“Let me get this right. You have 16 properties? Each worth about $500,000? And they all have negative amortized loans?”

It’s 2006.

My wife and I are on a double date with Mike and Sue. This is our first time hanging out.

And … our last.

Mike went on to share his simple investment strategy:

- Step 1: Buy a property with no money down, negative amortized loan with a balloon payment.

- Step 2: When the property goes up in value, refinance and take the money out.

- Step 3: Invest in the next properties.

He loved to speculate with new condos and homes. They were worth an extra $50,000 to $100,000 by the time they were being built.

He’d just refinance the loan, take the money out, plop it down on two or three new properties, rinse and repeat.

“But Mike, what if prices go down?” I ask.

“They never go down. Not in Florida.”

I explain that prices DO go down, especially in Florida … ground zero of swamp land speculation.

And that interest rates are going up, a clear sign that prices will taper. That could be very bad for his adjustable rate loans.

He disagreed.

“People are flocking to Florida, pushing the market higher and higher.”

As my wife and I drove home that night, we discussed how insanely dangerous Mike and Sue were being with their business plan. At some point, the party would end. Wouldn’t it?

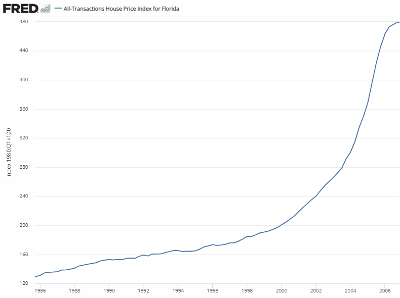

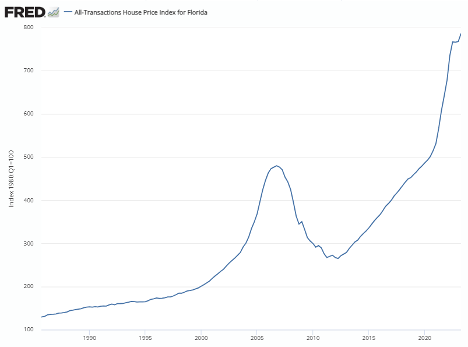

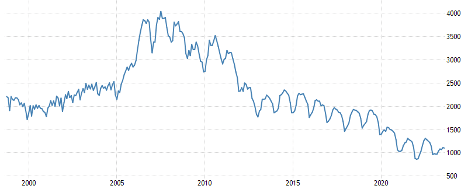

This is the chart I kept thinking about.

It shows the median sales price of a home in Florida.

Prices just kept climbing. Most people felt FOMO … the fear of missing out on all the money being made. There were stories of overnight millionaires.

But things just didn’t sit right with my wife and me. So, we put our only rental property up on the market. We listed it at some insanely high price. Within a week, we had offers. We made a nice profit.

Soon after, real estate prices in Florida started falling. They fell from a peak of $480,00 to $265,000.

On average, people “lost” $215,000 for every home they owned.

Speculators, like Mike and Sue, were wiped out within a year. They literally fled the state and left their properties abandoned.

First-time homebuyers were also wiped out. Anyone who bought at the peak didn’t see prices return to that level for a full decade … 2017.

And it wasn’t just real estate prices.

The stock market tumbled. It dropped about 50% over the next two years.

The entire economy went into “The Great Recession.”

Why do I tell you all of this?

Many of you have written in. You’ve asked …

Are We in Another Real Estate Bubble?

Will it all come crumbling down? Again?

Let’s take a look at the data.

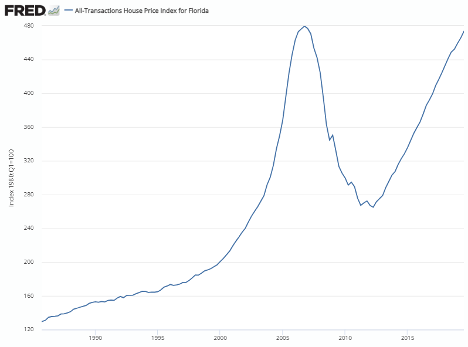

Home prices in Florida are soaring. I look at Florida because it tends to lead other states in real estate prices.

Here’s the rest of that chart that I showed earlier.

The median price of a home sold in Florida has now reached $785,000.

The national chart looks very similar. Prices have reached … $645,000.

But Aaron, there are no longer negative amortized loans. There are no longer balloon loans. And people, generally, have to put 10% down. Lenders do better background checks.

You are right. Mostly.

I do not think we are in the same situation we were in nearly two decades ago. Yet, while history doesn’t repeat itself, it does rhyme.

The more my team and I looked into the data, the more we saw red flags.

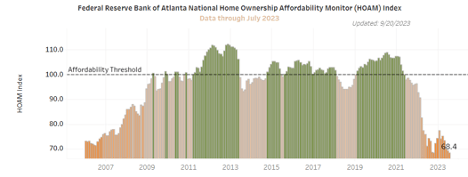

Red Flag #1: Home Affordability at 20-Year Lows

I often tell my team: “A chart says 10,000 words.”

And I think this is the case for the below chart, credit to the Atlanta Fed.

Today, home affordability (based on income, interest rates and more) is at the lowest on record.

The last time it was this low was in 2006.

To me, that is very alarming.

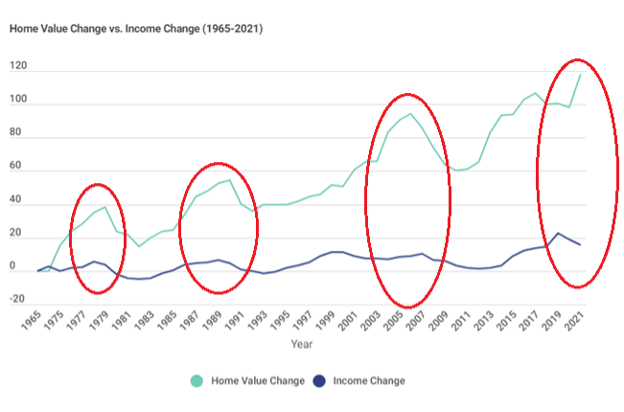

Red Flag #2: The “Fourth Gap”

This is a similar chart.

It highlights the CHANGE of home values vs. income.

At first glance, you can see that there is a long-term divide taking place. That is concerning.

But look closer. Inside the red circles.

Any time that gap accelerates quickly, home prices fall. In 1980, 1990 and 2006.

And what just happened? Once again, the fourth gap accelerated.

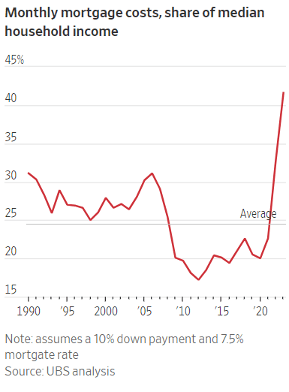

Red Flag #3: Mortgage Rates Are at a 23-Year High

This one is simple.

The Federal Reserve has raised interest rates at the fastest pace in history. They’ve stated that they will keep rates at this level for a while to fight back inflation.

In turn, 30-year mortgage rates are at a 23-year high.

And this ties into the previous two charts. It’s a big reason why housing affordability is so low.

A $500,000 mortgage on that new home just went from $2,000 to $3,500.

That’s a big difference.

The monthly cost of a new mortgage is now 42% of the median household income … higher than 2006!

This chart from UBS paints a pretty alarming picture.

To be clear about this … the Federal Reserve, arguably the most powerful economic agency in the world, has promised a “reset” in the housing market. They want prices to cool off.

Those are the three big red flags.

But Aaron, if this is the case, why do prices keep going up?

Ironically, you can thank the Federal Reserve for that.

As they increased interest rates to tame inflation, they created inflation in the housing market. Due to higher interest rates, homeowners who once bought their house with a 3% mortgage, can’t sell.

If they were to move, they’d have to start over … with a 7.5% mortgage rate. That’s a big hit.

Therefore, there is very little inventory. The lowest in 20 years.

Yet, there are millions of millennials who, now that they have enough money, are looking to buy.

Low supply + big demand = higher prices.

So, Are We in a Bubble?

Yes. We are in a real estate bubble.

I can’t say that there will be some massive crash like we had in 2006. That’s because it’s impossible to predict what the Federal Reserve will do with interest rates.

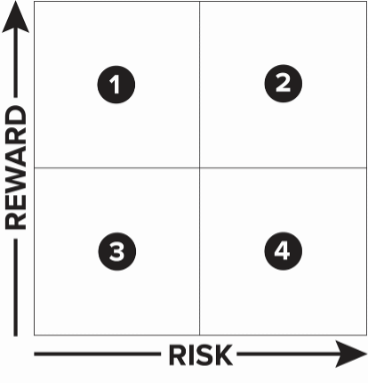

But I will say this. Right now, real estate is a “Zone 4” investment.

Due to all the red flags out there, real estate falls into the “High-Risk” Category.

And because of inflated prices, it is also “Low Reward.”

Nobody wants to invest in Zone 4 … “High Risk, Low Reward.”

I’ll invest in Zone 2 and Zone 3 from time to time.

But Zone 1 … that is the best place to be. Who doesn’t like a high reward with a low risk?

And here’s the good news. Because of the tumultuous market we are in, there will be more and more opportunities in Zone 1 over the next year. Amazing opportunities to make incredible returns with very little risk.

Next week, I’ll reveal one of my favorite Zone 1 investments … a bank that pays me a 19.59% dividend.

Aaron James

CEO, Banyan Hill Publishing and Money & Markets

P.S. I’d love to get your input. Will prices go down? Will they go up? Is now the time to invest? Click here to let us know in this short poll. We’d all love to know your thoughts.

Once you’re done taking the poll, please feel free to email me with your thoughts. My email address is aaronjames@banyanhill.com. I’ll share insight from the Banyan Edge community next week.