In recent articles, I’ve talked about how raising interest rates leads to lower inflation.

Inflation is caused by a mismatch between supply and demand. The Federal Reserve can’t increase the supply of goods and services. So, to control prices it must engineer “demand destruction.”

That’s as nasty as it sounds.

I’ve already explained how the Fed uses the “wealth effect” to make households with lots of stocks cut spending … and why that strategy won’t work with U.S. wealth concentrated in so few hands.

I also explored how big changes in the U.S. and global economy since the 1970s will force the Fed to raise interest rates A LOT to bring inflation down.

Today, we’re going to look at the impact of their demand destruction on U.S. households.

The implications aren’t pretty. Depending on how long it takes to bring inflation under control, what you’re about to hear could completely upend the investment landscape for years to come.

Fortunately, forewarned is forearmed — and I’ve got my eye on companies that will thrive in these conditions.

Home Is Where Prosperity Is

Mainstream talk assumes that wages are the main driver of inflation, as in the 1970s.

True, the labor market is tight. Higher interest rates will lead to a weaker labor market, as businesses cut investments and hiring. Wages will fall, especially for lower-income households.

But the big impact of demand destruction won’t fall on burger flippers and cashiers.

It’ll hit the middle class, especially those in their prime working years, via housing costs.

Housing is the biggest driver of wealth accumulation for most U.S. households. Building equity in a home is a major part of the American dream. It’s not necessarily the road to riches, but it’s historically been a path to comfortable prosperity.

To see how rising interest rates will affect that, consider the things that constitute “prosperity” for most people:

- Healthy food.

- Comfortable and dependable shelter.

- Essential services, like water, electricity, heating and cooling, and digital connectivity.

- Adequate health care.

- Education and personal development, especially for kids.

- Modern conveniences like labor-saving appliances, electronics and entertainment goods.

- Recreation, ranging from dining out to vacations.

- Having enough left over at the end of the month to invest in your family’s future.

The Hill Just Got Higher

Households extend and improve their enjoyment of the eight elements of prosperity over time. Things are tough just after you buy your first house, but gradually, your disposable income increases. It’s like climbing a hill.

How long the journey to prosperity takes depends on interest rates.

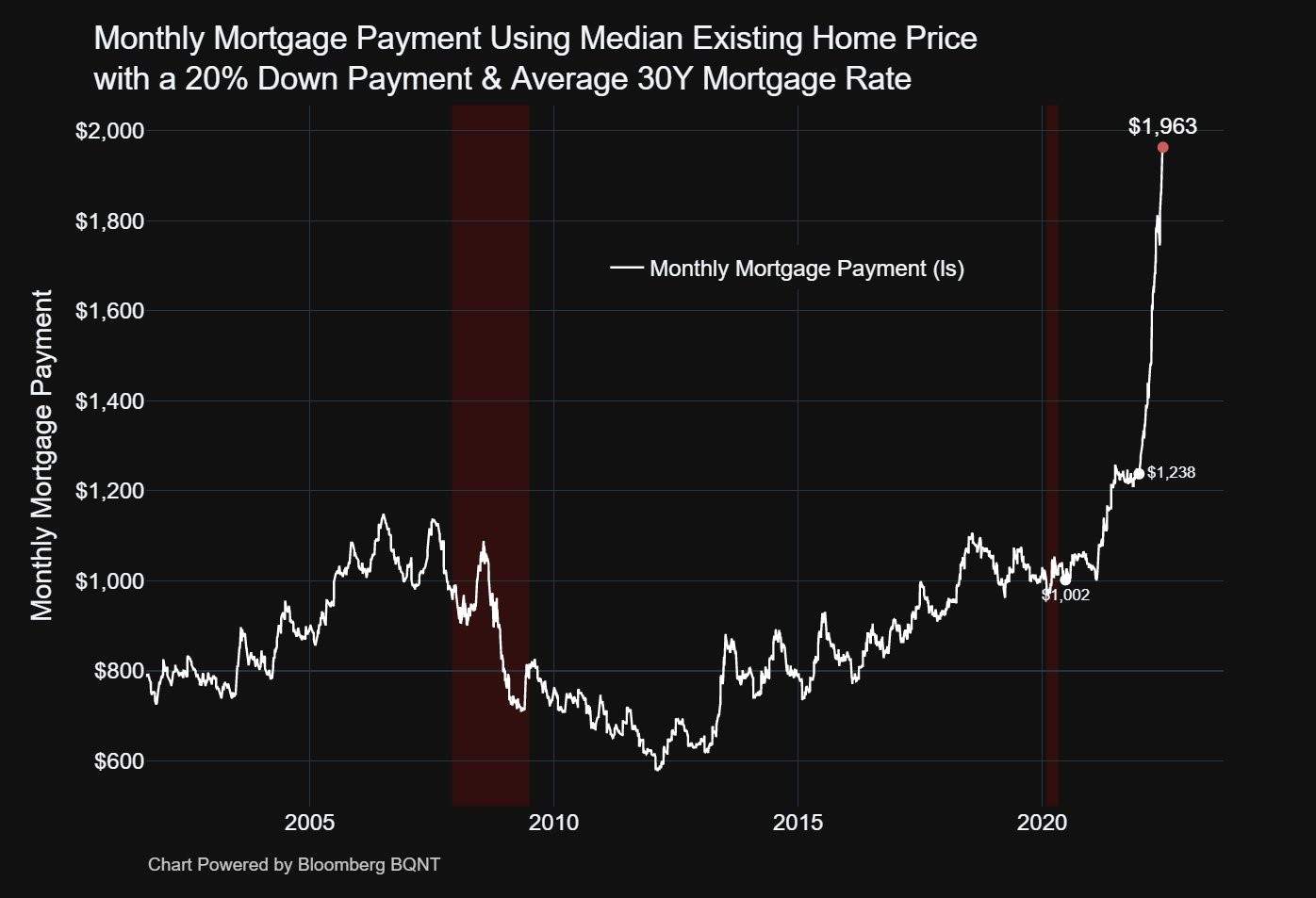

The chart below shows the mortgage payment on a median existing U.S. home:

For most of the last 20 years, the mortgage payment on such a home ranged between $800 and $1,000.

This year it’s almost doubled … in just a few months.

But that’s just the start.

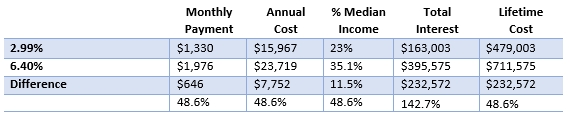

The table below shows the long-term consequences of an increase in mortgage interest rates. I’ve chosen my own rate (2.99%, locked in a few years back) and the recent quote for a standard 30-year mortgage. The figures assume the house costs the current median price for an existing home, $395,000:

Here are the key takeaways:

- The monthly, annual and lifetime costs of buying a home are nearly 50% higher than they were just a few months ago.

- Every year, a house will cost nearly $8,000 more. That’s almost $650 a month more going to interest.

- Mortgage payments have gone from 23.6% of the median U.S. household’s income to over 35%. Anything over 30% is considered distressed, which puts the household at financial risk.

- Over the lifetime of a 30-year mortgage, the household will pay over $230,000 more in interest.

The implications should be obvious. Every penny that goes toward higher interest costs is a penny that won’t be spent on other things.

People will eat cheaper food. That’ll be worse for their health, but they won’t be able to afford the same quality of health care.

They may have to scale back on their educational aspirations, purchases of durable goods and leisure activities.

But the rot doesn’t stop there.

The businesses that provide the very elements of prosperity will also see their revenues fall as consumers cut back.

So, they’ll reduce their own investments and hiring, contributing to a slower economy.

In a vicious cycle, that will make it harder for households to climb their way to prosperity.

With so much of their income going to housing, households will save less, which will reduce the demand for stocks in 401(k) plans and individual retirement accounts.

Although wealthy households will pick up some of the slack, we’ll hear a “giant sucking sound” as money leaves the stock market and goes to the mortgage finance industry instead.

Buying the Essentials

The key to happiness is a willingness to adjust your expectations (within limits, of course). Raging against the inevitable doesn’t change anything except your blood pressure.

The U.S. economy will likely go through a period of extended weakness as higher interest rates direct more and more of the nation’s income into interest payments rather than the real economy. That’s going to lead to a decline in consumer expenditure on things they don’t absolutely need.

So, what’s an investor to do? Simple: Buy companies that make things people absolutely need.

We’re at a unique moment in stock market history. Most investors — especially those who “grew up,” financially speaking, after the great financial crisis — haven’t yet come to terms with the fact that the huge gains of the last decade are over.

That’s created a unique opportunity for you.

The stocks of many companies that sell consumer staples are still below their long-term valuations. Most of them pay hefty dividends.

That’s precisely why my strategy going forward is to buy those companies. No matter what happens, their earnings will continue, as will their dividends. And as the rest of the market gradually realizes that they’re the only game in town, money will flow into them, pushing up their share prices.

As I said, forewarned is forearmed … so make the shift now before everyone else!

Kind regards,

Ted Bauman

Editor, The Bauman Letter