There’s a big problem: Millennials aren’t investing.

Only a third of millennials ages 26 to 37 have a retirement account.

When we examine the numbers, they look dire.

According to the National Institute on Retirement Security:

Only 19.1% of millennial Latinos and 22.5% of Latinas participate in an employer-sponsored plan, compared to 41.4% of Asian men and 40.3% of millennial white women, who had the highest rate of participation in a retirement plan.

On the high end, if you’re a millennial Asian man, 58.6% of your peers aren’t going to be prepared for retirement.

And on the low end, if you’re a millennial Latino, 80.9% of your peers are unprepared.

Do you fall in this age range? Your children? Your grandchildren?

We can solve the millennial retirement crisis. It’s not too late to convince young people to start saving for retirement now.

Millennials Are Missing out on Free Money

If you know a millennial whose eyes glaze over at the mention of retirement planning, they might need a reminder that their company is offering free money.

More than half of U.S. employers offer a 401(k) “match.”

This means that, for every dollar an employee contributes to his or her 401(k), the company will contribute $.50 up to a percentage of the employee’s salary. The median is 6%.

That’s essentially a 3% raise deposited right in the employee’s retirement account!

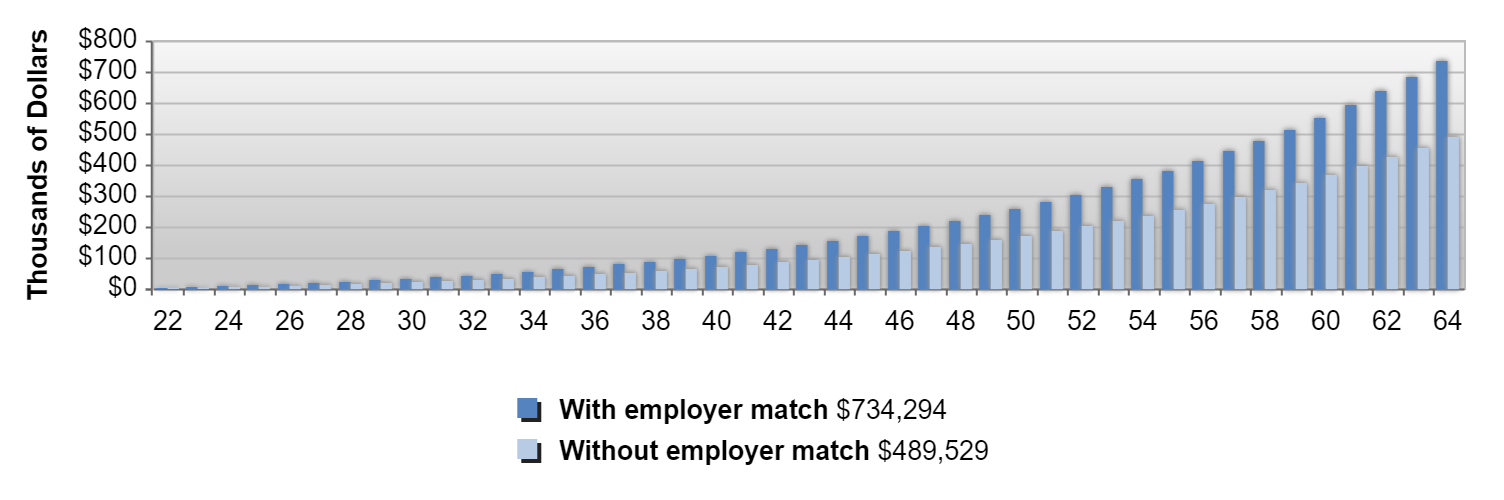

That might not sound like much, but take a look at this 401(k) calculator chart from Bankrate. It contrasts salary with and without an employee match. The dark-blue lines show the amount in a 401(k) with an employee match each year to age 64.

3% 401(k) Match Makes a Huge Difference Over Time

For one, the millennial, age 22, makes the average income for their age range as of last year, according to a study by CNBC — $27,300.

It presumes they contribute 6% to their employer’s 401(k) with an annual salary increase of 3%, a retirement age of 65 and an employer match of 50% on up to 6% of their salary (so, a 3% match).

A small 3% match makes a massive difference over time. After just 10 years, they’ll have $14,486 more thanks to the company’s money.

And by age 64, thanks to interest and returns, the employee with a match will have an additional $244,765 in their account without having saved an extra dime.

If they start at a higher salary or their annual increases are greater thanks to promotions, it gets even better.

Many millennials are a long way from retirement, so they aren’t thinking about it. Their salaries, however, are another story.

A reminder to take advantage of their company’s match — and make 3% more that easily — can be powerful.

A chart, like the one from Bankrate, that shows how much money they’re passing up if they’re not participating might be the best way to show how important, and how easy, it is to save money. We can solve the millennial retirement crisis by showing them the money!

Good investing,

Kristen Barrett

Managing Editor, Banyan Hill Publishing