The headlines are raging: “A recession is coming!”

The spread between 2- and 10-year Treasury rates is 13 basis points.

When the spread is narrow like that, the yield curve is flat. When that spread goes from positive to negative, the yield curve is inverted.

And there’s the boogeyman. An inverted yield curve has predicted U.S. recessions for the last 60 years.

Yet at the same time, the economy is strong. And we are told the yield curve is no longer a good indicator of recession.

Maybe it’s not.

There are reasons to wonder if the yield curve’s forecasting capabilities are failing.

In July, former Federal Reserve Chairman Ben Bernanke said that normal signals like the yield curve have been distorted by regulatory and policy changes.

Last December, Fed Chair Janet Yellen suggested: “The relationship between the slope of the yield curve and the business cycle may have changed.”

And just this week, my colleague Paul made a case for why we shouldn’t fear the yield curve.

All valid perspectives.

The yield curve has not officially inverted yet. If it does, maybe the market can shake off recession fears this time.

But another indicator, with an impeccable track record, has all but triggered a countdown to the next recession.

Out With the Yield Curve, in With Unemployment

Friday’s November U.S. Nonfarm Payrolls report revealed disappointing job growth.

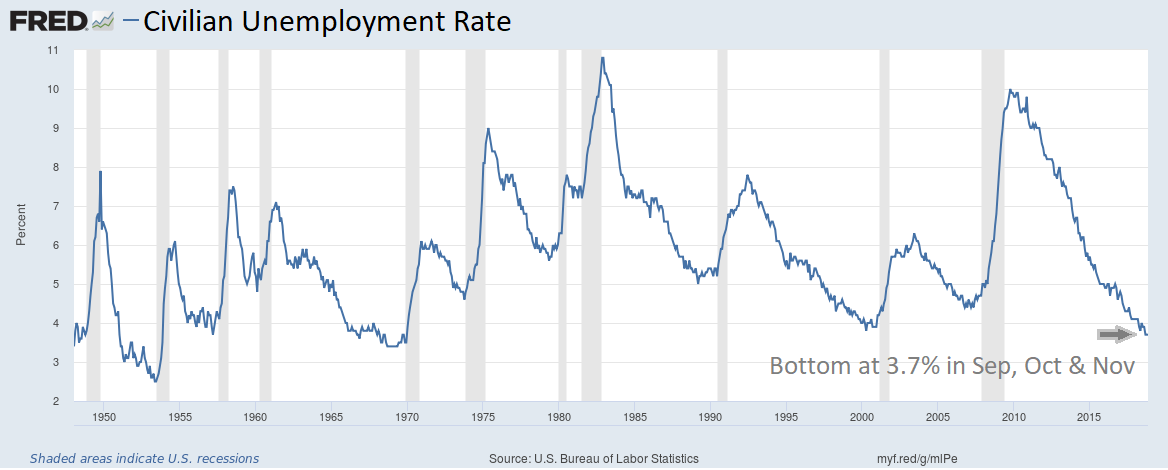

Unemployment is bottoming. And it’s a warning sign.

The blue line on the chart is the rate of unemployment in the U.S. The gray bars are periods of recession.

When unemployment bottoms, a recession follows. On average, the contraction begins about seven months later.

Today, unemployment is 3.7%. The Fed considers it “full employment.” Essentially, whoever wants a job has one.

There’s nowhere for unemployment to go but up.

It warrants caution — a recession could begin next year.

But there’s no need to panic.

Just be sure you have a plan to protect yourself from a nasty drop in the market.

Good investing,

John Ross

Senior Analyst, Banyan Hill Publishing