Did Somebody Say “Blue Light Special?”

Great Ones, we’ve long talked up the average consumer’s willingness to overspend like no tomorrow.

You might fancy yourself a thrifty shopper, but c’mon: Who doesn’t at least shell out for the good frozen pizza every once in a while? No?

Call it a willingness, call it an active addiction … inflation has certainly made it difficult to “treat yourself,” however your budget defines that. (Especially with, you know … the sheer cost of existing.)

But hey now, my fellow penny pinchers and coupon clippers: Discount sales are headed your way! Just … not for the reasons you might expect.

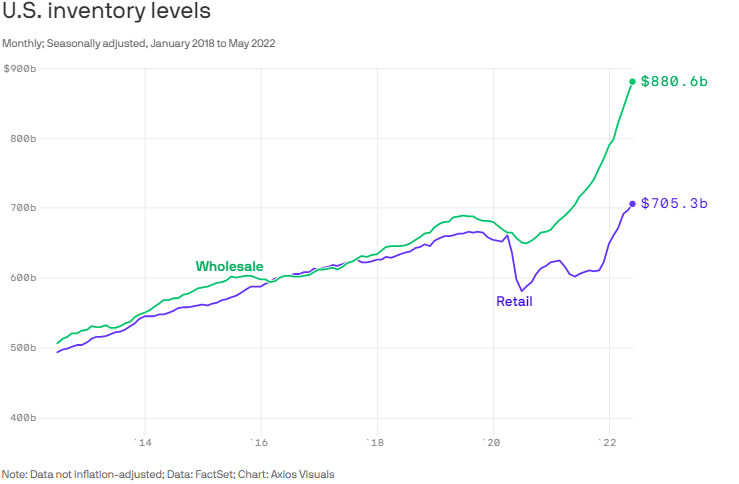

Throughout the course of the pandemic, earnings reports from retailers usually boiled down to one of three complaints: labor, inflation and the supply chain. Don’t worry: We’re not getting into the inflationary nitty-gritty today, nor will we talk up the labor market. (Phew!)

Because today, the supply chains that have been binding retailers all pandemic long … are starting to ease up. New data shows warehouses are filling up with all kinds of junk — too much stuff, in fact.

As the chart below shows, retailers’ inventories are now overstocked above pre-pandemic levels:

Wow, would you look at that?

It’s all the back-ordered and unavailable stuff you wanted to buy during the pandemic, finally reaching retailers’ backrooms. We’re talking appliances, sweatpants, hoodies, furniture, packaged goods, TVs and other assorted home entertainment junk.

Hey … wait a minute! This sounds awfully familiar. You trying to give me déjà vu?

Nope, that just means you’ve been keeping up on your Stuff. That or you’re a Target (NYSE: TGT) investor who viscerally remembers TGT stock dropping 25% the morning it warned of these inventory troubles … over a month ago.

See, Target saw other retailers like Walmart (NYSE: WMT) starting to struggle with excess inventories that they’d ordered to meet consumer demand in the pandemic.

The problem is that now, in a somewhat-kinda-maybe-post-COVID environment, consumers aren’t demanding those specific items anymore. Suddenly those overstocked inventories aren’t so appealing, after all.

So what does Target do? Get the worrying over with ahead of time. Target warned its investors (and teased its shoppers) that many products would be deeply discounted and out on clearance in the coming months.

Now you might finally be able to snag some good deals at Target. But if you’re a TGT investor, this means potentially devastating margins on those discounted goods next time earnings season rolls around.

And let’s remember: Target is trying to get ahead of this problem before it’s too much of a problem, clearing out the back stock at a loss to refocus on what consumers actually want to buy these days. Other retailers? They’re probably still wondering whether to disappoint investors now or later.

That’s just the way the supply chain goes … like a sprung Slinky smacking you back in the face.

At a time when literally everything costs an arm, leg and kidney, these discounts are excellent news if you’ve been holding off on buying that new TV.

But if you’re seriously invested in the retail sector? Get ready to hear companies complain about falling margins instead of supply chain holdups next time earnings rolls around.

But hey, at least the grain is starting to flow again … right?

Want Bear Market Riches? Do This…

The bear market hasn’t stopped Andrew Keene from outperforming the market all year. And he doesn’t even need to short stocks…

Since February 15, Andrew has posted a win rate of 73% on closed positions, trading ONLY CALL OPTIONS in a bear market.

In the Trade Room, his followers have seen gains of 48%, 56% and even 100% in as little as 15 minutes. And they get as many as 10 daytrading ideas EACH DAY, hand-selected by Andrew himself.

Access to this coveted club is opening up for the first time ever. Follow along with Andrew every morning and watch your portfolio grow before lunchtime.

…to chart a course on the future of its company, that is.

After teasing Wall Street all week about whether it would fly off into the sunset with JetBlue or Frontier, Spirit Airlines (NYSE: SAVE) surprised literally no one when it announced a postponement on today’s shareholder vote.

Noooo! Just. Make. A. Decision. Please!

I share your sentiments, Great Ones. I really do. But can you fault Spirit for trying to squeeze every last drop of shareholder value out of this merger madness? I mean, the airline’s definitely, 100% doing this for the interest of its investors and not itself … right?

To make matters more interesting, both Frontier and JetBlue have upped their antes the closer we’ve gotten to D-Day. That’s … umm, Decision Day, btw. We’re not storming any beaches over here.

In other words, Spirit can smell desperation from both parties to come out as the winner of this high-flying duel. And it’s banking on getting even more bang for its buck — erm, fleet, as we approach another meeting milestone.

Spirit shareholders aren’t helping matters either. With Spirit stock up another 4.5% today following the company’s decision delay, investors have signaled this is one layover they’re willing to wait for.

Constellation Needs A Lucky Star

Constellation Brands (NYSE: STZ) just can’t seem to find its northern star to make its way back into investors’ good graces this quarter.

The brewer of beer, wine and spirits experienced a brief boost in share price this morning on news of higher-than-expected earnings — $2.66 per share, to be exact — but tapped out midday after investors caught wind of its lowered financial forecast.

While alcohol sales are likely to remain strong through the end of the year (gotta get through this recession/not-a-recession somehow, right?), Constellation expects fiscal full-year earnings to fizzle nearly a dollar lower than its initial projection.

Can you guess what’s dragging on the drinkmaker’s profits?

That’d be the company’s investment in pot purveyor Canopy Growth (Nasdaq: CGC), which Constellation currently has a $556 million loss in. Talk about a buzzkill…

Unfortunately, until federal legalization takes hold in the U.S., Canopy’s growth is gonna be limited in its size and scope … meaning it’ll continue to meddle with Constellation’s earnings each quarter.

Given everything else that’s been going on in the market lately, this particular drink was too bitter for STZ investors’ tastebuds, and the stock sank nearly 4% lower on the news.

Bed Bath & Beyond’s (Nasdaq: BBBY) back on our leaderboard today — and this time, it’s got a lead foot down on the accelerator as it leaves (or at least considers leaving) Buybuy Baby in the rearview mirror.

Are you trying to tell me it ain’t never lookin’ back on Buybuy Baby, and that’s a fact?

I see you’re up-to-date on your ‘90s country hits! What else don’t we know about one another, Great Ones? (How about this: Got a favorite song — country or otherwise? Send it our way. You’ll get bonus points if you can tie it into an investing angle, Great Stuff style!)

Anyway, enough with these Thursday Throwbacks — it’s the Throwdown you’re here for. Or in Bed Bath’s case, the throwaways.

It’s not that there’s zero value in Bed Bath’s baby gear chain … far from it. It’s just that with all the other things tied to the company, it’s received unwanted attention from activist investors who believe the only way to save the struggling retailer is to spin off its best parts for profit.

See, back during the holiday shopping season, Buybuy Baby’s same-store sales actually grew at a healthy clip even as Bed Bath’s core business circled the drain.

But left in now-excommunicated Mark Tritton’s hands? Yeah…

Even the booming baby chain’s started to slip under his poor excuse for management. And the way activist investor Ryan Cohen sees it, the only way to save the now-struggling business segment is to sell.

Poor Sue Grove. She couldn’t even have one day of peace in her new role as interim CEO before the sharks started to circle. But at least investors will have a better sense of the company’s future depending on how she handles this new debate.

What do you think, Great Ones? Should Bed Bath sell and pocket the profits? Or hold and hope for brighter baby gear sales ahead?

Don’t forget to send us your stock-related songs and investing soliloquys! GreatStuffToday@BanyanHill.com is where you can reach us best.

In the meantime, here’s where you can find our other junk — erm, I mean where you can check out some more Greatness:

- Get Stuff: Subscribe to Great Stuff right here!

- Our Socials: Facebook, Twitter and Instagram.

- Where We Live: GreatStuffToday.com.

- Our Inbox: GreatStuffToday@BanyanHill.com.

Until next time, stay Great!