All investors eventually consider income. But it’s often when they’re older.

They may discover that Social Security is lacking. Then they realize their nest egg isn’t big enough. These realizations can lead investors to form bad decisions which are all too common.

That’s because receiving sufficient income requires large amounts of capital. For example, if you want $1,000 a month, you need $300,000 in Treasurys earning 4%. Many, probably most, investors don’t have that much.

Realizing they don’t have enough capital, investors tend to look for alternatives.

One alternative known as structured notes has gained popularity in the past few years. Investors allocated $94 billion to these notes last year. That was slightly less than the $101 billion they bought the year before.

Investors seem to like the limited downside these notes offer. Let’s take a look at an example to understand how it works and to see if these are really worth the hype…

A Cap that Cuts Both Ways

Let’s say a broker offers a two-year structured note tied to Tesla at $250/share with 20% downside protection and a 4% quarterly coupon (16% per year).

You decide to invest $1,000. You get paid 4% ($40) every quarter as long as Tesla is above $200. That price is the level where the 20% downside protection kicks in.

If Tesla is below $200, you don’t get the $40 payout.

At the end of two years, if Tesla is above $200, you get your $1,000 back. If Tesla is below $200, you get $800 back since your loss was capped at 20%.

That cap cuts both ways. Let’s say Tesla is at $500 at the end of two years. You collected $40 every quarter for a total of $320. You also get your $1,000 back. Your $1,000 investment grew 32% rather than 100%.

Advocates of structured notes will argue that it’s not fair to compare the returns to the stock. It might be better to think of the note as a bond. A Tesla bond maturing in two years carries a yield of 2%. It trades at a premium, so your actual income would be less than that.

Compared to a bond, the structured note looks good. But that may not be the right comparison.

You could cap your loss in a stock with put options. In this case, a $200 put on Tesla expiring two years from now is trading at about $36. I won’t detail options pricing, but this means you are protected against losses that exceed 20%. The cost of this insurance is about 14% of the stock price. With this trade, you keep all of the upside in Tesla. You also have less risk than the note offers.

If you are bullish on Tesla, but worried, the put option is a better trade.

Unfortunately, Tesla doesn’t offer income. If you want 4% income, a two-year Treasury note offers 4.87%, guaranteed. That won’t be enough income. But for smaller accounts, there really isn’t a way to have it all.

Seeing Past the Hype

So when is the structured note better? It’s hard to say. Several studies have shown the notes are never really a good deal.

One academic study called “Engineering Lemons” offered an interesting comment on structured notes:

In my 2006–2015 sample of over 28,000 yield enhancement products (YEP) the securities offer attractive yields but negative returns. The products lose money both ex ante and ex post due to their embedded fees: on average, YEPs charge 6–7% in annual fees and subsequently lose 6–7% relative to risk-adjusted benchmarks. Simple and cheap combinations of listed options often first-order dominate YEPs.

Another study: “The Anatomy of Principal Protected Absolute Return Barrier Notes,” found that the products’ fair price was an average of 4.5% below the price investors paid. In other words, investors paid $1 for something that was worth $0.955.

There are other studies. Some show the notes cost 6.5%. Others show they cost 8%. No study shows they are the best income strategy.

Despite their proven shortcomings, investors continue to pour billions of dollars into structured notes. Why? Promises of income with limited risk are alluring. Especially when the costs are hidden.

But real income is difficult to find, especially in the low-rate environment we’ve lived through for years.

That’s why the team at Money & Markets decided to make it easier for investors like you to learn about better income investments and strategies that actually work.

They put together a special collection of income tips, tools and secrets of the wealthy in a brand-new book — Endless Income: 50 Secrets for a Happier, Richer Life. To learn how you can access your copy, click here.

Regards,

Michael Carr

Editor, Precision Profits

This Will Solve 2 Major Drivers of Inflation…

Two headlines broke this morning that would seem to be unrelated.

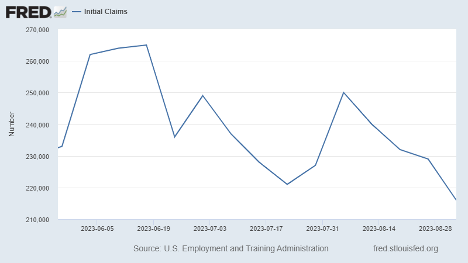

Initial jobless claims dropped hard last week, and are now sitting at multi-month lows.

Rising jobless claims had given hope to the idea that the labor market — one of the biggest drivers of inflation — might be finally cooling. But the sudden drop in claims shows that the job market remains exceptionally hot.

The other headline concerned productivity … which is another driver of inflation.

Rising productivity means we can make more with less. This is the key to raising living standards without getting stuck on a perpetual inflationary treadmill.

Well, about that…

The Labor Department revised its estimate of nonfarm productivity for the second quarter lower, from 3.7% to 3.5%.

Even 3.5% looks pretty darn good and would normally give me hope. But it followed a first quarter in which productivity growth was actually negative. Workers were 1.2% less productive in the first quarter of this year.

You don’t have to have a Ph.D. in economics to understand the connection here. When the job market is exceptionally tight, younger, more “green” and marginal workers that might ordinarily have a hard time holding a job, get pulled into the workforce. These workers are naturally going to be less productive than the ones that have been in the role for years, or even decades.

A hot labor market also tends to bring a lot of churn. When you’re constantly having to onboard and train new workers, you’re not getting much production out of them.

In the short term, there isn’t much of a solution here other than a recession that forces layoffs. And clearly, no one wants to see that.

In the longer term, technology will bail us out.

And it’s already starting.

Artificial intelligence and robotics automation will allow companies to produce more with less. And given the massive sums being invested here, we may be on the cusp of the single biggest explosion in productivity since the dawn of the Industrial Revolution.

If you want to delve into the emerging mega trend of AI, go here for Ian King’s #1 AI stock recommendation.

Regards,

Charles Sizemore

Chief Editor, The Banyan Edge