Story Highlights

- One chart shows the stock market hates junior mining companies right now.

- But large-cap companies got a tailwind from the gold price.

- They’ll start buying out undervalued tiny companies — so contrarian investors should be on the lookout for junior miners with promising discoveries.

Tiny exploration mining companies — I’m talking $300 million cap and smaller — usually don’t produce metal yet.

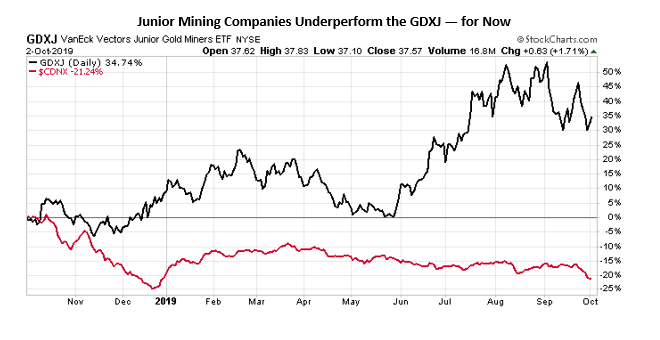

Gold and large gold miners rallied recently. These junior mining companies didn’t follow.

I’m calling it now: This is going to drive the major companies to acquire junior miners with the most promising discoveries.

You see, juniors are the companies building new mines or developing new deposits.

That doesn’t mean that they are worthless. It means they carry more risk.

And that scares investors away. But I see something in the months ahead that the market is ignoring.

The Market Undervalues Junior Miners

Take a look at the chart below:

The black line is the VanEck Vectors Junior Gold Miners fund (NYSE: GDXJ). It tracks companies with market values in the billions, including Kinross Gold and Yamana Gold.

The red line is the TSX Venture Exchange. That’s like the Dow Jones Industrial Average for tiny mining companies.

It holds 939 small miners. As you can see, the small miners underperformed the GDXJ by 55%.

This is because investors think companies on the Venture Exchange are riskier.

Almost all the companies in GDXJ produce metal now. The tiny companies listed on the TSX Venture don’t. So, the value of these commodity stocks depends on your view of the future.

The chart above shows us that the market doesn’t think much of the future of mining.

The thing is, mines don’t live forever.

A mine is like a loaf of bread in a sandwich shop. You make so many sandwiches, and then you need a new loaf of bread. The TSX Venture Exchange is the bakery.

These tiny companies are finding the new mines that the companies in the GDXJ need in order to keep producing metal.

Prediction: Buyouts Are Coming

Pan American Silver, for example, is a $3.4 billion silver and gold producer.

Its most promising new discovery isn’t Pan American’s.

A tiny, $23 billion microcap miner discovered it.

Pan American partnered with this company to earn a partial interest in the new discovery.

So, a $3.4 billion mining company partnered with a $23 million mining company to find its next mine.

The usual outcome of such a partnership, if there is a successful discovery, is a buyout of the junior partner for a huge gain.

For instance, in 2016, the giant miner Goldcorp acquired junior Kaminak Gold for $520 million. Goldcorp wanted to acquire Kaminak’s Coffee project in the Yukon.

Sometimes it’s back-to-back acquisitions.

In 2010, Fronteer Gold paid $281 million for junior AuEx Ventures, in order to control the Long Canyon gold project — then giant gold miner Newmont Goldcorp bought Fronteer for $2.3 billion.

We saw something similar recently.

In 2016, Nevsun Resources acquired Reservoir Minerals for $365 million. Nevsun wanted access to the Timok copper-gold project in Serbia.

Then, in 2018, mining giant Zijin Mining bought Nevsun for $1.4 billion.

My point with all these examples is that the junior partners made important discoveries — only to be bought out by larger mining companies.

That’s the kind of market we are in today.

Junior mining companies are undervalued. Larger mining companies had a tailwind. They have capital to spend and are looking for the right targets.

As the gold price rises, this separation will get larger. I expect to see consolidation in the junior mining space as the most promising new discoveries get snapped up while the gap is still large.

Good investing,

Matt Badiali

Editor, Front Line Profits – natural resource stock strategy

P.S. I love buying in on a trend when the average investor is selling. In my premium service Front Line Profits, I find small-cap companies that are set to skyrocket — including junior miners whose discoveries make them perfect candidates for buyouts!