectory of the stock market, well, all markets really post the Great Financial Crisis, is one of greater and greater risk taking. Now, part of it is because the mathematics of having very, very low bond yields mean that it makes stock much more attractive and it pushes you up the yield. In other words, you chase yield. You basically look for riskier and riskier assets. But it’s also because people’s experience drives them. They get in the habit of winning and so they make bigger and bigger bets. It’s like you’re sitting at a crap table or any other kind of a gambling scenario. Sure, there were dips during this period, but they were usually V-shaped dips. And then people got used to the idea that the stock market would bounce back quickly so they were all dip buying opportunities.

And, of course, the mother of all V-shaped dips was the spring of 2020 with the COVID crash and policy makers rode to the rescue, boom. And everybody thought, “Well, this is the way the world works. Let’s put our chips down. Let’s bet on more of the same.” The problem is that people assume that recessions and stock market crashes could be stopped in their tracks and that triggered something, risk taking went wild. It went to the point where people were pouring money into profitless SPAC deals, IPOs, tokens named after dogs, digital drawings of bored monkeys, algorithmic stable coins promising 20% payouts like TerraUST. Now, it was the natural culmination of a decade long bull run. It was just the appetite of risk has become the norm and people decided to do all those things. Now, all during this period, my feeling was I’m resisting this with all my being, because I know as an economic historian this is not going to end well. I kept saying it. Now, of course, people are sheepishly agreeing with me saying, “Why didn’t you say so back when?” I did actually.

But the key thing is that it’s not just about the Fed and rates. What matters is that the risk cycle is doing a 180 degree turn and the rate hikes are just the catalyst. What’s changing is it’s what’s in people’s minds. People imagine that rate cuts happen and it just drives the stock market in this mechanical way, but that’s not necessarily true. I mean, think about the history. During the dot com bubble, The Fed funds rate was about 5%. The Fed started hiking again in 2004, but the housing boom continued even when rates were above 5%. In fact, the worst parts of the housing boom were deep into The Fed’s hiking cycle around 2006 when rates were already over 5%. So that tells you that it’s not just about rates, it’s about investor psychology. Now, in every case, the market turned. And so the big issue is, why did it turn? And really it comes down to investor psychology turning.

Now, it’s like a herd of something, a herd of Buffalo, for example, or a school of fish is probably a better example. A school of fish or a flock of starlings can turn on a dime, and that’s the way the market operates. Now, we know that The Fed is no longer in a position to maintain easy money because of inflation, but there’s every reason to suspect that it won’t do this in the future either because it’s realized what will happen if The Fed lets the market dictate the policy process. If The Fed feels it has to negotiate with the stock market and with bond markets and, God forbid, crypto markets about what it’s going to do, it’s lost its pricing power. It’s lost its control over financial conditions, and that’s what The Fed wants to squeeze out of the market. I said this about three or four months ago. I argued that The Fed was going to use inflation as an excuse to reassert its control, and clearly that’s what’s happening. And, finally, that message has sunk through.

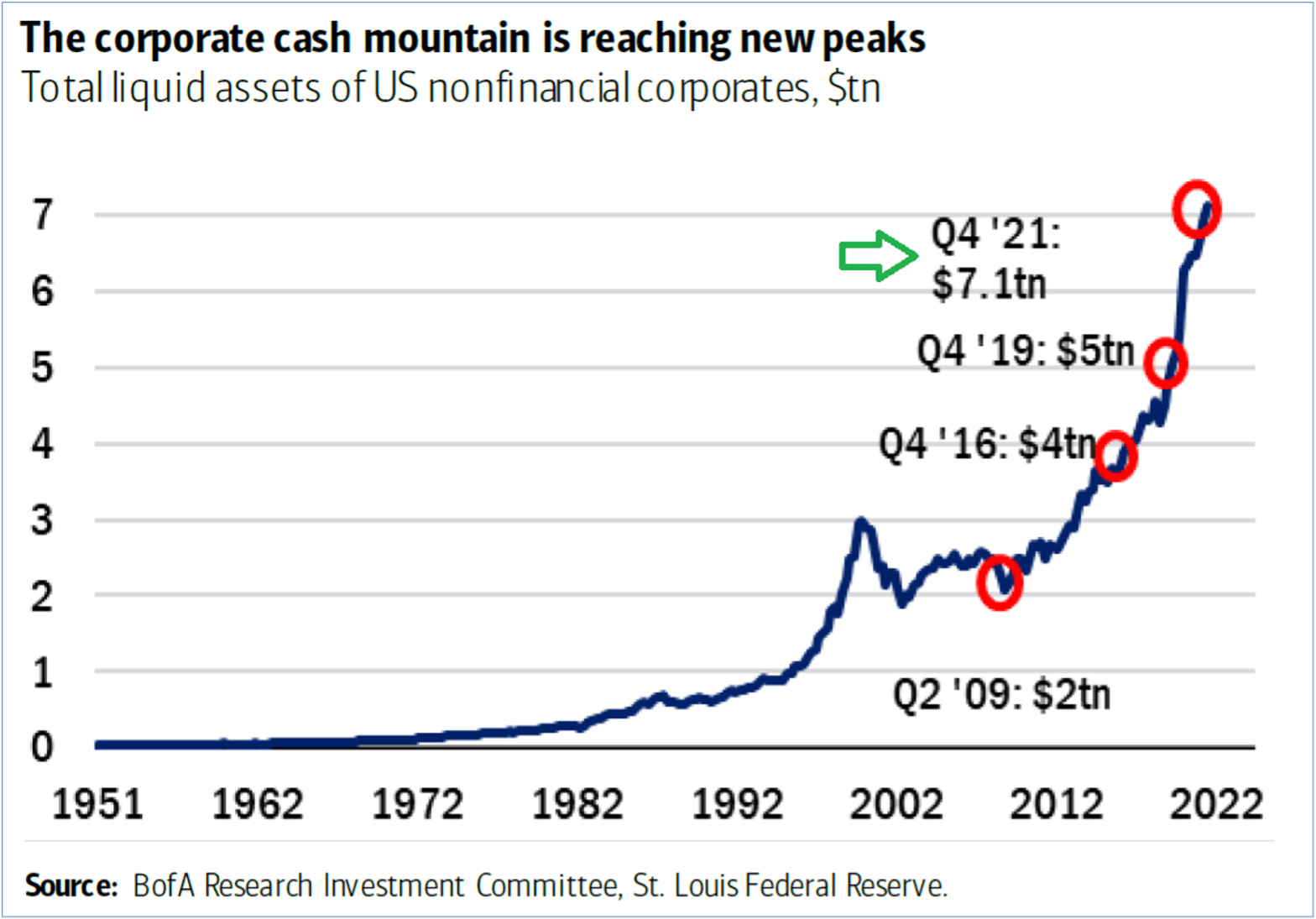

Now, in that context, I want to revisit a quote that comes from John Stewart Mill, one of the great economists, political economist, actually, in the 19th century. He said, and he knew this very well, but even back then that “the malady of commercial crisis is not in essence a matter of the purse, but a matter of the mind.” So that’s my message for today, folks, that what we’re seeing is a change in the way that people think about the way the stock market behaves. The critical thing is, when that change is complete, people are still going to be looking for yield and they’re going to be looking for them in the kinds of places that I specialize in, in The Bauman Letter, and one of those things is dividends. So my final message for today is just to show you what is likely to happen. Here’s a chart that shows that corporations are now sitting on an incredible amount of cash:

They used the opportunity of the last couple of years to pay down their debts and right now corporate America and non-financial companies, we’re talking about everyday companies, are sitting on $7.1 trillion worth of cash. Interestingly enough, that exactly offsets the fall in the Nasdaq. Now, what are they going to do with that money? Number one, they’re going to use it to buy back stock. That’s going to boost earnings per share. That’s going to boost share prices. So, eventually, you’re going to see that starting to happen. But more importantly, they’re going to boost dividend payments. They’re going to start basically dispersing cash because we’re probably going to be in recessionary conditions or at least weak conditions and they’ve got to use the money for something so why don’t they give it back to their shareholders. In fact, what happened during the 1970s, the S&P 500 companies that paid dividends doubled their dividend payments during the inflationary period of the 1970s.

Now, analysts right now expect 13% dividend growth from S&P 500 dividend pairs. That’s more than twice their expected growth rate. Certainly, higher than what we expect the market index itself to do. So the bottom line here, folks, is that if you want to protect yourself against inflation, against higher interest rates, and, above all, against market psychology, forget about all the stuff that worked the last 10, 15 years. Look for inflation protected dividend yields from the best high quality, cash flow rich, dividend paying stocks. Where are you going to find them? The Bauman Letter. My Endless Income portfolio is doubling the market’s performance over the last year and trashing it this year.

So that’s where you want to be. This is Ted Bauman signing off. I’ll talk to you again next week.

Kind regards,

Ted Bauman

Editor, The Bauman Letter