Over the Labor Day weekend — when he wasn’t supposed to be laboring — Clint Lee sent me a fascinating chart. It shows the level of insider stock purchases in the broad technology sector:

(Click here to view larger image.)

The trend is clear. When the market starts getting “toppy,” insiders at technology companies stop buying their own shares. They resume in a pullback, like in 2018 and 2020.

Corporate executives know what’s going on in their industries better than anyone else. Every quarter, they must tell the market what they think about their own prospects in an official filing.

But they can buy and sell shares in their own company at any time. That makes insider purchases a critical data point for investors.

Look at the bottom right-hand corner of the chart. That’s the lowest level of insider buying over the last five years.

This is powerful evidence of something I’ve been saying all summer. I said it again in my weekly YouTube video on Friday last week.

Right now, smart investors should be buying quality companies. That means strong balance sheets, recession-proof revenues and above all, strong free cash flow.

Here’s the evidence.

Flight to Quality

One thing you can be sure of in a low interest-rate environment is that when people sell shares in one group of companies, they’re going to use the cash to buy shares in another group. Parking it in bonds is out of the question.

That dynamic has made so-called “rotations” — when money sloshes from one part of the market to the other like bilge water in an old ship — much more powerful over the last decade.

That’s why staying on top of these rotations is such a critical task.

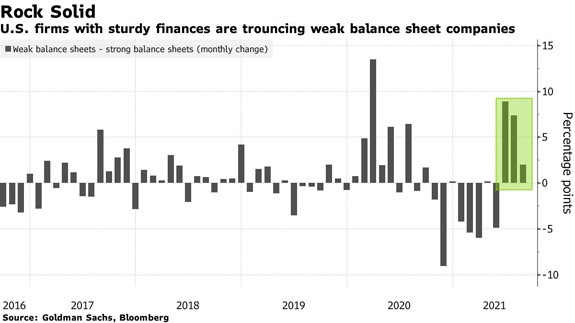

In the first quarter of this year, companies with weak balance sheets outperformed quality companies by over 20% — the biggest gap since 2006. Companies with shaky credit like Expedia Group Inc., Alaska Air Group Inc. and Carnival Corp. were the star performers. The assumption was that the economy was about to reopen, and with trillions in federal spending on the way, the economy would rocket.

Things are very different now.

Over the last three months, quality companies have outperformed their weaker brethren:

(Click here to view larger image.)

For example, in the third quarter, Adobe Inc. jumped 14%. Costco is up 17%. Alphabet rallied 18%.

I can’t know for sure, but I’d be willing to bet that some of the money generated by insider selling at growth-stage tech companies helped generate those gains.

Switching Gears Midcycle

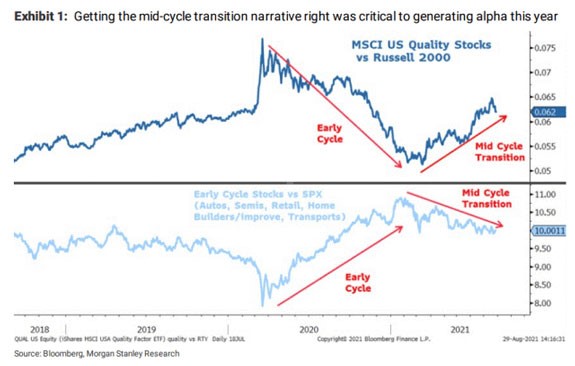

Morgan Stanley’s research department has been pushing the idea of a “midcycle transition” for most of the summer. The chart below shows this in action:

(Click here to view larger image.)

In the early part of this cycle, two groups of stocks outperformed:

- Companies with relatively weak financial positions, represented by the Russell 2000 Index, outperformed quality companies.

- Stocks that tend to do well when the economy is recovering outperformed the S&P 500 as investors anticipated the economy’s grand reopening after COVID-19.

As the chart above shows, however, those two trends changed sharply toward the end of the first quarter. Quality stocks now outperform more speculative plays, and reopening stocks are falling compared to the broader market.

Tortoise and Hare

The rotation back to quality companies this summer is part of a longer trend.

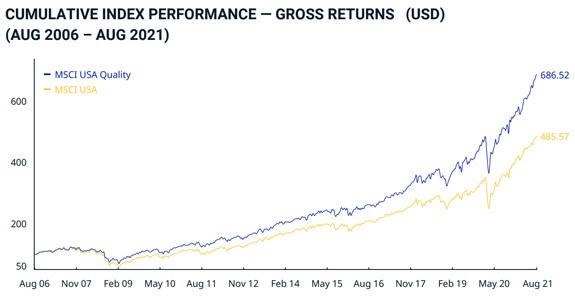

The chart below shows the three-year relative performance of the iShares MSCI USA Quality Factor ETF (BATS: QUAL) and the Russell 2000:

- Over the period, quality outperformed more speculative growth companies.

- Quality stocks are less volatile. They fell by much less than small-cap growth stocks in March 2020. They didn’t participate in the huge run-up in growth in the last quarter of that year or in the first quarter of this year … instead quality just kept grinding higher:

(Click here to view larger image.)

Quality stocks are the tortoise to growth’s hare. That’s because, over the long term, strong balance sheets tend to outperform weak balance sheets:

(Click here to view larger image.)

That’s because quality companies are attractive in all market conditions.

Nervous about a sell-off? Move to quality.

Think the economy is going to improve? Interest rates might rise, so buy quality companies with low debt.

Worried about recession? Strong balance sheets and cash flows help companies survive no matter what.

I’ve been targeting quality companies all summer in The Bauman Letter.

If you want a taste of what investing in quality can do for you, check out the iShares MSCI USA Quality Factor ETF (BATS: QUAL).

Kind regards,

Ted Bauman

Editor, The Bauman Letter

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}