I almost fell off my chair…

My father was in his 60’s at the time.

And he’d just made what could’ve been the biggest financial mistake of a lifetime.

My pop was a very conservative investor and didn’t have the temperament for stock investing.

No matter how many times I told him not to look at his brokerage statement, he couldn’t help it.

He’d panic when the market was down, and when it rose, he wanted me to double down.

In 2000, the dot-com bubble burst. Over the next two years, the stock market fell more than 50%.

He had reached his pain threshold and couldn’t take it anymore.

So in 2002, he swore off owning stocks and told me to sell most of his holdings.

I was only able to convince him to keep a few stocks like Apple and Berkshire.

A few years later, on a Sunday afternoon, he let slip that he had put a “few dollars in annuities.”

When I saw the rate he locked into, I thought it was a misprint.

My father was sold a 2% annuity and invested about $100,000.

A financial planner played on all his fears of stock market volatility into a handsome commission for himself. Planners make between 3% to as much as 8% selling annuities.

When I asked him why he bought the annuity, his response was that he was a “conservative” investor.

I shared with him that there’s a big difference between being conservative and being a sucker…

The Trap of Investing in Annuities

I’ve shared with you in the past that if you can’t handle the stock market’s ups and downs — buy Treasury bills instead.

And I told my dad the same thing. Why buy a 2% annuity … when a Treasury bill was yielding 4%?

It took me a while, but I finally convinced him to break the annuity, take the penalty and let me invest his money in great businesses trading at bargain prices.

That was in 2005.

And over the next 14 years (he passed away in 2019), he racked up huge gains in the stocks he had in his portfolio such as McDonald’s, Apple and Lockheed Martin. This was in addition to his Google and Berkshire holdings he didn’t sell.

His golden years were a lot more golden as a result.

Now, in 2023, it seems like millions of American retirees might fall into the same trap — especially with headlines like this:

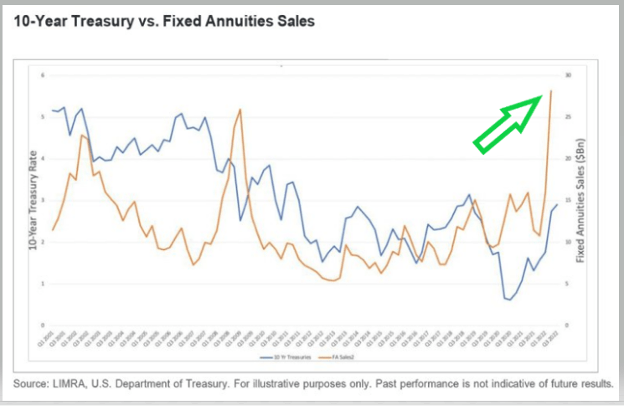

Due to rising interest rates, falling stocks and uncertainty about the economy, annuity sales surged over 20% last year.

The 10-year Treasury yield rose from around 1% in February 2021 to now close to 4%. You can see the spike in annuity sales (gold line) and 10-year Treasury sales (blue line):

Behind the Curtain

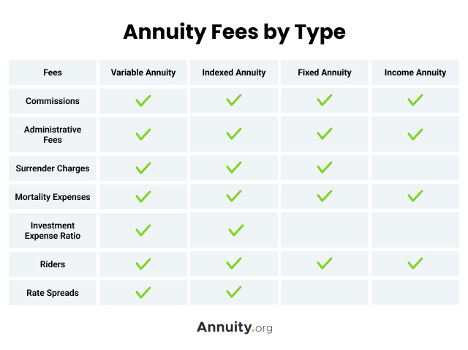

Here’s a quick rundown of all the fees involved with owning a typical annuity:

That doesn’t even include penalties like the ones my pops paid for withdrawing his money ahead of schedule!

While your money is locked up in an income annuity, you lose control over it.

And as I mentioned above, income annuities often won’t keep up with inflation at today’s rates.

Even after last year’s rate hikes, the best annuity yields, of around 5%, are still paying out less than inflation which is running 6.4%.

Liquidity can also be a major concern. Most annuities offer regular but somewhat limited liquidity. But sometimes there’s none at all.

When you buy an annuity, here’s what you are doing:

- Handing over control and liquidity to financial planners.

- Charged penalties if the annuity is cashed in early.

- May underperform the rate of inflation.

Bottom line: There’s really only one thing you need to take away from this today…

If you have a long-term time horizon, nothing beats investing in stocks.

So here’s what I recommend.

Invest Like an Owner: Don’t Invest in Annuities

Now you know why I would never buy annuities.

But I’m not sour on annuities as a business, just as an investment.

It’s much easier and cheaper to buy a 10-year Treasury bond if you want a fixed return.

Or if you want income, I’d much rather own Johnson & Johnson (NYSE: JNJ). The dividend yield is currently about 3% and you also have the kicker of the share price rising as earnings grow.

The way to make money with annuities is by owning the companies that sell annuities. This way we benefit from the growing appetite that investors have for annuities.

That’s exactly what I started doing at the end of 2021.

Inflation was soaring, after Biden’s $1.9 trillion stimulus package. I quickly saw that it wasn’t a matter of if rates would rise, it was just a matter of when.

As interest rates rise, annuities sales pick up. You have more buyers locking in 4% returns than you would 1% returns. That’s why rising rates are a strong tailwind for annuity sales.

On November 3, 2021, I told my Alpha Investor subscribers to buy shares of a unique Fortune 500 financial stock — due in large part to the cash flow from its rapidly growing annuities business.

Then on December 29, 2021, I recommended subscribers buy an alternative asset manager that had recently made a huge commitment to the annuities business.

And in January of 2023, I recommended a leader in the variable annuity market. Trading at just 2X earnings, the stock has already soared more than 33% since we added it about six week ago.

To get the details about my strategy, click here and see how we’re buying the companies selling the annuities.

Over time, buying businesses like these, when they trade at attractive prices, is a pretty simple way to ride the tailwind of higher annuity sales.

Regards,

Founder, Alpha Investor

P.S. When I buy a stock, I want it to do one thing: Show me the money.

And that’s something many companies couldn’t do last year.

When the Federal Reserve started raising rates in March 2022, stocks took it on the nose.

By the end of 2022, 40% of the Russell 2000 Index were unprofitable.

That’s why I focus on great businesses that are making money.

When you buy a great business at a bargain price … higher returns are usually inevitable.

In fact, there’s one class of stocks that are outperforming the market by a country mile.

Before my next buy alert, check out my special video here to get the full story on some of the best stocks for 2023 and beyond…