The Federal Reserve’s interest rate rampage continues as the S&P 500 and broader market officially enter bear market territory.

But this isn’t the end of the world. Quite the opposite.

In fact, today I’ll be giving you four key signals that will eventually confirm the Fed’s fury is ending. Follow them to find out when the market really hits bottom … and you’ve got a golden ticket to future gains.

Click here to watch this week’s video or click on the image below:

TRANSCRIPT

Hello everyone, it’s Ted Bauman here with Big Picture, Big Profits, with your Friday video. I’m editor of The Bauman Letter. If you’d like to subscribe to that letter, you can click on the little icon up in the left-hand corner, or you can click on the link below in the description. We’re doing great guns with our dividend payers this year. We are beating the market by a hefty percentage, and that’s really been the strategy. We’re focusing on companies that make good money, have good strong moats, paid good dividends, so that even if the market falls, you’re still getting that great return.

Three things happened in the market today. Even though I’m here, in South Africa, you can see I’m wearing my cold weather clothing, because it’s really cold here in Cape Town. Three things happened this week. First, we officially entered a bear market in the S&P 500, which means despite the fact that the Nasdaq hit bear quite a bit earlier this year, now the broader market is officially in bear territory. Really, the question is what happens after that? I’m going to be talking about that just now.

The second thing that happened is that the Fed raised its benchmark interest rates by 75 basis points or 0.75%. That was widely anticipated by the market, particularly after the inflation print last Friday. That’s why the market was so bad on Monday. That’s what pushed this bear because, essentially, when they saw that the inflation print had actually come in higher than expected and higher than the previous month, in fact highest to 40 years, I said, “That’s it, the Fed is going to raise rapidly, so we better brace ourselves.” It’s weird, but there were people actually talking about the possibility of a dovish tilt, of a slowdown, of a pause in interest rate hikes. I think the problem is that too many people have spent their entire careers in the soft, easy money regime, and they don’t understand how this kind of stuff works. I’ll get back to that in a moment.

The third thing that happened, this week, is that the world did not end. I think, a lot of times, people forget that all this stuff passes. Everything that’s happened historically in the stock market eventually resolves. Sometimes it takes a while. The bottom line is, this is just part of the game. You don’t always get stocks going up. You don’t always have a friendly macro environment to trade in. Despite what a lot of people were saying in 2020, 2021, that’s not the way the market works folks. Bad things happen too, but eventually they end.

That’s really the question we want to look at today. On that score, I noticed that the Bank of America surveyed investment managers, the big guys, the ones who handle a lot of money. They had a questionnaire they sent out to firms that have a combined, almost, trillion dollars’ worth of money under management. Those are some pretty heavy hitters. One of the things that they asked them were, “What do you think needs to happen, in order for the Fed to stop raising rates?” So, today, what I thought I would do, is talk about that. Let’s talk about what’s actually happening in the market. That’s one thing, but what about what would happen going forward? What would it take for the Fed to say, “Wait we’ve raised rates far enough”? That’s really a question that everybody wants to know the answer to, because that’s really the key thing.

Here are four things that the market talked about, or rather that the Bank of America people identified, the survey respondents. The first one is that if you get a monthly inflation print below 4%, that could lead the Fed to pause and say, “Well, if we’re heading in the right direction.” Now, one of the reasons why that would be so significant is because it’s so far below where we are. Here’s a chart that shows private consumption prices, the core measure of inflation that the Fed likes to use:

You can see that they are very, very high. What you’d need to see is for that green line to fall below four. That would, potentially, lead to a pause in inflation rates, but that seems like the least likely one.

We could see inflation over 4% for the next, for the rest of this year, easily, possibly into next year as well, given the way things are going. Remember, this is not just about COVID. This is not just about supply chain problems, or COVID relief payments and all the cash that that pumped into the economy. It’s also about the war in Russia or in Ukraine, which has thrown the energy markets into a big tizzy. Of course, the same thing applies to agricultural commodities. That’s the first thing. If we see inflation below four, that would imply that a lot of those inflationary drivers have been resolved. That could lead the Fed to dial back its rate increases.

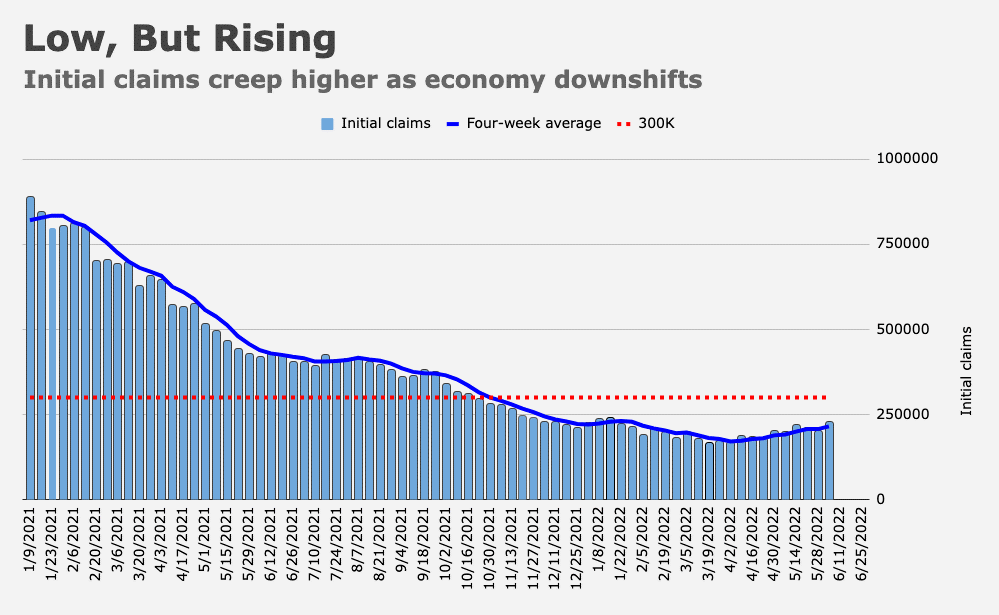

The second thing would be if we see a monthly new jobless claims rise over 300,000. That’s the second thing that the investment managers thought would be the case. Here’s a chart that shows where things have been:

We bottomed out, back in March, with the lowest claims’ levels so far, but then they started to rise again. Part of the reason why they’re rising again is because of the knock on effects of the ongoing problems in the global economy, but also simply because people are not spending money on certain things. They’re shifting. They’re spending away from things that they were spending a lot on, during the pandemic, like durable goods, and they’re shifting more towards services.

Now, you would think that would mean a big rise in the rate of employment, or rather in employment in service sectors, but that’s not necessarily happening yet. We’re seeing a lot of service companies, particularly fast food restaurants, even retail stores, shifting towards automation, and trying to decrease their dependence on physical labor, actual human beings. Bottom line is the investment boffins think that if we get above that dotted red line, we could end up seeing the Fed hitting pause on interest rate hikes.

The third thing would be if the credit market starts to show cracks. Now, remember credit markets are like an octopus. They have a lot of different pieces, a lot of different arms. There are different types of credit. Obviously, the Treasury market is a type of credit, but what we are really concerned about is the spread between yields on junk bonds and on treasury bonds. What happens is, that as financial conditions tighten, when companies roll over their debt, whether it’s monthly, quarterly, yearly, whatever, their short-term debt financing, they often face higher interest rates.

Once the spread gets really high, once people start becoming cautious about buying a junk corporate debt, that leads to a general reluctance to invest in that, which means that rates get even higher. You can get a nasty spiral going. The Fed would be pretty nervous about letting that get out of hand, because it could imply bankruptcies, which means counterparty risk, which means you could have a new financial crisis, on top of the inflation, everything else. If anything, I would imagine that’s probably the one that the Fed would be the most concerned about. That would be the one that would lead them to act very quickly, if we started to see serious problems in the junk bond market.

Now, here’s a chart that shows the spread between high yield corporate credit and the 10-year Treasury, which is kind of the global benchmark:

It’s risen above the 5% spread level. That’s basis points on the right-hand side. 500 basis points is a 5% yield spread. We got there in the beginning of 2019. Remember, that was the period when, just after 2018, the Chairman Powell talked about tightening and slowing down the Fed’s QE activities in the market through a tantrum. That’s what led to the yield spreads then, but he backed off ’19. 2019 was pretty good, not too many problems, although we did have higher spreads than we did in 2018. Then, came COVID that we had a short term spike, and yield spreads fell below the long term average until the beginning of 2022. They’ve risen. They spiked early in the year, fell again, spiked again. They’re down a bit, they’re down towards the 4% spread, but they’re inching back up.

Now, remember, this is probably the single most important thing to watch, because all of these things are things you can easily pay attention to. You can get on any of the news sites, whether it’s monthly jobless claims or the inflation print or yield spreads. The key thing is that these are the things that the Fed is going to be paying attention to. If you can anticipate their direction, you can start placing bets on a pause in the Fed’s rate hiking, which would then lead to a bounce back in stock. If you can see it coming, you can start positioning yourself and hit go. Fire your stock purchasing cannon when you begin to get the accumulating evidence that the Fed is going to pause, because then the stocks are going to start taking off again.

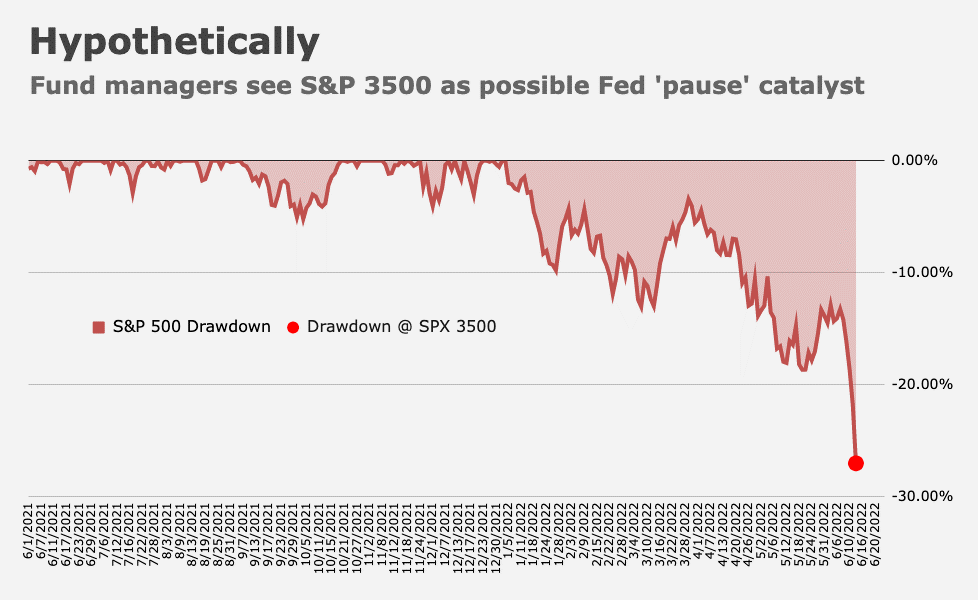

The fourth thing, of course, is if the stock market goes down to a level that the Fed begins to feel uncomfortable with. Remember, we often say the stock market and the economy are two different things, which is true. The stock market is the backstop for a lot of wealth in the economy. When the stock market falls to certain levels, that means that you begin to have a reverse wealth effect, where people stop spending money because they feel like they’ve lost a lot of wealth because stock prices in their portfolios have fallen. The stock market does have a practical effect. Now, less than 50% of Americans own stocks. Only a tiny sliver of people own enough stocks where it really becomes a major issue for them, if prices fall off a cliff. In that 90% to 99% income percentile, you do have people who will make major shifts in their household spending, particularly on things like new vehicles, durable goods, renovations, even vacations, and things, if the stock market keeps falling. The thing is, we know where the Feds put isn’t, it’s not at 4,000, it’s not at 3,900, it’s not at 3,800. We’ve passed all of that. The question is, where is it?

Well, the guys that Bank of America interviewed said they think it’s around 3,500. If the treasury market or rather the S&P 500 were to fall down to the 3,500 level, that could lead the Fed to say, “We need to re-institute our put.” Now, that would be still quite a bit below where we are. That would be in the neighborhood of about 32%, 33% fall off from the peak that we experienced on January 3rd, but it would still be a pretty significant fall from even where we are. The critical point, here, is that even if we do- Excuse me. Even if we do get the Fed intervening, it would probably still be in conjunction with some of those other factors.

Now, remember, all of these things are interrelated. The level of the stock market depends strongly on things like unemployment claims, inflation, et cetera. The paradox is that the better things get, the lower inflation. The lower unemployment claims get, the stronger the economy. The more likely that we’ll see further inflation. That leads the stock market to go down. It’s a weird paradox. Strong economy means higher interest rates, means lower stocks. Weaker economy means lower interest rates, means stronger stocks. Go figure. Anyway, where we are this year, I’m just calling up. We are down 20.48%, as of the close yesterday, on Wednesday. That would still be another eight points beyond here, if the Fed were to intervene on that basis.

Now, the other thing to bear in mind is what happens after you hit bear. In many cases, the stock market bounces back quite strongly, after we hit bottom. The critical thing, of course, is to know when we do hit bottom. I tend to think that because there are no obvious financial stresses right now in the system, although the corporate credit market could do it, we don’t have major problems in the economy. There’s nothing that, other than interest rates and inflation, could derail the economy. My sense is that the Fed will probably take their foot off the gas, before the market gets too far down. Not because of the market, but because the underlying economy is relatively robust.

The critical thing here is, you got to keep your powder dry. You got to keep your eye on The Financial Press. Listen to people, like me, who are watching these things. Look for the unemployment prints. Look for the inflation prints. Look for junk, sorry, junk bond spreads over treasuries. That’ll give you an idea of when the Fed might say, “We’re not going to raise this time.” Trust me, if the market begins to feel, if they begin to price in that the Fed is not going to be raising interest rates for a couple of their meetings, the market will recover and strongly. Of course, if that holds, if they can maintain that, I think the market could recover. You could see 20%, 30% gains, over the next 12 months, if you can spot the bottom. That’s going to be the big question for everybody.

In the meantime, keep your money in the strong cash flow generators, companies that have good balance sheets, companies that survive well during depression. I like the low income retail sector, obviously. We’re starting to see stocks like Dollar General and so on bounce back way over the big guys like Target and Walmart. Start thinking about recession but also keep that powder dry, because if you can have money on hand, when the stock market turns, if you can buy the bottom, you can make a lot of money.

Anyway, this is Ted Bauman signing off. I will talk to you again next week. Bye, bye.

Kind regards,

Ted Bauman

Editor, The Bauman Letter