It’s funny how Wall Street analysts love a stock when it’s overvalued….

And they hate it when the stock finally sinks to a reasonable price.

But that’s where we find ourselves with Beyond Meat Inc. (Nasdaq: BYND) these days.

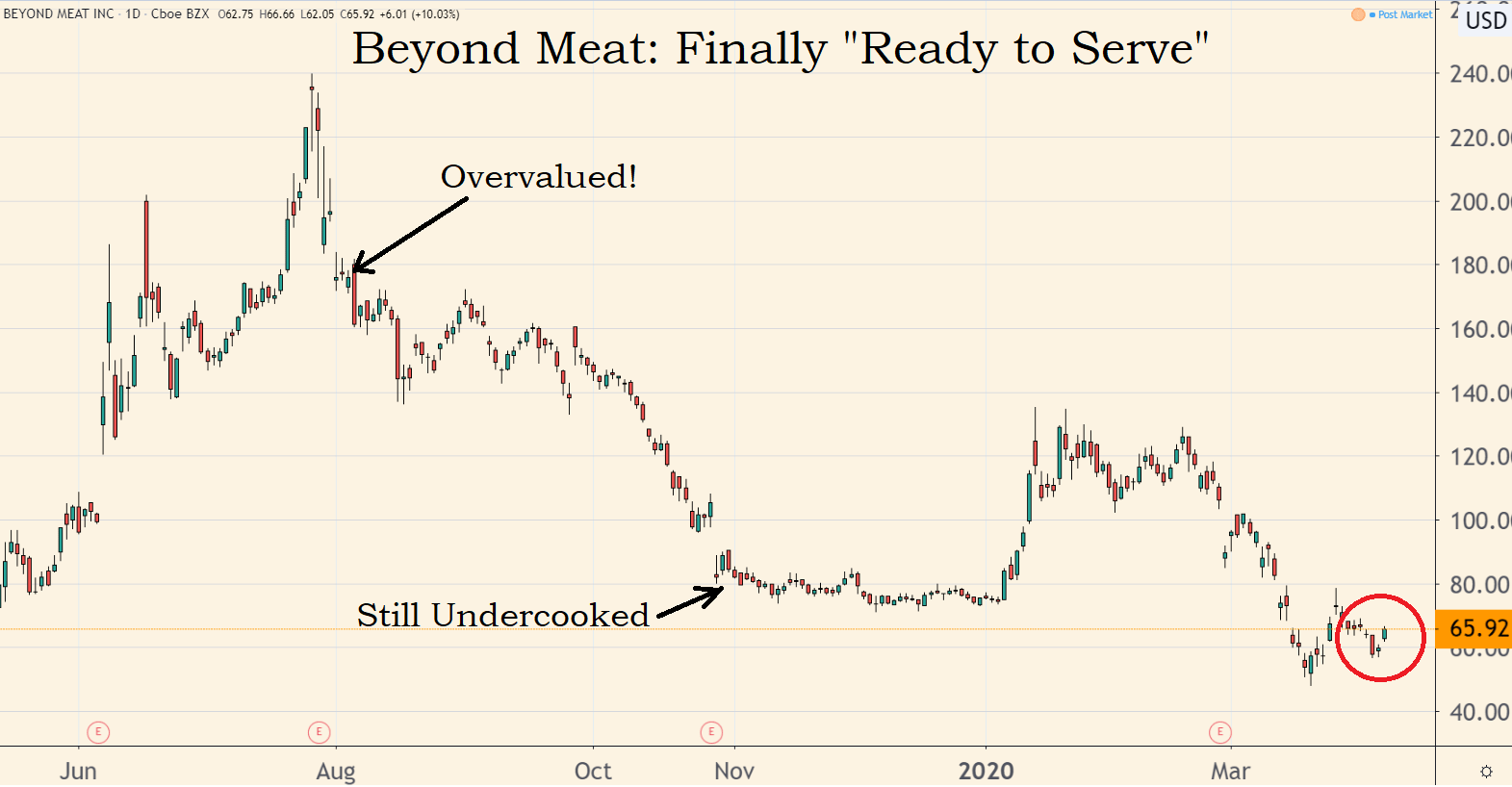

Just to catch you up — last August, with the stock at $174, I said to avoid the shares. Great growth prospects, but terribly overvalued.

By November the price fell to $79. Still too overvalued, I said. Wait ‘till it drops almost by half again, to $45.

Last week it hit $50.

Close enough, I say. This one’s cooked all the way through and ready to serve!

Wall Street Took Beyond Meat off Its Menu

(Source: TradingView.com)

This latest sell-off in the shares came, of course, at the hands of COVID-19.

Goldman Sachs Group Inc. delivered what I believe to be the final blow to the stock late last month, rating the stock a “sell” and lowering its price target to $39.

Over half of Beyond Meat’s sales come from the food service industry. In Goldman Sachs’ thinking, the virus represents a major threat to sales since most restaurants are either shut down or limited to takeout orders.

According to the firm, when things get back to normal, perhaps many restaurant chains — more concerned with survival than serving the latest trendy food — will be less interested in plant-based menu offerings.

Lastly, with the virus having prompted cross-border trade restrictions in Europe, Beyond Meat’s international growth prospects might be off the menu for a period of time as well.

I see things differently.

BYND’s Time Is Now

The impact of the virus and its associated economic fallout is transitory. Whether vaccines arrive on the scene or not, no one will care about any of these concerns a year or two down the road.

More importantly, at a recent $65 stock price — down 70% in eight months — those concerns are already baked into Beyond Meat’s shares.

Granted, the stock remains overvalued by traditional measures.

Analysts expect 2020 to be the company’s first year of profitable operations, generating earnings of $0.25 a share. If we divide the price by this year’s profits, we get a price-to-earnings ratio (P/E) of 260.

But then again, all things being equal, how much would you pay to own shares in a company that, despite the COVID-19 headwinds of the moment, is still set to nearly triple its profits in 2021 to $0.68 a share, and then nearly double them again to $1.20 a share the following year?

If we multiply its 2021 profits by the current P/E ratio, we’re looking at a stock price for BYND of $176 late next year.

If the company hits its 2022 earnings forecasts, even a more depressed multiple, say 100X, still means the stock doubles in two years’ time.

That’s the whole point of owning growth stocks. If a company’s earnings are rising by 50%, 100% or more in a year or two, it’s easy enough to justify a high P/E ratio.

It’s also why it’s especially important to buy shares of companies such as Beyond Meat when Wall Street analysts turn negative on them.

It means much of the risk has already been priced into the shares.

Best of Good Buys,

Editor, Total Wealth Insider