Americans sport a record $1.3 trillion of auto loan debt.

That amount has grown by 54% in the past 10 years — second to student loan debt, which grew by 75%. Other forms of consumer debt shrank in the same period.

Auto loan delinquencies measure loan payments that are more than 60 days past due. They came in at normal levels in March and April.

That feels reassuring since the economy was shut down in April, and millions lost their jobs. It seems that delinquencies aren’t spiking. That should be good news.

But don’t be fooled … And don’t invest in these companies just yet.

Borrowers in hardship rose fivefold from March to April. Hardship includes deferred payments, frozen accounts and frozen payments. They may not be delinquent, but they will be soon.

Stimulus checks and unemployment benefits are helping keep these numbers down. But that’s only temporary relief.

The auto lending industry is not in a recovery.

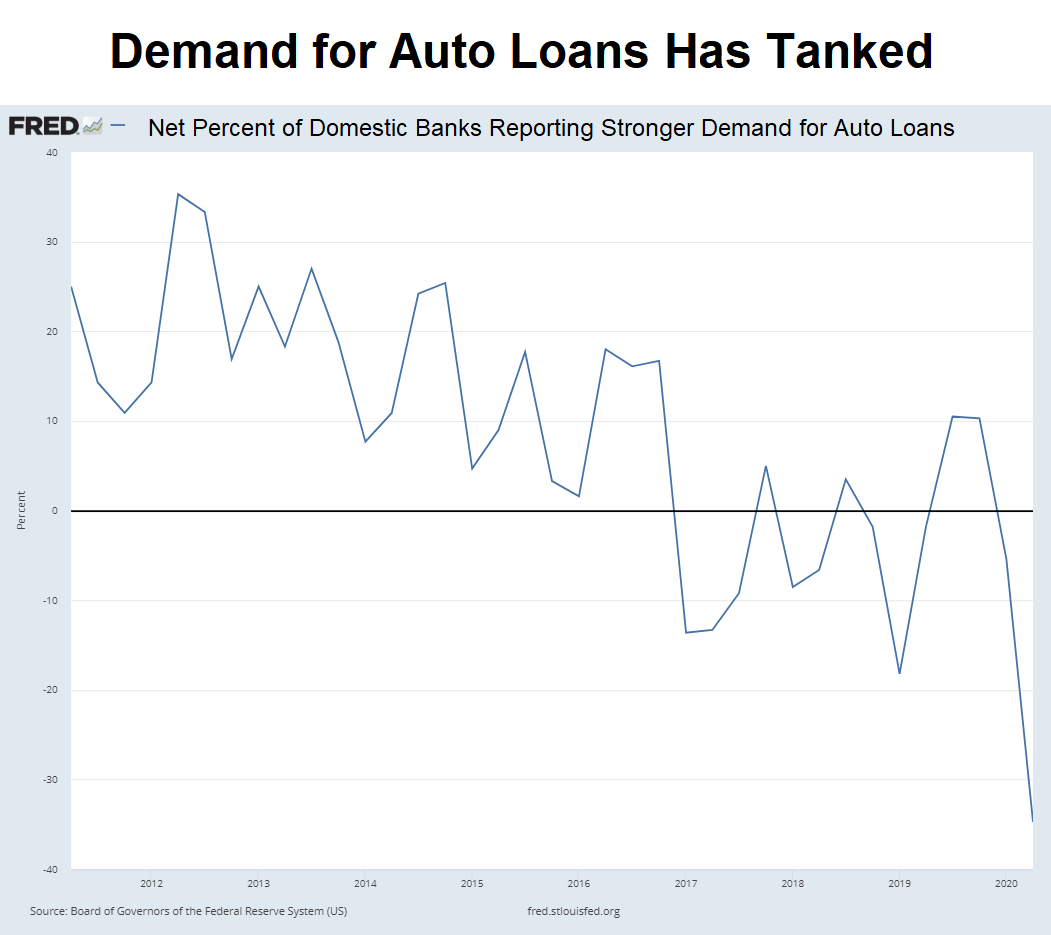

Banks have reported a severe drop in the demand for car loans.

That’s no surprise with stay-at-home orders in place and surging unemployment.

It’s a bad sign for companies devoted to automobile financing. They won’t be making as many loans. They make their money from the interest and fees on those loans. Fewer loans mean less revenue for them.

And it’s only half the battle.

Because there is trouble ahead for these companies’ outstanding loans.

Stocks tied to the riskiest part of this industry have been bouncing with the broad market … But it’s not time to buy in.

Subprime Car Loans Are a Ticking Time Bomb

Things were turning south for auto lending even before the year started and the pandemic set in.

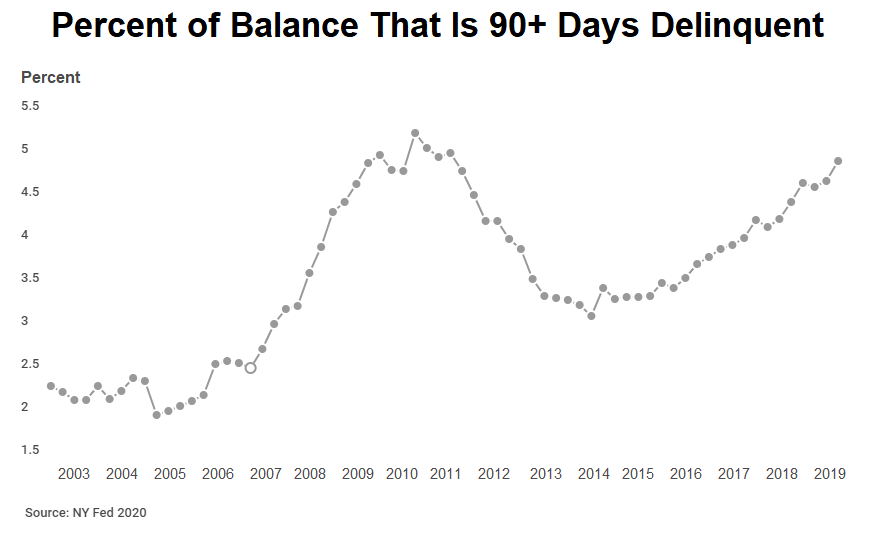

In the fourth quarter of 2019, delinquencies reached its highest level since 2011. That was when consumers were emerging from the throes of the 2008 financial crisis and recession.

There are more than 83 million outstanding car loans in the U.S. And subprime borrowers — those with credit scores below 670 — account for 22% of those loans. That’s more than 18 million loans, covering roughly $286 billion.

These 18 million borrowers are most vulnerable to financial hardship in recession. And they’re the most likely to miss or skip payments.

They’re also more likely to be victims of predatory lending. In other words, they get slapped with a loan that is way larger than the value of the car and hard to pay back.

Subprime borrowers are good for auto lenders when they’re making payments on interest-heavy loans. But not when they quit paying. For example, one company we mention below reported a first-quarter credit loss expense of $908 million. That 64% higher than the year-ago quarter. That’s the money the company has to put aside for expected delinquencies. That number only factors in pressures that appeared through the end of March. The second and third quarters will be much worse.

Which brings me to the stocks to stay away from.

Don’t Buy These 2 Auto Lenders’ Stocks

Santander Consumer USA Holdings Inc. (NYSE: SC) is a consumer finance company that serves the retail vehicle industry. It provides loans for car purchases and car dealers’ infrastructure and capital needs. Santander is the company I mentioned above, it lost $908 million in just the first quarter of this year.

A group of states accused Santander Consumer USA of malpractice in subprime lending. The company was stepping over the lines of basic consumer protections. The company agreed in May to pay $550 million to settle.

This wasn’t the first time Santander Consumer USA was called out for shady practices. The company faced similar challenges from state attorneys and the Federal Reserve in 2015, 2017 and 2018.

Saddling consumers with unreasonable loans will come back to bite this company.

Delinquencies will rise now that there’s more pressure on vulnerable borrowers.

Credit Acceptance Corp. (Nasdaq: CACC) will also feel the recession bite down.

Credit Acceptance is the second-largest auto-focused lender. It’s also a collections agency.

During normal times, this company hums along with solid fundamentals.

But these aren’t normal times.

Its ability to collect on loan money has fallen to 64.8%, a 10-year low.

It’s also losing market share in lending. Loan volume at its dealership partners is down. And so is the growth in dealers it’s partnering with.

The demand for car loans is falling. Borrowers will miss more payments. Unemployment benefits and stimulus checks will dry up.

It’s not a good situation for Credit Acceptance and Santander Consumer USA.

Don’t buy into stocks like these.

There are tough times ahead for this industry.

Good investing,

Editor, Apex Profit Alert