In times of turmoil, people tend to point fingers at anything and anyone.

And in today’s market, with two weeks of downtrends, increased interest rates and rising prices on gasoline …everyone’s pointing fingers. But who’s to blame here, if anyone?

Today I’ll be clearing the air on these gas price myths and setting the record straight on what the real issue is.

Click here to watch this week’s video or click on the image below:

Transcript

Hello everyone, it’s Ted Bauman here reporting to you from Cape Town, South Africa. Well, I’ve been away, but I’m still doing my job as always. One of the great things about being a newsletter writer is that you can pretty much do it from anywhere on the planet. So I am reporting to you from Cape Town and will be doing so until late July. Now, before we go any further, I want you to click on the little button on the screen that shows you how to subscribe, but in this case, it’s not my newsletter I want you to subscribe to. I want you to have a look at my colleague Clint Lee’s product called Flashpoint Fortunes.

Everybody knows you’re not going to make money by buying stocks in the hope that they go up right now. What Clint has done is developed an option service that has had a tremendous win rate since the beginning of the year, because he’s able to spot the possibilities of companies losing value and therefore advise on put options that you can buy to make tons of money. He’s done extremely well this year and so can you if you subscribe to Flashpoint Fortunes. So please click that little link. There’s also a link in the description below my video.

Now, today, I want to talk about oil, more specifically, gasoline prices because one of the things that really gets me is when people start talking about reasons and explanations for what’s going on that really make no sense at all from an economic perspective. In other words, they’re just not true. So let’s talk about why gas prices are high in the United States. And when we do that, let’s go back and use economics 101, shall we, folks? Here’s a picture that shows where things are:

A gallon of gas is now over $5, diesel even worse. And I can tell you, I have a diesel vehicle here in Cape Town and the same problem is here, folks. Diesel is just ridiculously expensive and I’m going to explain to you why that’s the case. Now, before we go any further, let’s just have a look at the actual track record what’s been happening with the price of gas:

This chart is a little bit dated, it goes back to 2020 and it shows that the gas price was very low. This was actually drawn from New York area, but it’s got the US average in blue. So prices did start to rise during 2021 obviously because the economy was recovering and then towards the end of 2021, prices they kind of flattened out, but then they spiked and they spiked because of the Russian invasion of Ukraine.

Now, since then they’ve continued to rise. So one of the things to remember is that although the rise in demand for gasoline and diesel as a result of the recovering economy is one factor. There’s also the Russian angle, which I will return to in a moment. But it’s not the problem that you think. The Russian issue is not what most people think. Now, of course, politicians are having a field day, aren’t they? I mean, that’s what they do. Republicans blame President Biden and the Democrats for being anti-energy says The Wall Street Journal.

Basically green policies threaten the oil industry so the oil industry won’t invest and so that’s why we have high gas prices. Democrats blame the oil industry for exploiting the situation to reap windfall profits, fattening their margins, pocketing lots of money at everybody else’s expense. Some like me actually blame bigger pictures, longer-term trends and in particular, the role that the financial sector plays in determining whether or not investments happen in a big, expensive industry like oil.

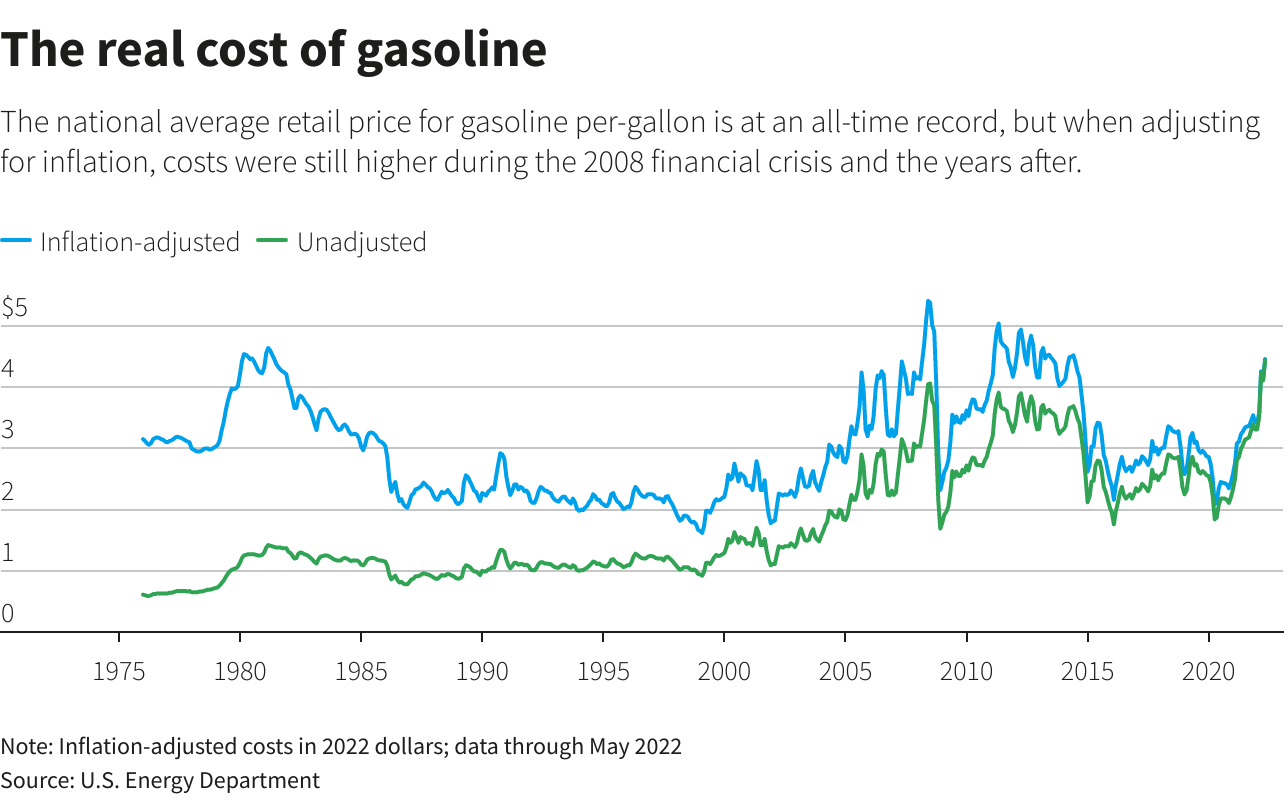

Remember, Wall Street controls the money that finances things like oil refineries and drilling. And if they don’t want to play ball, it’s not going to happen. Now, let’s talk about a couple of facts that most people are unaware of. When I researched this I kept surprising myself. I kept going, “Wow, is this true?” Well, let’s start with one. The real cost of gasoline is actually lower than it was during the Great Financial Crisis. Here’s a chart that shows the inflation-adjusted and unadjusted price of gas. The inflation-adjusted price is in blue:

Now, it’s a little hard to see maybe, but it’s substantially lower than the unadjusted retail average price. In fact, it’s right about where it was during the period from around 2005 until the financial crisis, and then again after that when there were still shortages in oil production resulting from the effects of that crisis. So, the key thing here is that everybody is freaking out about the price being over $5 a gallon. The reality is that it’s actually less expensive in inflation-adjusted terms. In other words, considering what people are bringing home in terms of wages and so on than it was not too long ago. I know that doesn’t make anybody feel any better, but it is an important factor to remember. It’s been worse in the past.

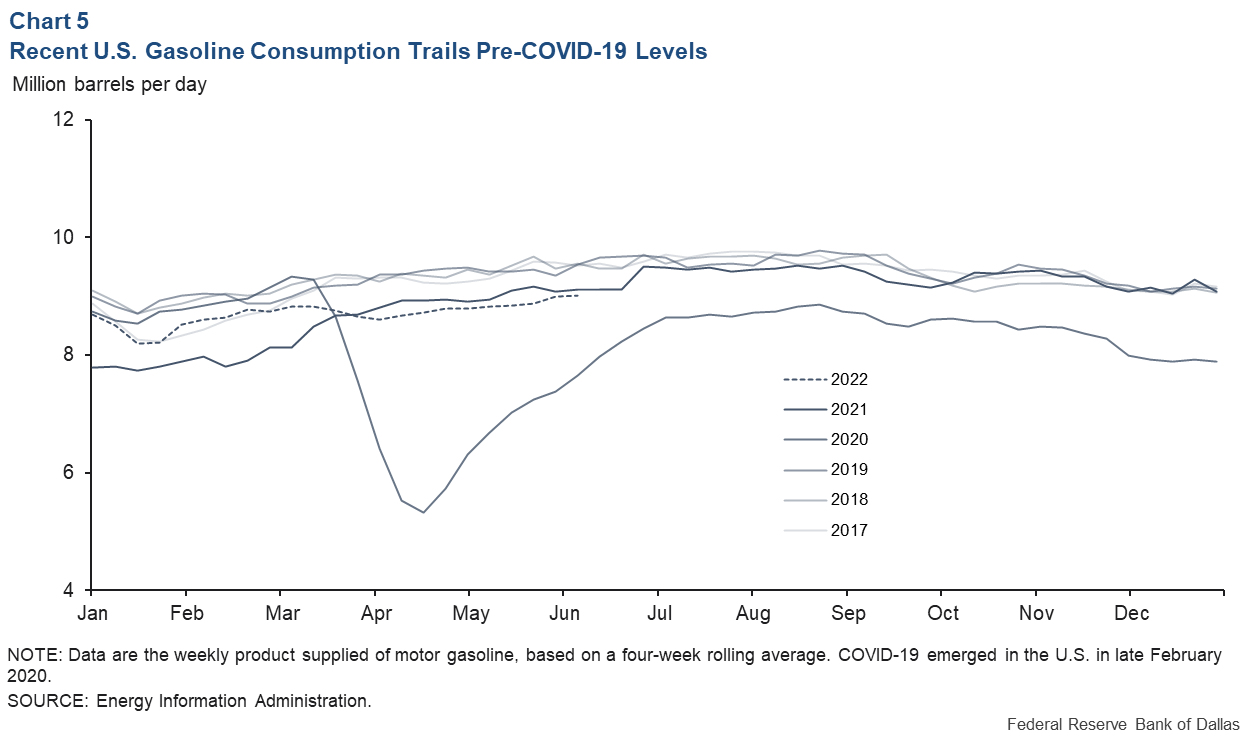

The second factor that I think is so amazing because nobody seems to be caught on to this is that consumption is actually not higher than usual. A common argument is that the Biden administration’s COVID relief spending has led to too much money chasing too few goods and that gasoline is one of those goods, but the facts don’t bear that out, folks. Here is a chart that shows recent U.S. gasoline consumption on a yearly basis. And the dotted line is 2022:

Now, what’s interesting to me is that dotted line is below every single line except for 2020 and that is the year of COVID. Right now, consumption, in other words, the millions of barrels of gasoline or equivalent barrels of gasoline consumed every day are lower than they were in 2021, 2019, 2018, 2017. So how can it be that we have high gas prices because if demand is lower than it has been historically, then it doesn’t make sense that there should be high gas prices? Yes, we know that the price of oil has gone up, but the United States also has domestic production capacity most of which is not exported, which typically gets sold to refiners at below the global market price. So we shouldn’t see prices as high as they are, unless there’s something else at play.

Now, the third factor that a lot of people are not aware of is that sanctions on Russian oil matter, but not in the way that you think. Now, before its invasion of Ukraine, Russia was a major exporter of both crude oil and refined petroleum products, especially diesel. Now, one of the things that a lot of countries like Russia do is they provide what’s called feedstock, which is an intermediary step between oil and the final product gas or diesel or even kerosene.

And the idea is that they do the first step of refining in Russia and then put it on ships, and send it elsewhere where it gets refined into whatever people want. Now, one of the critical things about Russian oil production is that their Urals light crude is particularly suited for the production of clean diesel. Now, again, being in here in South Africa it’s reminded me that 10 years ago, diesel was a much more polluting than it is now because the amount of polluting particulate matter in diesel has been reduced by switching over to cleaner feedstocks, and a lot of those feedstocks came from Russia.

Now the problem is that whereas Russian oil goes through pipelines, which have not been shut down, oil is still flowing on land-based pipelines. Russian ships are no longer accepted in ports pretty much all around the world, except for China and a few other countries. So the result is that even though Russian oil is still getting onto the market, Russian-refined oil products, including the precursor to gasoline and diesel are not.

So there is a shortfall in that segment, which helps to explain the high price of diesel, but it’s not so much a problem for gasoline. And that leaves the actual factor, the one that very few people have been talking about at least in the mainstream press and that is refining capacity. Now, the last new oil refinery or refinery was built in the United States in 1997. Since then, we’ve seen steady increases in fuel efficiency and so the oil industry, the midstream sector, i.e., the refiners tends to believe that they can manage with the existing refinery that they have.

So they haven’t been building new refineries, they’ve been adding onto existing ones. They’ve been basically kind of managing it in a way that they can cope with current demand without having to go to all the expense of building new refineries. But COVID had a massive impact on this like so many other things. Since the COVID crisis started, six US oil refineries have closed, including one that was damaged by Hurricane Ida in the Gulf last year. Two others have converted to produce renewable diesel. In other words, diesel that is made from renewable feedstocks like oils and things like that, cooking oils.

So the bottom line here is that the big problem that we have is that when COVID hit like a lot of other industries, the U.S. oil refining industry cut back on capacity thinking, well … as one industry observer put it, they said to themselves, “Alright, well, we’re planning to retire these facilities, these refineries anyway in a year or two so let’s just do it now. There’s no reason to try to hold onto them and keep them going if the economy’s going to slow down, and they’re so close to the end of their operational lives.”

And of course, that’s not what happened. We recovered from COVID and all those decisions now seem silly, but they made perfect business sense at the time. Now, the result is that us refining capacity has fallen by nearly 5.5% since 2019. That’s more than a million barrels per day in refining capacity. Here’s a chart that shows that, it shows exactly what’s happened:

Look at 2019, it maxed out at just under 19 million barrels a day in refining capacity, but now it is under 18 million. So we’ve seen a huge drop in refining capacity. Now, the interesting thing though is that that capacity is still not being fully used. And here is a chart that shows utilization of U.S. refining capacity:

Now you’ll note that on the far right-hand side this is a bit dated, it goes back to January only, but it’s still lower than it was back in 2017, 2018. And the reason for that is that some of this capacity is offline temporarily. Now, one of the things that happens when there’s a slowdown in the economy like during COVID is that instead of spending a lot of money to repair and build new machinery at refineries, you simply go and borrow from parts of the refinery that are not being used and use them, you cannibalize them and you use them to basically keep the other parts of your refinery going.

So what’s happening now is it’s taking time to get potentially available refinery capacity back up and running because some of the parts that were required to do that were basically taken to fix other parts of the same refineries. So the key thing here is that we’ve got lower refinery capacity and we’re not using all that capacity because some of it needs to be brought back online. Now, what that means is that the single-biggest driver of high oil prices or gas prices isn’t just the cost of a barrel of oil. It’s the margins that refiners are getting.

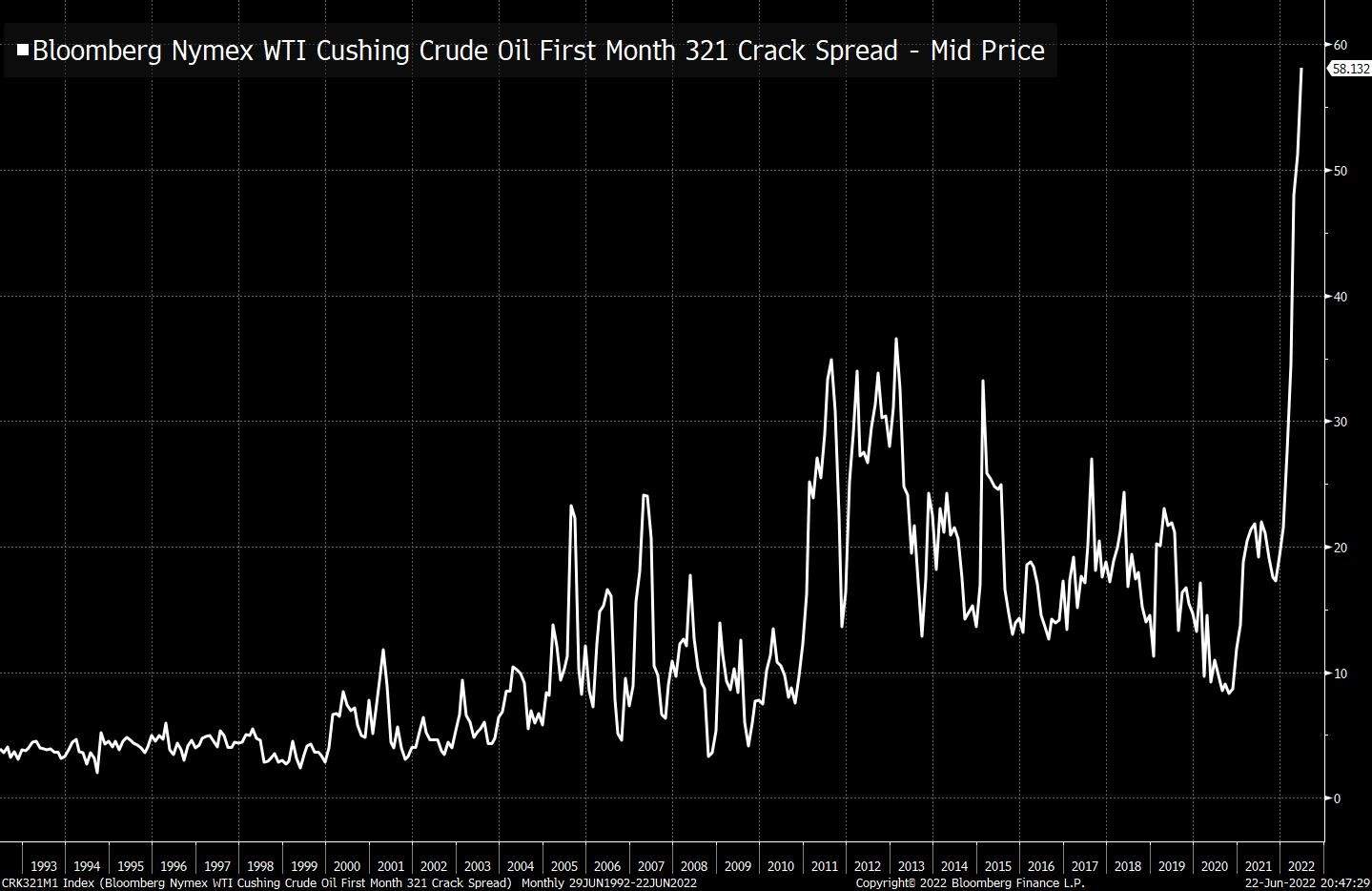

Now, the margins that refiners get are basically the difference between the price of a barrel of crude oil, landed at the refinery and the price of a gallon or the price of a barrel equivalent of gasoline or diesel as it leaves the refinery to go onto the retail market. Now, here’s a chart that shows what’s known as the crack spread going back to the early ’90s:

During most of the ’90s it was fairly stable. It peaked several times during the mid-2000s thanks to oil issues related to the Middle East. It rose again after the Great Financial Crisis for similar reasons to what we’re seeing today, that refining capacity was mothballed during the great financial crisis. You can see it having pulled back from its peak in 2007, during 2008, ’09 and ’10. And then because that capacity had been mothballed temporarily, crack spreads rose, but then they kind of fell over time. But look what’s happened now, look at the spread. I mean, we’re seeing a current crack spread. This is basically the number of dollars per barrel of oil that goes into the refiner’s profits. It’s now sitting at $58.13 a barrel.

Now, the normal crack spread, the one that most people that during normal times, it’s between 10 and $20. But thanks to the loss of refining capacity in our refineries, that’s now averaging 50 to $70 a barrel, that’s on top of $120 a barrel oil. So that’s three and a half times the normal rate. Oil has doubled in price basically since the debts of the COVID crisis, although at one point oil was trading for negative. It was people were paying you to take their oil, but around $60 a barrel was kind of the benchmark, now it’s 120, that’s twice. But what we’re seeing is three and a half times that in crack margins, which are the refiners’ margins.

Now there’s a final issue, which you never see discussed anywhere except in the trade news which is the real story. And that is that Wall Street does not want to see U.S. oil producers invest in new production. Now, there’s a common belief that is the major issue and that the reason is because of the Democrats and President Biden, and green oil policies and all of that. Well, that’s fine if your mission is to produce propaganda and stir people’s anger, but it’s certainly not the only issue. In fact, I’m going to show you a chart just now that shows you that it’s a relatively minor issue:

The problem is that global oil projections are down. In other words, the future (after we get through this current patch) oil consumption is still going to decline over time thanks to increasing efficiency in the use of gasoline and diesel engines becoming more efficient vehicles. But also because of the rise of green energy, things like electric vehicles and hydrogen. And that’s a market-driven phenomenon. That’s not President Biden telling people not to use oil. The market is already doing that itself. A lot of us have made good profits by investing in alternative energy, in alternative vehicles. And we do that because we know that that’s the way the market is headed. Well, so does Wall Street, but what Wall Street fears most of all is the repeat of what happened about eight years ago. About eight years ago, 2014, 2015, the U.S. had just gone through a major boom in shale fracking.

In Texas and in North Dakota, we saw huge output coming from this new fracking technology and it was doing wonders. It was helping to drive the price of gasoline in the U.S. down, but then the oil price collapsed for a couple of reasons. One was a slowing global economy after the initial recovery from the global financial crisis. But the other was simply that basically because so many people were rushing into fracking, producing so much new crude from that source, eventually the market got oversupplied and there was an oil glut globally.

Now, that led to bankruptcies all across Texas, all across the upper plains basically in North Dakota and so on as producers, frackers and even pipeline companies that had borrowed a lot of money to increase capacity went bankrupt. Loans didn’t get paid to Wall Street. Investors who had put equity investments into these companies lost their shirts. So right now Wall Street is saying, “Hey, folks, we’ve been here before. We’ve seen high interim prices and we know what comes afterward. Eventually, they normalize. If we spend a lot of money now on increasing capacity, all we’re going to do is position ourselves for another glut and another collapse in prices, which will cost us more money.”

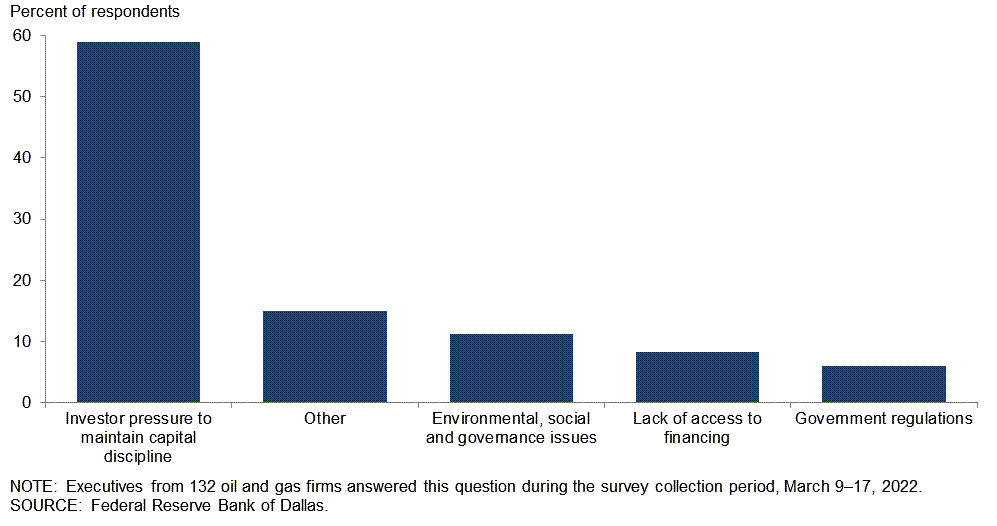

So for now what’s been happening is that Wall Street financiers, big banks, hedge funds, the ones who traditionally provide the financing to expand production capacity are saying, “Hey, what we’d rather see you guys do with your windfall profits is buyback shares and issue dividends.” In other words, give money back to the market. Don’t spend the profits you’re making in boosting production capacity, because you’ll be sorry in the long run. And here’s a chart that shows precisely that:

This was a Federal Reserve of Dallas questionnaire they sent out to 132 oil and gas firms. And nearly 60% of them said that investor pressure to maintain capital discipline, i.e., not invest in new production capacity was the single biggest factor preventing them from investing in new output. Even other was bigger than environmental, social and governance issues and government regulations.

So the key thing here, folks, believe what you want to believe. I know a lot of people are going to watch this video, you’re going to write in the comments that I’m talking rubbish. But the reality is that there are a host of factors other than politicians that are causing the gas price to go high. And one of the main ones is the internal dynamics and decision-making of the oil industry and of the financial sector that finances it.

Now, what can we do? Well, even if U.S. oil producers increase their output, we don’t have enough refining capacity to handle it. So you’ll get maybe more oil and a lower oil price, but you won’t get more refining capacity because the refineries are already near peak capacity. So instead what we’ve seen is gas prices rising because of a classic mismatch between demand and supply. Remember, these things take a long time to resolve.

Now, you could artificially cut gas prices like Biden and Congress are considering doing by suspending the gas tax, but that won’t help because prices won’t go a little bit lower, but then we’ll end up with shortages because people will want to buy more gas at that lower price. But we still won’t be able to produce more of that gas because our refineries are at full capacity. At the same time, providing subsidies to drivers like California’s proposed $400 per vehicle gas tax rebate would simply increase the profits going to refiners.

People would go out, they’d buy more gas, but all it would do is feed the pockets of the refineries, feed their profits because it wouldn’t necessarily lower the gas price. So do you want government action that produces long queues at petrol stations or do you want government action that pads the pockets of the refiners? I don’t think anybody wants that. What they want are lower gas prices. Now, ultimately the only way that’s going to happen is if the demand for gas begins to fall and in a twist of fate it looks like that might be happening soon.

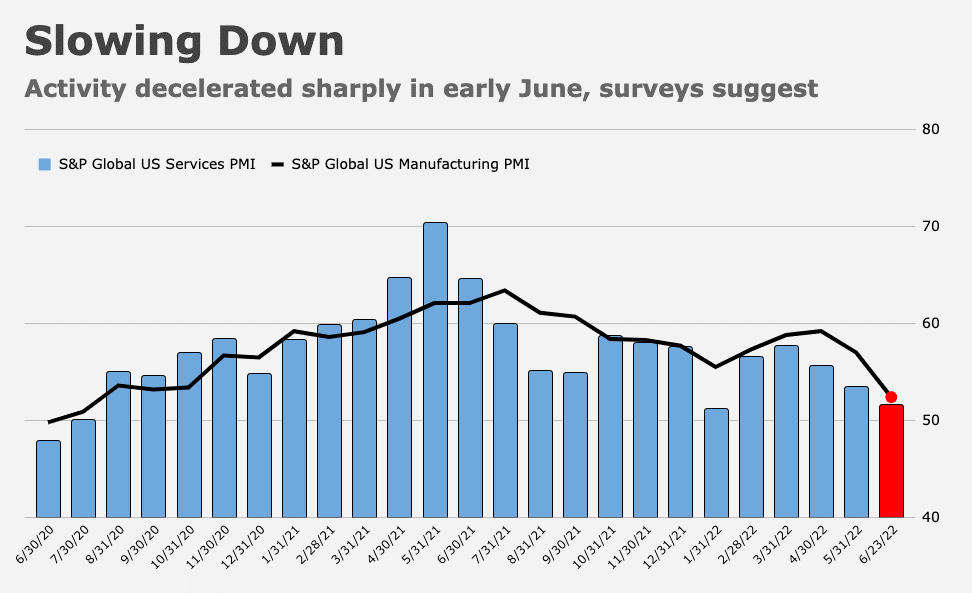

Here’s a chart that shows global U.S. services and manufacturing producer price indices. And what we’ve seen since the beginning of the year is that those things are falling dramatically. Basically, we are starting to see the effects of the rise of interest rates and basically the fact that people have spent a lot of the stimulus money. The economy is slowing down, folks.

So my prediction is that we’re going to see high prices throughout the summer. We’re going to continue to see them be higher than they normally are, but within six months, maybe a little bit longer, we’re going to see gas prices going back down to levels that are compatible with U.S. refining capacity. Now, obviously, the Russian invasion of Ukraine and the impact on the oil market is going to have a big impact until it’s resolved, but I still believe that we could get back to lower oil prices.

What’s not going to happen I believe is that U.S. oil prices are not going to end up producing more or investing in more production capacity, because they don’t want to get caught with their financial pants down the way they were in 2014 and 2015. And that’s just a fact of financial life in business. Unfortunately, it’s costing you and me and trust me, prices are up in this country as well as the United States.

So for the time being, we just have to grin and bear it. And if it makes you feel better to point fingers at politicians, be my guest. Unfortunately, it’s not going to solve your gas price problem. Anyway, this is Ted Bauman signing off and don’t forget to check out Flashpoint Fortunes. I’ll talk to you again next week.

Kind regards,

Ted Bauman

Editor, The Bauman Letter