He made $100 million for himself and $700 million for his investors in 2008.

And now he’s at it again.

Michael Burry predicted the 2008 global financial crisis, bet against the housing market and made a fortune.

There was even a movie made about him.

So when Burry tweets, people pay attention.

In a post on X (formerly Twitter), on September 29, 2022, Michael Burry predicted another crash.

This time he’s betting that the stock market will crash…once again.

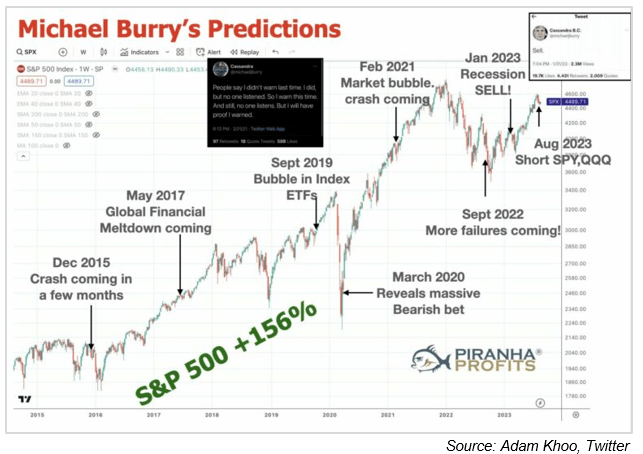

Anytime I see a prediction, I check out how previous predictions panned out.

And Burry’s record of making big predictions leaves a lot to be desired:

- 2005, he predicted the collapse of the subprime mortgage market. We all know what happened in 2008…

![]()

- 2015 predicted another crash — the S&P 500 surged 11%…

![]()

- 2017 predicted a global financial meltdown — S&P climbed 19%…

![]()

- 2019 predicted a stock market crash due to a bubble in index ETFs — the market gained 15% the following year…

![]()

- 2020 made another bearish bet — the S&P rocketed 72% and he had to issue an apology on social media…

![]()

- 2022 — the market shattered another of his market crash predictions with a 21% surge…

![]()

Burry’s track record begs the question …why would anyone listen to his predictions?

(Click here to view larger image.)

Yogi Berra was spot on when he said: “It’s tough to make predictions — especially about the future.”

The bottom line, folks, is this … no one has a crystal ball.

It is impossible to predict the future and be right all the time.

I have a better way … that’s worked for me as well as some of the greatest investors of all time.

Without making predictions, I’ve helped my readers make open gains of 215% in four years, 356% and another 186% in three years.

Here’s how…

Think Differently

I’m an Alpha Investor.

That means I don’t need or use crystal balls, astrology, sunspots or read tea leaves to make money in the stock market.

Alpha Investors stand head and shoulders above the rest because…

We don’t invest because others agree or disagree with us.

We invest because our facts and analysis are right.

We are confident in our decisions and don’t need confirmation.

We don’t stay in the middle of the pack … we lead.

We are not afraid of stepping out.

We think differently than other investors.

THAT’s how we make money.

With that mindset, I help Main Street Americans invest in Alpha companies … stocks that will return a minimum of 100% within four years.

To find those companies, I make sure it meets my “Alpha-4 Approach”:

- Alpha Market: Investing in a company riding a mega trend.

- Alpha Leadership: Run by a CEO with integrity, experience and a proven track record.

- Alpha Money: In a company that has a rock-solid balance sheet.

- Alpha Price: When the stock price is trading below the underlying worth of the business — that’s a great price.

If you’re fed up with mediocre returns, story over substance or just want to start making money — I invite you to be an Alpha Investor.

Because Alpha Investors are a breed apart.

Regards,

Founder, Alpha Investor

Attention Alphas: Charles spotted his 4 Alpha Pillars flashing in one sector. A bull market is just getting started in this Alpha Market. So, if you want his favorite stock recommendation (trading for less than $15 right!) — click here for the details now.

The Credit Card Catastrophe

We’re already starting to see the first signs of stress.

Two weeks ago, I commented that credit card debt had topped $1 trillion for the first time… and that balances had exploded higher by 35% in just two years.

Now, a trillion dollars is a lot of money.

But in a vacuum, that number doesn’t necessarily mean much. It’s not the balance that disturbed me. It was the speed with which we got there that raised the red flags for me.

And about that…

A recent report by JD Power found that only 49% of Americans with a credit card are able to pay off the balance each month.

51% of Americans with a card now carry a balance … and at an average rate of 14.8%.

Now, it’s not the 51% by itself that is the problem. If that was a static number, I might shake my head in disapproval, but I wouldn’t necessarily consider it cause for alarm.

But that number isn’t static…

And it’s trending higher.

In fact, this is the first time in the history of the survey that a full majority of American credit card holders were unable to pay their balances in full each month.

Of course, you know how credit card balances work.

Once you get into a hole … it’s really hard to dig yourself out.

Particularly when you’re paying pawnshop interest rates. The debt snowballs and, for many, ends up becoming unpayable.

And of course, all of this is happening before student loan payments restart next month. Adding several hundred dollars of debt payment into the mix will no doubt push the number of at-risk credit card holders a lot higher.

Trouble Ahead?

Are the banks in trouble? Not really…

Yes, they will take losses, and their shareholders won’t be happy, but this won’t be enough to really blow them up. This isn’t as dangerous as the mortgage crisis that took down the banking sector in 2008.

My concern is what it means for consumer spending.

At some point, credit card debt becomes unpayable for a large swath of borrowers, and the defaults start … which forces the banks to tighten lending standards and cut some borrowers off.

Every dollar not borrowed is a dollar not spent. And every dollar used to pay down debt is effectively two dollars not spent.

We shouldn’t underestimate the economy’s ability to muddle through far longer than we imagine possible.

If we’re looking for that proverbial straw to break the camel’s back … this might be it.

Have you ever had to pay off credit card debt before? Let me know your thoughts here.

Regards,

Charles Sizemore

Chief Editor, The Banyan Edge