A Goldilocks economy is not too hot and not too cold.

This is stolen from the line in the popular children’s story where Goldilocks describes the best temperature of porridge.

The term describes an ideal state for an economic system. Not too hot to cause inflation and not too cold to cause a slowdown in growth.

Under these Goldilock’s conditions, the market tends to stay in a bullish uptrend.

The term was first used by an unnamed government official in 1996.

The stock market was in the middle of an unprecedented boom because new technology like PCs and software had rapidly increased economic productivity.

This ideal Goldilocks state would keep the Federal Reserve on the sidelines, allowing it to keep rates lower for longer. It would also keep the stock market bears at bay.

Friday’s unemployment report, while less than economists expected, suggests Goldilocks might have found the perfect temperature for stocks…

This Isn’t a Normal Market

I checked the financial news headlines after the report, and it looked bad on the surface.

One, in particular, proclaimed: “August jobs report badly missed expectations with 235,000 payroll gain as the Delta wave slams hiring.”

Of course, this was in large font and boldface type.

If you read that, you might have dumped all your stocks. But the market barely flinched.

The S&P 500 closed the day flat while still up 0.5% for the week.

Indeed, U.S. businesses created only one-third of the jobs expected.

In a normal environment, investors might be worried about a forthcoming economic slowdown.

However, these aren’t normal times, and this isn’t a normal market.

COVID Might Be Doing the Fed’s Work

There was a sharp slowdown in hiring from July, which was revised to 1.1 million from 943,000 added payrolls. It was also the weakest month since January.

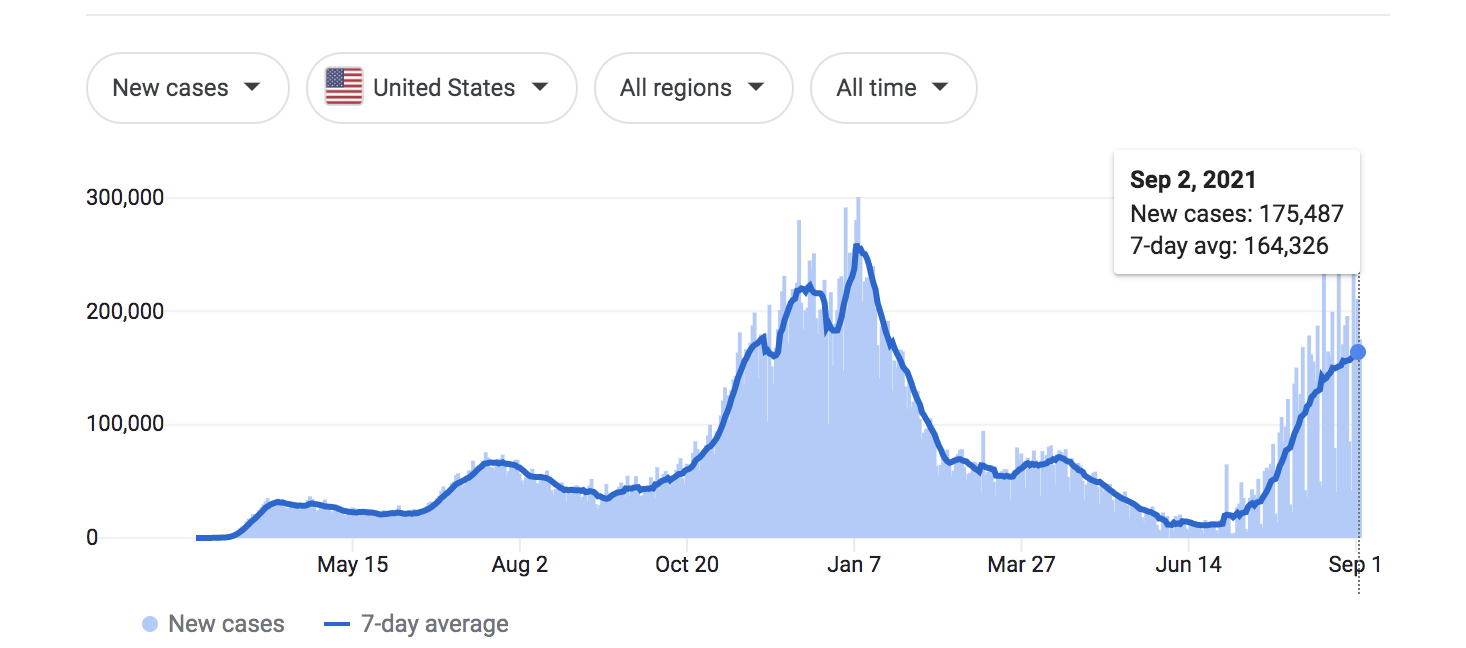

But the weak jobs number should have been expected. COVID cases have been on the rise since early July.

The seven-day average of 164,000 is nearing the peak reached in January.

There was a similar situation in December and January when the monthly payroll number dropped from its trend:

Eventually, COVID cases started declining, and payroll growth picked up again.

In a weird twist, these short bursts of COVID might be doing the Fed’s work.

We know the Fed is concerned about an overheating economy, and these short episodes of COVID seem to tamp the brakes on hiring.

In doing so, they prevent the economy from overheating. Not too hot and not too cold.

And, more importantly, they keep the Fed and the bears on the sideline.

Regards,

Editor, Strategic Fortunes