I’ve emphasized the centrality of U.S. government policy to your investments for 18 months.

Whether it’s the Federal Reserve, stimulus payments, infrastructure bills or the fight against COVID, what the public sector does has had an outsized influence on stock prices.

In theory anyway, the people making those decisions are accountable to us as citizens, taxpayers and voters.

But the last few weeks show that decision-makers who aren’t accountable to anyone can have a far greater impact.

At the end of August, Chinese Premier Li Keqiang said his government would “work to stabilize commodity prices.” It would sell stockpiles of iron ore to push down its price, and order steel producers to cut output. This was the effect on global iron ore futures:

(Click here to view larger image.)

Stocks of ore miners have collapsed, with BHP and Rio Tinto down 12% in the past week. U.S. investors who bought those stocks in anticipation of a U.S. infrastructure deal are getting crushed.

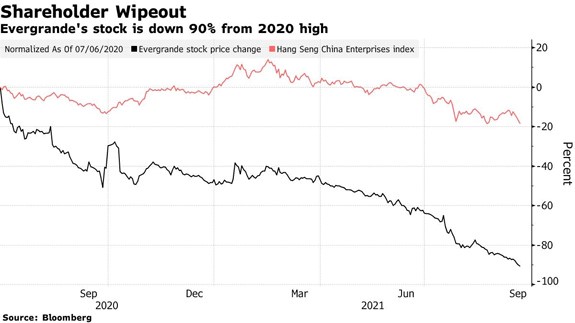

Today, September 20, a much bigger group of U.S. investors learned just how vulnerable we are to the whims of the Chinese Communist Party:

(Click here to view larger image.)

Folks, like it or not, your investments and your future prosperity are at the mercy of a small group of unaccountable policymakers on the other side of the planet.

And there’s only one thing you can do to take it back from them.

Another Asian Contagion

Over the weekend, Chinese property giant Evergrande told creditors and investors it can’t make cash interest payments on its $300 billion liabilities, 6% of total Chinese real estate debt.

In desperation, it offered them real estate in lieu of payment.

That was probably worse than default.

Evergrande’s stock price collapsed … and on Monday, so did global stock markets. Ordinary investors like us are suffering.

The only thing we can do is to try to make sense of this debacle … and learn from it.

The starting point is the role of real estate in the Chinese economy.

Including the construction sector, the Chinese real estate sector makes up 30% of that country’s gross domestic product (GDP).

That is an extraordinary figure. It’s nearly double the figure for Japan in the late 1980s, before its own property bubble collapse, which led to two decades of economic stagnation. It’s three times the level reached in the U.S. prior to the great financial Crisis, followed by a decade of subpar growth.

But that’s only part of the problem.

Ever since the Communist Party allowed semi-ownership of private residential property in the late 1990s, ordinary Chinese have invested in apartments to secure their nest eggs:

(Note the empty parking lots.)

Millions of Chinese households give developers full down payments on apartments in the planning stage. Most never occupy them, holding them as speculative assets. The reseller market for these apartments is frothy. Chinese home prices have surged sixfold over the past 15 years, making cities such as Shenzhen less affordable than London.

That spurs developers to build even more apartments.

But there’s another piece of the puzzle. In China, the state owns all land. To pad their budgets, Chinese local authorities sell rights to urban land to developers at discounted prices.

Low land costs plus spiraling home prices boosted developers’ margins rapidly over the last decade. That sent the shares of Chinese real estate companies into the stratosphere. Hundreds of millions of Chinese own those shares. Investors all over the world own their bonds.

3 Red Lines

This is obviously unsustainable.

The problem is that the Chinese Communist Party encouraged this real estate boom to spread the illusion of prosperity to ordinary Chinese.

To dial things back a bit, last year the Party issued a “three red lines” financial policy for property developers:

- A 70% ceiling on liabilities to assets, excluding advance proceeds from projects sold on contract.

- A 100% cap on net debt to equity.

- A cash to short-term borrowing ratio of one or less.

The effect was akin to telling an Olympic sprinter that they could only run on one leg.

Deprived of their favorite financial engineering tricks, developers like Evergrande had to scale back production. That reduced the cash flow available to make payments on their debts.

It also enraged buyers whose apartments had not yet been delivered … and led to a collapse in Evergrande’s share price:

(Click here to view larger image.)

Without the opportunity to issue new shares, cut off from new credit, and with investors clamoring for their properties, Evergrande approached the end stage earlier this month.

Ripples in the Global Financial Pond

Investors fear a disorderly collapse of Evergrande’s position could cause global knock-on effects:

- Chinese stocks: Chinese apartment buyers and stock investors could get only a tiny fraction of their investments back. That could lead to lack of confidence across the sector, and in Chinese financial markets more broadly. That, in turn, could lead to a huge withdrawal of liquidity from companies that have so far escaped the government’s crackdown, like electric vehicle and solar manufacturers. We are seeing that today, with declines of 6% to 10% in such stocks.

- Credit contagion: Many Chinese banks and quasi-banks are exposed to Evergrande and its customers. A collapse could lead to forced restructuring or outright failure. That would reinforce the liquidity problem above. But it could also cause a crisis in emerging markets, where exposure to Chinese junk bonds is particularly high. In 1998, for example, credit market problems in Thailand led to a global financial crisis. China is many orders of magnitude larger than Thailand’s market ever was.

- Withdrawal of state support: Many Chinese companies — including those favored by global investors — have benefited massively from state support. But most is from regional and local governments. If Evergrande were to fail or its debt liquidated at low recovery rates, those governments would be reluctant to support Chinese companies again. That could lead to ratings downgrades for those companies and their debt, as the assumption of state backing evaporates.

- Forced deleveraging: The biggest risk of all is that the Chinese government repeats Japan’s mistake in the 1990s of not reining in excessive credit and shutting down insolvent borrowers quickly enough, causing long-term damage to growth in the world’s No. 2 economy. That could have a devastating impact on companies all over the world.

Choose This Safe Port in the Storm

China’s rulers guided it to global economic power through a complex web of policies designed to create the illusion of financial prosperity. The one thing the Chinese government fears above all is a collapse in its legitimacy if it cannot deliver the good life to its subjects.

That’s not so different from what’s happened in the United States since the great financial crisis. Congressional bailouts and Fed quantitative easing policies have basically the same goal. The only difference is that in the United States, politicians’ primary constituency is Wall Street, not ordinary people. (If you doubt that, read this.)

The bottom line is that a big chunk of global equity markets is a house of cards. It depends on government policies, both at home and abroad, over which we have little control.

The best way to protect yourself from the revealed risk in this situation is to load your portfolio with precisely the sort of quality companies I recommend in The Bauman Letter.

I’ve been loading up on such companies since spring, anticipating a “black swan” event like this. Amid today’s rout, 11 out of the top 12 best-performing stocks in The Bauman Letter model portfolio came from that lot.

And wouldn’t you know it … of the 30 stocks in the Dow Jones Industrial Index, next month’s pick is the only one that saw a gain today!

Kind regards,

Ted Bauman

Editor, The Bauman Letter

{kind=link}

{kind=link}

{kind=link}