Recently, someone I follow on Twitter recounted how a friend had invested some money for his child. He expected an annual average return of 16% on that investment. He based this on the compound annual return of the total U.S. stock market over the last decade.

There’s only one problem: Past performance is no guarantee of future returns.

If you extend the stock market’s average return back 20 years, for example, it falls to 9.8%. That’s consistent with the long-term average over the last 200 years.

To anyone whose stock trading experience spans the 12 years since the Great Financial Crisis (GFC), that may seem disappointingly low.

But those 12 years are exceptional.

Only one of them produced a negative return — 2018. Even then, the Federal Reserve Chairman Jay Powell-induced crash in the fourth quarter of that year immediately reversed in 2019, when the market rocketed 31.5%.

Over the last two centuries, on the other hand, one out of every four years produces a negative return.

That raises an important question for all investors.

On what are your expectations for the next decade based? Could they be leading you into a trap?

The Law of Long-Term Averages

Repeated experiments prove that most of us think the future will be like the recent past.

At one level, that’s a sensible assumption. Most of the time, change happens incrementally. That means we can “see it coming.”

One thing we can’t see coming is so-called “black swan” events. These are inherently unpredictable happenings, like the GFC or COVID-19.

Of course, some people warned beforehand that such things could happen. For most people, though, the probability was low enough that it didn’t make sense to plan on them.

But all this changes if you step back and look at things over a longer timeframe.

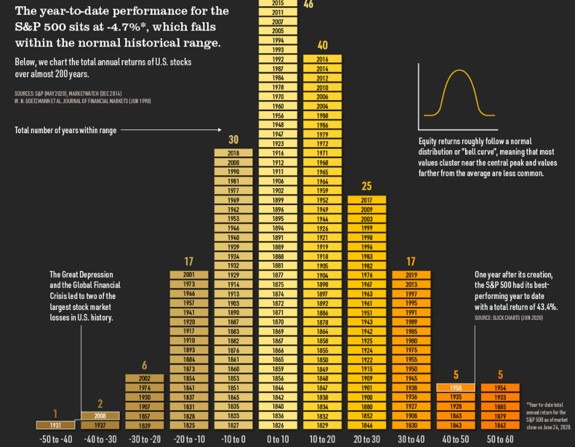

Earlier this year, the folks at Visual Capitalist published a chart of annual returns to U.S. stocks going back 200 years:

(Click here to view larger image.)

The biggest cluster of annual returns is between -10% and 20% a year. By contrast, the stock market saw annual gains of more than 20% only a quarter of the time. Negative returns happened 28% of the time.

Hidden in the data, however, is a revealing pattern.

Back-to-back decades of average annual returns over 15% are extremely rare.

Typically, decades where the annual average return exceeds that number are followed by decades of returns between 5% and 10%.

Well, Whaddya Expect?

That implies it’s dangerous to manage your portfolio on the assumption of above-average index level returns in the next decade.

Nevertheless, from the correspondence I get from my subscribers, it’s clear that many people expect just that. Based on the recent experience, they’ve come to see triple-digit gains as the norm rather than the exception.

This is unrealistic.

The chart below shows three ways of slicing the stock market going back to September 2002. The green line is the S&P 500. Red is the Russell 1000 Growth Index, the stocks with the most price momentum. Ruling them all is the orange Nasdaq 100, where the biggest technology heavyweights live:

(Click here to view larger image.)

The implication is simple. Ever since the Great Financial Crisis, a handful of mega-cap technology stocks have torn away from the rest of the market. Starting just before the COVID-19 crash, smaller tech companies began to pull away as well, accelerating that trend once Federal Reserve plunge protection policies kicked in.

Now, it is certainly possible that these trends could resume and continue over the next decade. But historically and statistically speaking, that’s highly unlikely.

Curb Your Enthusiasm? No.

That certainly doesn’t mean you should sell your stocks and cancel your subscriptions to financial newsletters. Quite the opposite, in fact.

The historical and statistical likelihood that big gains will be harder to come by in the near future simply means you’re going to have to work harder to find them … or pay someone else to do it for you. It just won’t be possible to hitch your wagon to a handful of companies growing at Apple, Google or Nvidia rates.

Here’s how I plan to deal with that.

First, I’m going to stick to the basic rules of investing. I’m not going to try to get rich quick by plunking everything down on a handful of stocks in the hope that they’re going to grow by triple digits in short order.

Second, I’m going to keep my portfolio well diversified. I’ll maximize my chances of beating the market by buying assets in different sectors, geographies and factor styles such as momentum, value and quality.

Third, I’m going to invest for the long term. Given the low likelihood of big annual jumps in stock valuations, I’m going to target a three- to five-year timeline for my investments, at a minimum.

Fourth — and most important of all — I’m going to anchor my portfolio around a group of companies that have the highest possible statistical likelihood of outpacing the market over the next decade. I’m going to prioritize companies in sectors that will grow regardless of what happens in the broader economy. I will choose those that pay solid and growing dividends and compound those dividends to increase my total returns.

That’s precisely why I’ve been recommending exactly such companies to Bauman Letter readers all summer! And why I will continue to do so.

Kind regards,

Ted Bauman

Editor, The Bauman Letter

{kind=link}

{kind=link}