Seven days into an advertising boycott against Facebook (Nasdaq: FB), the social media giant is on the ropes.

You see, businesses pay to have their ads featured as sponsored content in the Facebook app and on the website. This ad revenue is where Facebook makes its money.

And after a week, the boycott has cost Facebook millions in advertising dollars worldwide, as brands including Coca-Cola and Ford take the month off.

The company and its chief executive officer, Mark Zuckerberg, are regularly subject to accusations of racism, hate speech, election meddling and unjust firings.

And now, companies and regulators have added to the social pressure for change at the $670 billion company.

The stock hasn’t seen the impact … yet.

Facebook was one of the few stocks that traded at fresh all-time highs ($245.19 per share) as the platform benefited from a stay-at-home environment.

With bars and restaurants in some states reopened — or planning to in the near future — Facebook needs to capitalize on this momentum and push shares even higher.

The risk now is that the weight of the boycott will cause the share price to plunge in the coming weeks.

Today, I’ll break down the fundamentals, sentiment and technical analysis to see if Facebook is a stock you want to bank on or tank over the next 12 months.

Click below to watch my latest Bank It or Tank It and get my insights on Facebook:

This week’s features a popular stock that I’m sure pretty much everyone uses.

And if you haven’t used it, then I know that you’ve heard of it.

It’s Facebook (Nasdaq: FB).

And this stock is always caught up in some sort of drama, causing the stock to fluctuate up and down. It’s definitely one of the companies that has benefited over the economic lockdowns that we were in. And as the whole economy is slow to open back up, Facebook is a stock that’s going to continue to thrive.

So today, we’re going to be following our Bank It or Tank It analysis by taking a look at the fundamentals, the sentiment and the technicals to figure out if this is a stock that we want to bank or tank over the next 12 months.

This is a stock that’s always under pressure against how it handles ads and advertisers that are coming to its network.

What kind of content are they allowed to post?

Twitter is another company always caught up in this kind of feedback. The company blocks certain tweets, but allows other tweets.

And now, the regulators are coming for them. They’re looking to implement some sort of policy on these companies to keep them in check.

But when we step back and look at what these social media platforms offer, what Facebook is doing right now in connecting people all around the world, it’s really one of the only things left in the economy for people to turn to, for enjoyment, interaction and socialization.

I know my kids have really strung to the Xbox platform, where they play video games online with their friends, because they’re chatting and socializing.

For different generations, they’re using Facebook or they’re using Twitter to interact, because this is the main source of content that we’re seeing at the moment.

With the pandemic, our main forms of entertainment over the past six months have been on YouTube, Twitter, and Facebook. Companies that charge you nothing for the content that you receive.

Facebook has made money and thrived over the years by charging companies to place ads on its platform. And more importantly, these ads can specifically target certain demographics, certain types, certain likes that you have on Facebook based on your profile.

So they can be very specific and way more efficient than what you would see on a normal TV ad.

A lot of companies have pulled the plug on advertising on Facebook because of the drama on how it manages content on its platform.

But we’ve seen plenty other companies step in to fill that void and continue to help Facebook shares drive higher.

So today, we’re going to look at the fundamentals, the sentiment and the technicals to figure out if this is a stock that we want to bank on. We’ll start with the fundamentals of Facebook by taking a look at key stats.

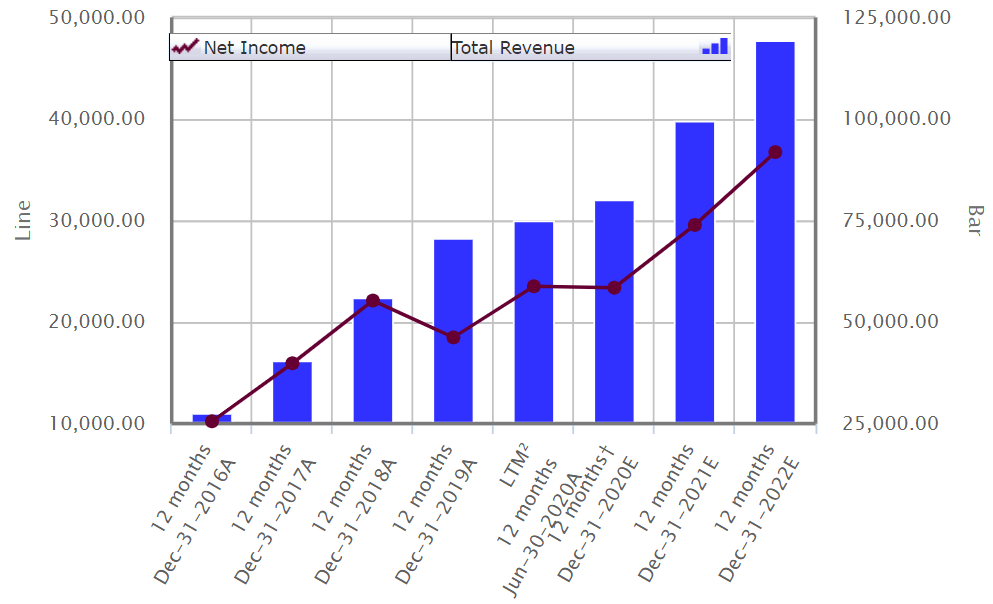

Facebook – Key Stats

This is a chart of revenues and net income. Revenue is the blue bars on the chart (on the right-hand side); and net income is the line on the chart (on the left-hand side).

The first thing that stands out to me is the clear uptrend. It starts on the bottom in 2016 and then continues to consistently climb higher. And again, this is solely driven by ad revenue for Facebook.

So, this is a company that’s really figured it out.

It’s thriving in this market. You can see consistent increases for both the bottom line and revenues from 2016-2018.

We’re seeing strong demand to advertise on this platform.

Net income took a little bit of a step back, and part of that is because Facebook’s ad revenue is the sole focus at the moment. It has its hand in other areas too, like virtual reality with its Oculus headset.

And I think that’s going to be huge in the future, but when we’re looking at it over the next 12 months, Oculus is not really going to be a game changer in that timeframe for the fundamentals that we’re looking at in the company.

So while the net income took a dip in 2019, you can see that it ticks back up in the June 2020 results.

Revenue didn’t go up too high, either. So it’s seeing a big jump in 2021 again, continuing into 2022.

I would say that, as it factors in the pandemic, it’s a positive for the company because it has seen strong increases in advertising throughout this pandemic.

The only problem I see that could hit Facebook is that the economy basically went through a recession.

So, there’s some softness in the economy right now. And as that turns around, which seems to be the case, as long as we don’t shut down the economy again, things are starting to reopen and pick back up with economic growth.

That’s going to boost more companies’ confidence to spend on advertising and pump more money into Facebook.

While it’s going to be a little volatile to get there, I think the 2021 revenue expectations are going to be in line with what Facebook sees. So this is a chart where the fundamentals are really sound and looks great.

Now, let’s take a look at a few comparable companies to see how Facebook stacks up…

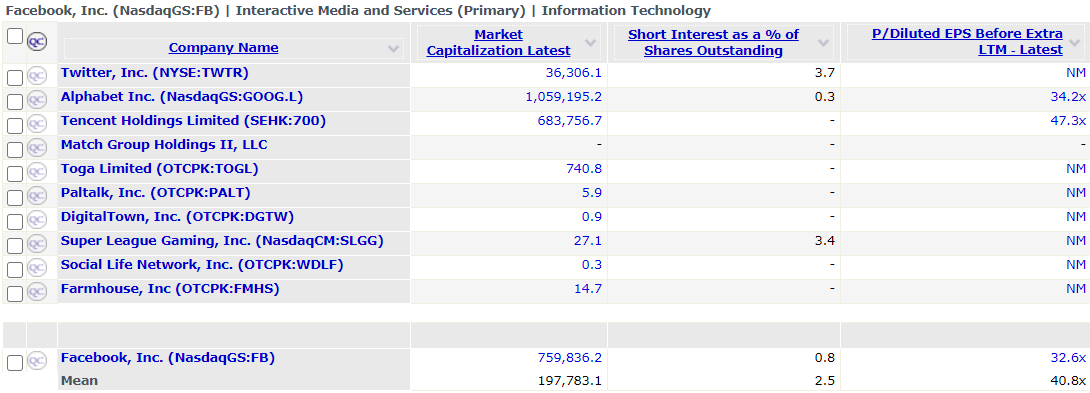

Measuring Facebook and the Competition

Some of these stocks, like Twitter and Alphabet (Google’s parent company), also rely on a lot of advertising. Then there are some other less popular social media companies.

The market caps give you a perspective of how large Facebook has become. At over $759 billion Facebook’s market cap is the second-largest company on the list. Only internet giant Google, is larger — with over a $1 trillion market cap and one of the largest companies on the stock market.

The average of these key competitors is $197 billion. So Facebook is definitely a large-cap stock at this point, which begs the question: How much growth potential is there for the stock?

The reason Facebook is valued so high among its peers is because it’s found a way to monetize its platform, whereas Twitter has struggled with its ad networks. You can see why it’s still just at a $36 billion market cap, which is nothing compared to Facebook’s $759 billion.

When we look at the short interest of Twitter, 3.7% of its outstanding shares are being sold short, meaning people are betting against the stock. For Facebook, it’s just 0.8%. Both are relatively low compared to companies that investors would be very bearish on, so this is nothing of major concern.

With the price-to-earnings ratio on the end, it gives us a perspective of how the industry is being valued. Looking at the mean for the stocks listed, that’s 40 times earnings.

You can see many of these companies don’t even have a price-to-earnings ratio, so it doesn’t impact it. Other companies don’t have a price-to-earnings ratio because they don’t have positive earnings.

So Facebook, at 32 times earnings, is fully valued. We wouldn’t expect that price to get much higher. But being a social media stock, it’s definitely pricing in a premium here for growth.

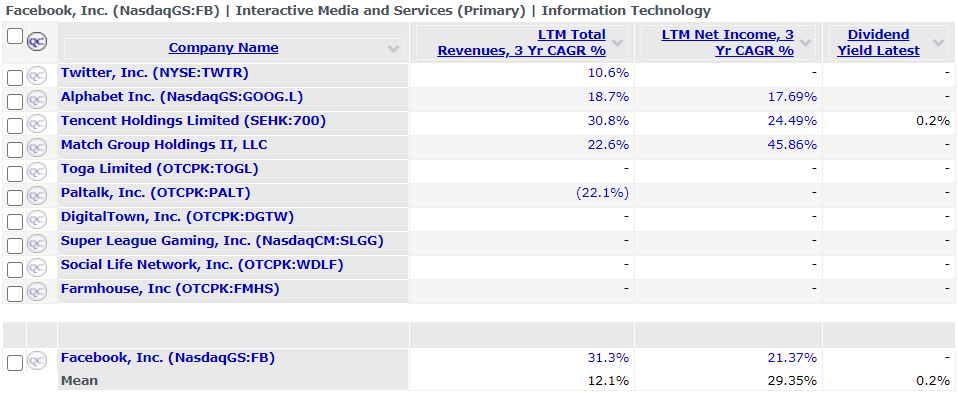

Now, for total revenues, three-year compound average annual growth rate (CAGR) and net income, Facebook’s kicking butt. It‘s at 31.3% revenue growth, on average, over the last three years and 21% net income.

That’s the bottom line, growing at an average rate of 21% per year. The crazy thing is that’s still below the mean of 29%, mainly because outlier Match is at nearly 46%. Only two others — Tencent and Alphabet — are seeing net income growth, at 17% and 25%, respectively.

But Facebook is really hitting it hard on the revenue side at 31.3%. It’s the highest of these companies, and that growth trickles into stronger net income.

So, I like what I’m seeing with the high revenue growth.

It’s found a model that works with monetizing its content, and I think that’s going to drive even higher net income growth in the coming years.

Now, I use dividend yield to get an idea of where its focus is. Either returning cash to shareholders or investing in growth.

These social media companies are still mainly focused on growth at this point, and that’s a good thing.

Even with Facebook and Google being large-market-cap stocks, they continue to focus on growth, instead of income.

Analyst Recommendation

Now, when it comes to the sentiment, I always look at what the analyst rating is for the stock. How Wall Street views it, in other words…

Based on S&P Capital IQ information, out of 43 analysts who cover the stock, it’s rated at 1.51 and is listed as “outperform.” A solid buy.

A 1 is an extreme buy; 5 is an extreme sell. So, it’s definitely screaming a strong sentiment reading here when we take a look at how Wall Street views the stock.

The Technicals

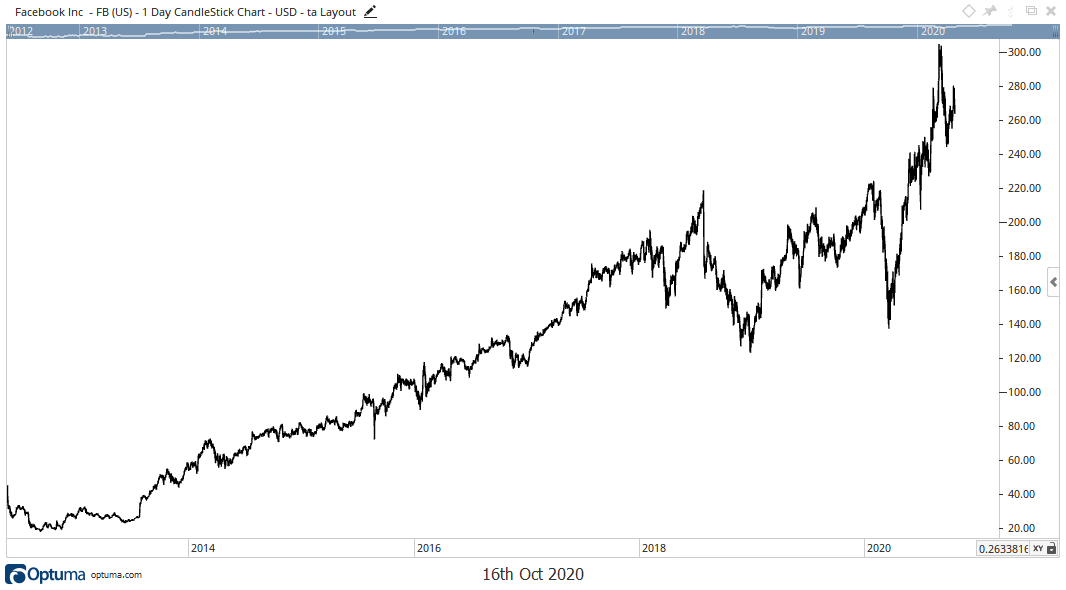

Now, my favorite part: A look at the price chart to break down the key levels to watch and take another look at sentiment based on the 200-day moving average.

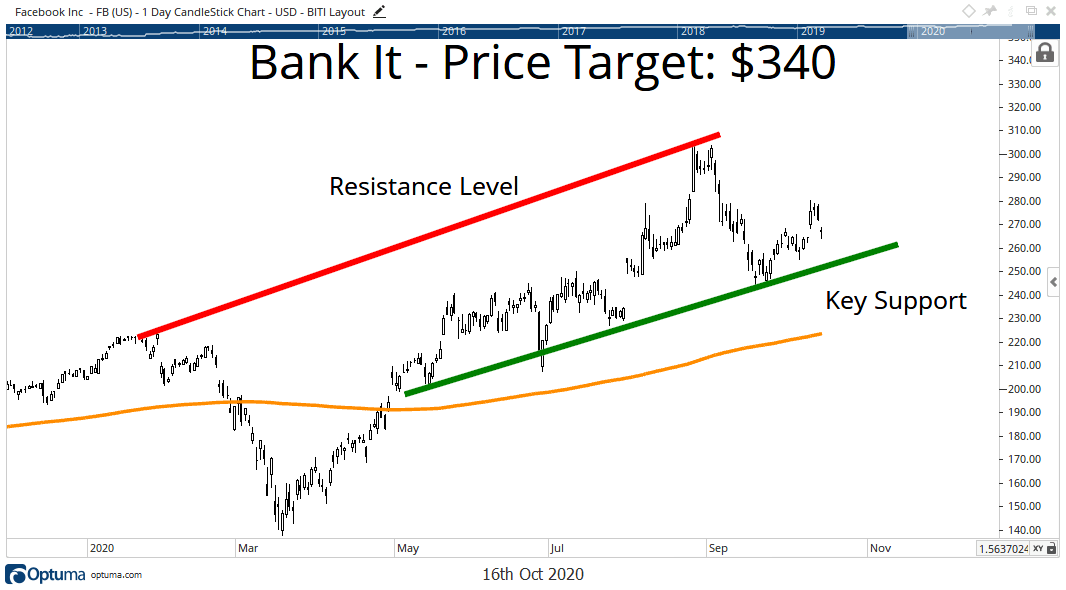

Just to give you an idea of what Facebook has overcome, it was just a $20 stock back in 2012. Now it’s more than $250.

So this is an extremely big run for the stock.

Even though it took eight years, this is still a massive run. And when you look at the uptrend, it’s still intact. Even after all the volatility that we’ve gone through over the last couple of years … the pandemic, everything happening in the world and the economy, we can see there’s a strong uptrend.

Now, when we take a look at the shorter-term key levels, we have a rising resistance line connecting the peaks. So that’s going to be a clear resistance area as Facebook continues to climb. But it still gives the stock plenty of upside.

My price target has the stock climbing back to the high end of this price channel, around $340. We just need the stock to find support at the short-term support area.

Facebook set new highs at the end of August. And I’m excited to see the stock continue to climb higher.

A Look at the Checklist

Now, let’s run through my checklist.

- Fundamentals: We looked at the fundamentals for Facebook, and the revenues and net income ran solid uptrends. So, I expect that to continue. It’s been able to get it done in the years past. And now, it’s overcome the hump, with strong income on the bottom line. And I think we’ll see that continue. So, fundamentals get a check mark.

- Sentiment: For sentiment, Wall Street’s bullish on the stock. It’s rated as an outperform. The stock is above its 200-day moving average, the yellow line on the chart above. So, I believe that this stock has a check mark for sentiment.

- Technicals: And we just looked at the key levels. With only one clear rising resistance, meaning that Facebook will have to move up even higher to hit it, I think we’re seeing the stock in a strong position to continue heading higher. So, it gets a check mark for the technicals.

And that means one thing… With three check marks on the board, this is a Bank It stock.

Ultimately, Facebook is a stock I see heading higher. And in a volatile market like this, it’s important to find the stocks that you can bank on and trust to go higher. And Facebook’s one of those.

Regards,

Chad Shoop, CMT

Editor, Quick Hit Profits