Recently, a Bauman Letter subscriber told me:

“Ted, the thing I like most about your service is that most analysts focus on the history of the market. You focus on the history of what drives the market.”

That’s an important distinction.

You can certainly profit by using a stock’s price history to spot opportunities.

But in times of major upheaval, like today, “technicals” are a poor guide. Normally, reliable information on the history of individual assets is overwhelmed by external factors.

In this case, I prefer to focus on the Big Picture.

And right now, the Big Picture is telling me to be opportunistic … but to let someone else do the work.

Where You Are (and How You Got Here)

The roots of today’s market pullback lie in the late 1980s.

That’s when the Reagan administration began to dismantle the regulatory framework that stabilized the U.S. financial sector since the Great Depression.

It’s also when Federal Reserve Chairman Alan Greenspan introduced what’s become known as the “Fed put” — an implicit promise to backstop financial markets no matter what.

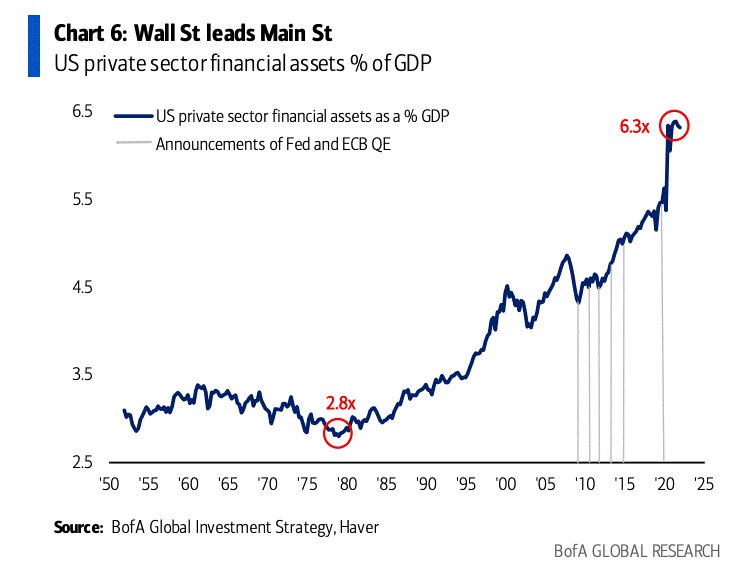

The result was to increase the proportion of financial assets — stocks, bonds, debt, derivatives and other paper claims on real wealth — in the U.S. economy:

(Click here to view larger image.)

Increasing the proportion of financial assets in the economy lowers the cost of accessing money. Cheap money encourages speculation.

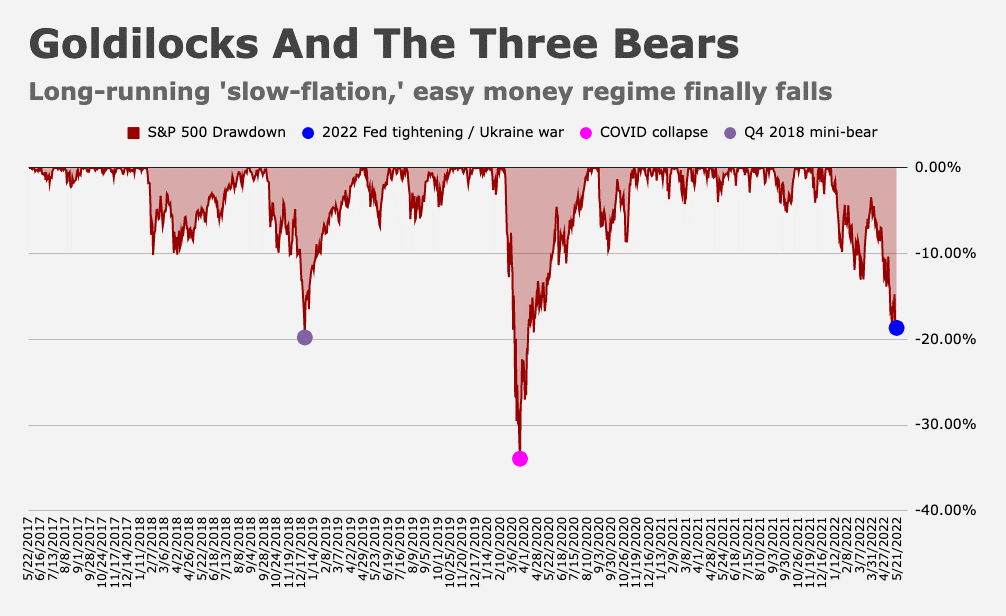

We can see the proof in a backward way. The two biggest stock market drawdowns in the last decade (other than the V-shaped COVID crash) happened when the Fed started raising the cost of accessing money:

(Click here to view larger image.)

In 2018, the Fed caved under pressure from Wall Street.

It’s been VERY clear that it’s not going to do that again this time.

As I’ve argued, the Fed’s newfound hawkishness isn’t just about inflation.

The Fed wants markets to return to a pre-quantitative easing situation. It wants investors to value stocks on their earnings potential, not on a flood of easy money to blow in a “casino” market.

That’s why 2022’s equity sell-off is all about derating. Most stocks are falling not because their business prospects have declined, but because their elevated price-to-earnings (P/E) ratios only made sense in a casino market.

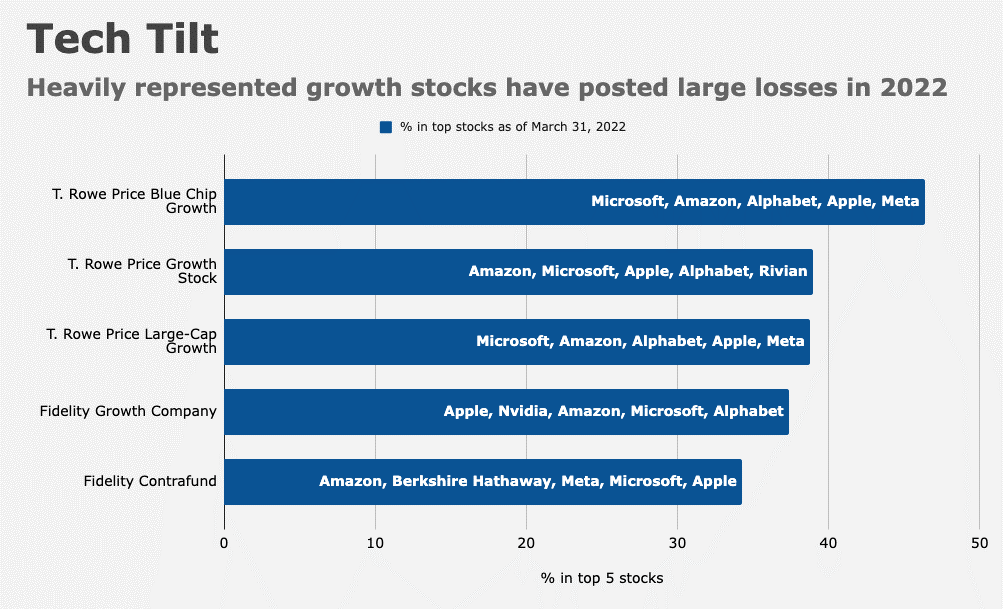

Unfortunately, stocks that experienced the biggest “casino” gains are popular in leading 401(k) retirement savings plans … maybe yours.

For example, at the end of the first quarter, the T. Rowe Price Blue Chip Growth Fund was heavily invested in Microsoft (Nasdaq: MSFT) (11.6%), Amazon (Nasdaq: AMZN) (10.9%), Alphabet (Nasdaq: GOOGL) (10.2%), Apple (Nasdaq: AAPL) (8.7%) and Meta (Nasdaq: FB) (5%). The fund is down 32.5% so far this year:

To summarize: Stocks went up because the Fed kept flooding the “market casino” with free chips. Now it’s calling them in.

That’s what’s putting the hurt on your portfolio.

Where You’re Going

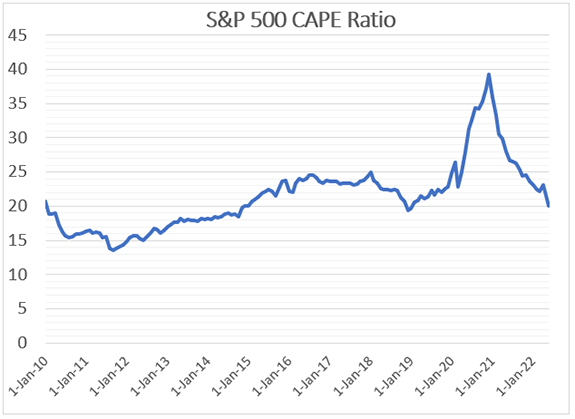

At some point, derating is going to stop. We’ll get back to P/E ratios that make “sense” in terms of actual company earnings.

You could argue that we’re already there:

But that’s not necessarily the end of the pullback. The same medicine that causes derating — financial tightening — can also cause recessions.

This is where history tells us a lot more than technical numbers.

The median postwar drawdown during recessions is 24%. We almost hit a 20% drawdown on Friday…

Which led some people to claim that recession is already baked into stock market prices.

But recall that the current drawdown is about derating sky-high P/E ratios as we move out of a Fed-induced casino market.

A stock market decline due to a recession would be on top of that.

But let’s say some recessionary anticipation is already priced in. Further price declines would come from falling earnings, like those we’ve seen from Walmart (NYSE: WMT), Target (NYSE: TGT), Kohl’s (NYSE: KSS) and other retailers recently.

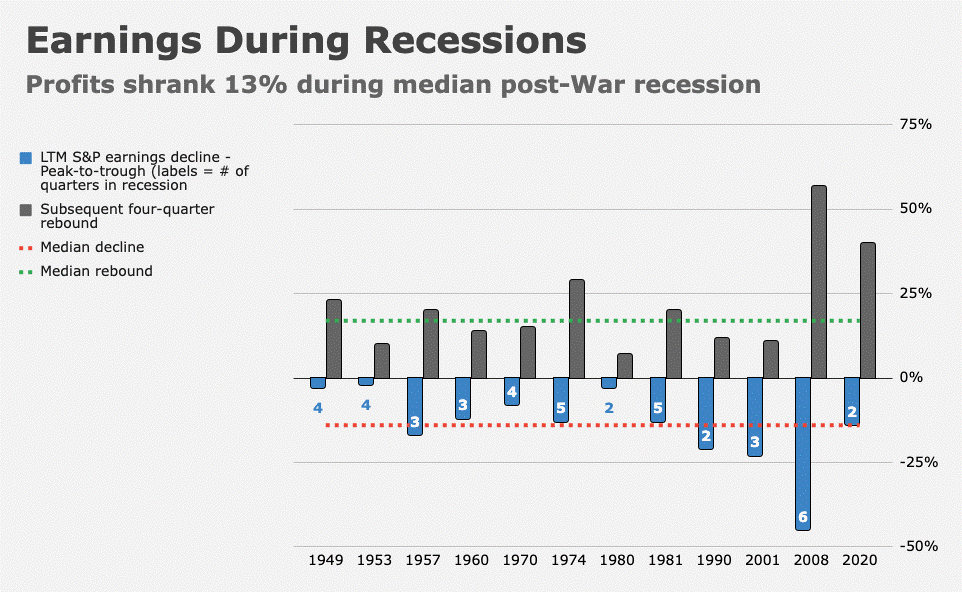

Again, history is a good guide. In recessions since World War II, corporate profits have shrunk by an average of 13%:

To summarize: If the Fed does tip the U.S. economy into a recession, the market could fall by another 10% to 20%.

Hang on to your long-term investments. But don’t expect a big rebound anytime soon.

What You’re Going to Do About It

A falling market involves three things:

- Stock prices fall.

- Volatility increases.

- Stock prices rise again.

One way to position for that is by “selling volatility.” It’s an options strategy and it exploits the fact that volatile stocks attract higher premiums, which erode as their exercise date approaches.

It’s not a play on rising stock prices. As I explained, that’s not going to work right now.

Instead, the goal is to generate income by selling options at a high premium and buying them back at a lower premium just prior to expiry. The strategy works particularly well in declining markets.

But you don’t need to worry about doing that yourself. Instead, you can buy an exchange-traded fund (ETF) that follows this strategy.

ETF managers buy exposure to stocks in an index such as the S&P 500 and sell covered call options on the same index. They exploit volatility to generate income as options premiums rise closer to expiry.

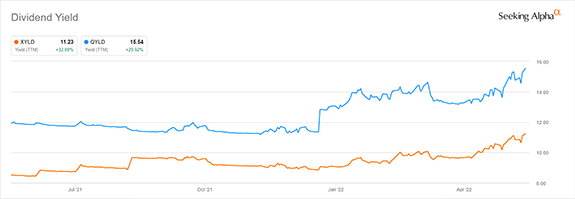

The Global X S&P 500 Covered Call ETF (NYSE: XYLD), for example, is currently paying a dividend of over 10.4%, paid monthly. The Global X Nasdaq-100 Covered Call ETF (Nasdaq: QYLD) pays 15.6%.

Due to the nature of the strategy, these dividends change month to month. But the trend is definitely up:

So, if passively earning a dividend yield anywhere between 50% and 100% more than the inflation rate sounds like a good idea to you in the year 2022, you know what to do!

Kind regards,

Ted Bauman

Editor, The Bauman Letter

{kind=link}

{kind=link}