On Sunday morning, my wife and I watched The Big Short.

It’s about four hedge funds that shorted the U.S. mortgage-backed securities (MBS) market starting in 2005.

Everyone else assumed MBS were the safest investment on the planet.

As clueless Wall Streeters in the movie kept saying, “Who doesn’t pay their mortgage?”

But these guys did their homework. They quickly learned the mortgages in MBS were garbage.

Originators handed out adjustable-rate mortgages (ARMs) like Halloween candy.

Big banks packed them into MBS. They bribed agencies for AAA ratings. Then they sold them to unsuspecting investors.

The shorts predicted that when ARMs began to reset in the second quarter of 2007, the MBS market would collapse like a Jenga tower.

That’s exactly what it did. Their short bets earned them billions. The rest of the financial system collapsed.

All through the movie, I kept asking myself one question … where’s the opportunity for today’s Big Short?

The Big Bailout

Even if you only started investing in the last few years, the events in The Big Short still dictate your returns.

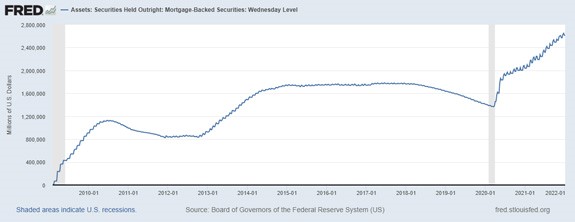

Starting in February 2009, the Federal Reserve bought trillions of worthless MBS from the banks whose corrupt dealings almost crashed the global economy.

Despite trying to unload some of this “toxic sludge” in 2018-2019, the Fed now holds almost twice as much MBS as it did when COVID started:

(Click here to view larger image.)

By bailing Wall Street out of its MBS folly — and keeping those junk assets out of the market for over a decade — the Fed altered the risk/reward relationship for asset markets of all kinds.

Above all, quantitative easing (QE) created TINA: there is no alternative.

If a free market had priced those MBS and Treasurys, the epic bull stock market of the last decade would never have happened.

Stock Market Kabuki

For 15 years, central banks and stock markets have performed an intricate kabuki dance.

Both know QE has distorted stock prices.

Both know QE isn’t supposed to be permanent.

Both know the other knows these things.

But since the Fed didn’t withdraw QE after Wall Street balance sheets recovered, the stock market became addicted to it.

If you take away an addict’s junk, the addict gets sick. That made the Fed nervous about withdrawing QE.

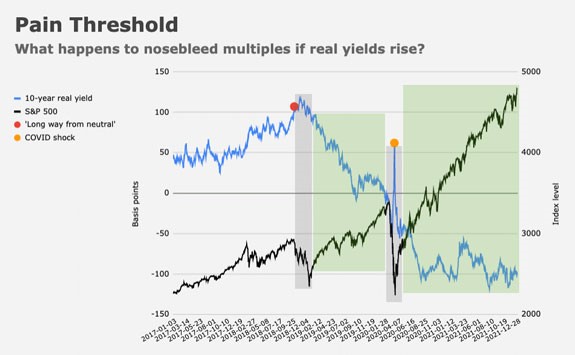

Indeed, every time the Fed started tapering, bond yields rose. Stock prices collapsed … especially highly valued tech and growth stocks:

(Click here to view larger image.)

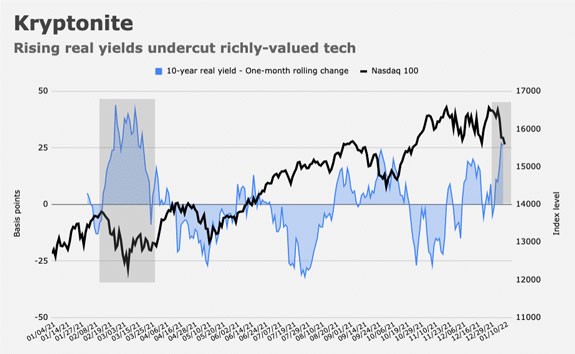

Over the last year, the inverse relationship between real yields and the Nasdaq 100 Index of top tech stocks has been extraordinarily close:

(Click here to view larger image.)

Exposing the Shorn Sheep to the Wind

A fortnight ago, Goldman Sachs predicted three interest rate hikes and Fed bond-selling in the fourth quarter.

Monday morning, it changed its prediction to four interest rate hikes and bond sales starting in March.

Ten-year Treasury yields reacted by spiking well above their previous peak during the last interest rate scare in April 2021:

(Click here to view larger image.)

The immediate cause of the Fed’s rediscovered hawkishness, of course, is consumer price inflation.

But as I argued in my Bauman Daily YouTube live Q&A video last week, the Fed is using inflationary concerns as an excuse to put the stock market addict into rehab.

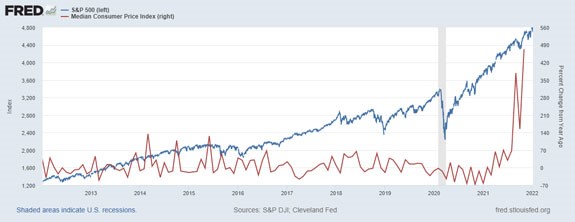

Recent decades-high inflation prints are a result of massive federal fiscal stimulus plus broken supply chains. Fed QE had little to do with it.

If you don’t believe me, look at the relationship between stock prices and inflation during pre-COVID QE. Unlike stock prices, consumer prices didn’t rise until Washington started handing out money:

(Click here to view larger image.)

The Little Short

I don’t think there’s a BIG short on offer in 2022.

But there certainly are plenty of LITTLE ones.

The price of overvalued growth stocks is inversely correlated to real bond yields.

Real bond yields are the difference between the nominal yield on a Treasury and the inflation rate.

We know that the Fed is going to be raising rates. It’s highly likely that economic growth will strengthen, and inflation will abate.

All of that will cause real yields to rise.

Ergo, stocks with high valuation multiples — especially price-to-sales (P/S) and price-to-earnings growth (PEG) — are good candidates for shorting this year.

For example, in the list below, there’s only one stock on which I would go long — Teladoc Health (NYSE: TDOC). That’s because its P/S is under 10, its PEG is under 1 and it’s got strong secular tailwinds that outlast COVID:

(Click here to view larger image.)

Although it also shows reasonable P/S and PEG, I wouldn’t go long on Coinbase (Nasdaq: COIN). It’s a derivative of crypto. A basket of common tokens and related companies is down 20% over the last month. COIN itself is down 12%.

You may recognize that list. It’s the top 50% of holdings in the Ark Innovation ETF (NYSE: ARKK).

In fact, comparing ARKK to the two top-performing “factor” ETFs (those that apply things such as momentum and value metrics to their holdings) over the last year speaks volumes.

The Pacer U.S. Cash Cows 100 ETF (BATS: COWZ) and the Invesco S&P 500 Pure Value ETF (NYSE: RPV) outperformed growth tech by 70% in the last 12 months. They contain companies that generate cash flow and trade at a decent valuation:

(Click here to view larger image.)

A famous economist once said that when the facts changed, he changed his mind.

I have a strong feeling a lot of stock market minds are going to change during 2022.

Kind regards,

Ted Bauman

Editor, The Bauman Letter

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}