“What’s the stock market?”

If you’ve ever had a kid, you’ll know my preteen daughter wanted an answer now. Not three seconds from now. NOW.

Under such enormous pressure to impart professional expertise to my offspring, I told her it’s where people buy and sell shares in companies. Inevitably: “What’s a share?”

Eventually she had interrogated me to her satisfaction. But now I had questions.

Every day, I use the S&P 500 as a shorthand for “the stock market.” Like most major indexes, the S&P 500 is weighted by the value of each company’s total shares outstanding. That means it assigns a proportionate weight to each of its constituents with giants like Apple Inc. (Nasdaq: AAPL) having the greatest influence on the index.

But why, Daddy?

The reality is that an index-based exchange-traded fund (ETF) using market-cap weighting is a highly concentrated portfolio of ultra-mega-cap companies. In traditional S&P 500 ETFs, like the SPDR S&P 500 ETF (NYSE: SPY), Apple’s 3.89% weight is larger than the bottom 100 components combined.

That means SPY, or any other traditional index-tracking ETF, is skewed toward moves in mega-cap stocks.

Why should we consider that top-down approach to be “the stock market?” And what would happen if we didn’t?

Playing With Weights

Over the past decade, investors have been pouring money into index-based ETFs. These typically hold the stocks in the underlying index, ranked by their size.

But did you know that most of the time, the largest stocks tend to perform worse than the average stock in their sector? Historically, the biggest firm in any given sector underperforms the average stock in that sector by 3.5% a year over time.

Scaled up to the level of an entire index, that discrepancy means you might be missing a lot of gains if you stick with plain-vanilla ETFs like SPY.

What happens if you change the weighting of the stocks in an index?

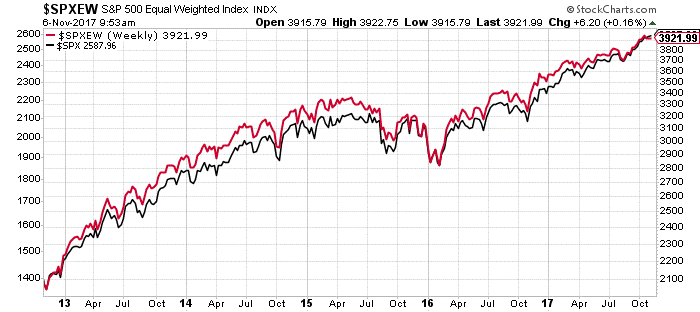

The chart below shows the normal S&P 500 (black line) compared to an index that weights each company equally (red line) — i.e., 0.2% to each company regardless of size.

From 2013 to July this year, the equal-weighted index beat the S&P 500 almost all the time. In fact, if you’d invested $10,000 in an equal-weighted index ETF in 2003, you’d have earned 33% more than a conventional ETF like SPY by now.

Equal-weighted indexes like the Guggenheim S&P 500 Equal Weight ETF (NYSE: RSP, above) have been around for a while. But now someone wants to go even further and launch a reverse-weighted ETF.

Even Stranger Things: The Upside-Down ETF

The Reverse Cap Weighted U.S. Large Cap ETF (NYSE: RVRS) launched last week. It holds all the components of the S&P 500 but flips their weighting, so that the proportions of its components are determined by the inverse of their relative market capitalization. Apple is the largest stock in the S&P 500, but it is the smallest component of the new fund.

By contrast, the smallest stocks in the S&P — Navient Corp. (Nasdaq: NAVI), Chesapeake Energy Corp. (NYSE: CHK) and Patterson Cos. Inc. (Nasdaq: PDCO) — are the largest components of the fund. Combined, they are worth just 0.4% as much as Apple.

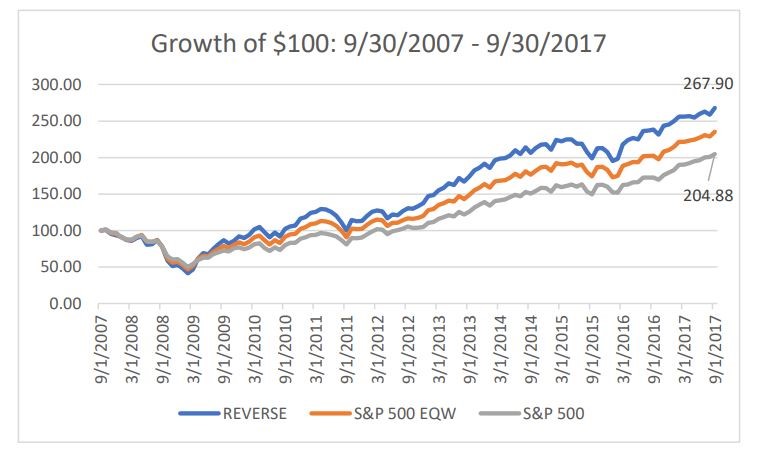

In back testing, this “upside-down” ETF outperformed both the normal S&P 500 and an equal-weighted model over the last 10 years.

What’s It For?

If you follow the ETF industry as I do, you’re probably tempted to think that the guys who design these things are running out of ideas. C’mon … an upside-down ETF?

But the back testing figures don’t lie. Both the equal-weight and the reverse-order ETFs beat the market over time.

But that’s the operative term: over time. ETFs like the new reverse-weighted RVRS are designed to take advantage of known relationships between variables over longer periods. RVRS outearns conventional indexes because, as I said above, large caps typically underperform smaller caps over time. The reverse is therefore also true.

Respect the Fourth Dimension

Allocating part of your portfolio to a proven, time-based strategy like alternative-weighted index ETFs is essential. The tested long-term relationships underlying them practically guarantee they will beat the market. They won’t win every month, but they’ll safely generate excess returns over time.

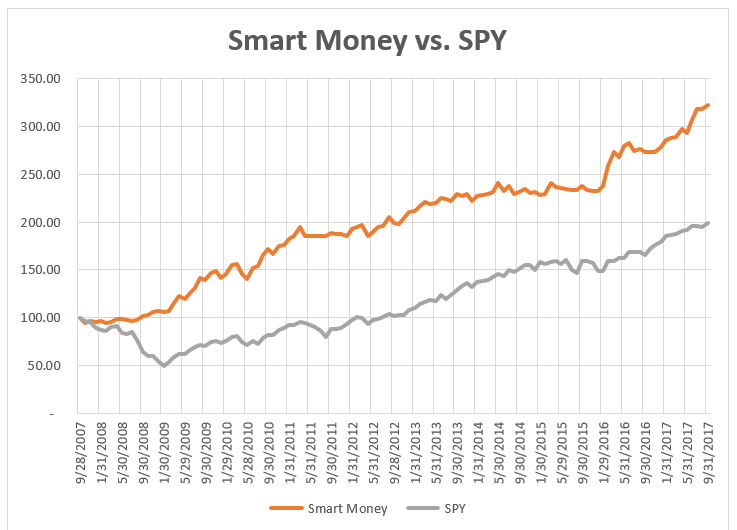

But there’s another strategy using time-tested statistical relationships that can achieve that same level of safety with even greater returns over time. It’s called the Smart Money system, and it’s part of my monthly Bauman Letter newsletter.

Besides the underlying mechanics, the big difference between the Smart Money system and these alternative-weighting ETFs is that Smart Money beats the S&P 500 over time … and in the short term. For example, the Smart Money system is up 24% this year versus just 16.7% for the S&P 500.

Over the last 10 years, Smart Money’s returns were 125% higher than the S&P 500. That’s waaaay higher than the excess gains from the alternative-weighting ETFs.

So, if you’re interested in achieving solid, safe, long-term gains that beat the market, by all means play with alternative-weighting ETFs.

But if you want to do that and make serious money, follow the Smart Money system.

Kind regards,

Ted Bauman

Editor, The Bauman Letter

Editor’s Note: Our beta testers — over 1,500 people from across America — had the opportunity to grow their money with Ted’s Smart Money system for 12 full months … and they love it! Perhaps best of all, this system is so effortless that it only requires 10 minutes of your time each month. To see why Smart Money is so straightforward that a 12-year-old can use it, click here.