Russia’s invasion of Ukraine is official.

With tanks in the street, sanctions set to fly and Russia’s stock market in free fall, I take a moment to zoom out and look at the bigger picture for your portfolio.

Today’s video covers Russia’s motivations for going to war, the likely outcome for global commodity prices, and how you can safely grow and protect your wealth as history unfolds in Eastern Europe.

Transcript

Hello everyone. It’s Ted Bauman here, editor of the Bauman Daily and of The Bauman Letter with your Friday YouTube video. Well, a lot to cover today. I’m wearing my Viking T-shirt because I just flew over Iceland and Greenland on my way back from Amsterdam, my layover points from South Africa. Amazing to see that out the window. I have to tell you it’s something I’ve never thought I’d ever see, but there it is.

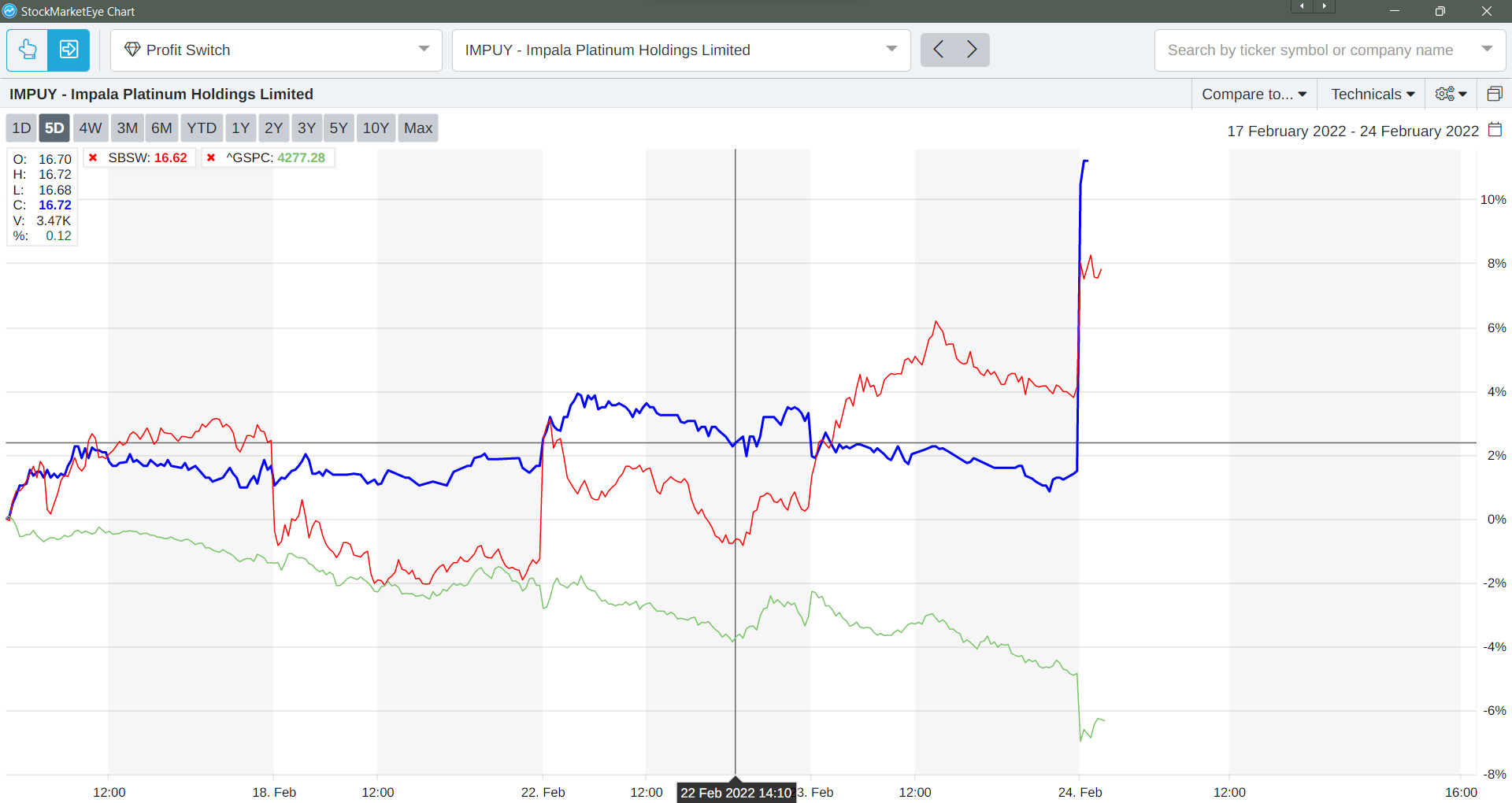

Today obviously the big issue is what’s going on in Ukraine and how that is going to affect markets. But let’s just reflect on the last video that I did where I talked about this issue. Here’s a chart that shows what happened to the stock I predicted, which was Sibanye Stillwater:

I’ve also thrown in Implats, which is another PGM producer. On the morning of the invasion yesterday you can see they did pretty much what I said they would do as opposed to the market. So I hope you made that play.

Now, don’t get the impression that I’m happy about the war. Some people wrote in and kind of implied that I was being amoral in the sense that I was looking for profits. Well, you’ve got to look for profits wherever they can be had. That doesn’t make war right, and I’m certainly opposed to this one as I would be to any war. But let’s just step back and review the situation. It’s not, strictly speaking, stock market material, but I am an economic historian and all also a fanatical military historian. What’s happening in the Eastern Europe situation right now is a lot of people compare it to Hitler and Czechoslovakia and the Sudetenland in 1938. But I think a better comparison is actually the Monroe Doctrine. Here’s a picture of James Monroe, the fifth president of the United States:

What all old Jim said was that as the Spanish empire in Latin America fell apart and as new republics were emerging to replace Spanish colonies in South and Central America, Monroe said, “Look, this is our backyard. If anybody, especially Britain or anybody else, tries to come and form military or political alliances, or try to these countries in a way that threatens us, because after all we’ve got Britain ruling Canada to our north. If you come in and start forming essentially geopolitical alliances to our south and circling us, we will fight you.” And in a sense that’s exactly what Putin is saying. Now, I’m not justifying what Putin is saying, nor would I justify what James Monroe did, but I just thought it was important to introduce that because it just goes to show that this happens when you’re a great power, this is something that great powers do. They get paranoid. They freak out. They want to protect their spheres of interest. It’s shocking, it’s unconscionable, it’s wrong, but it does have precedence historically. So I think it’s important to bear that in mind.

Now, one of the things that makes this whole situation so unbelievably sad is because this is an ongoing trend over the last 200 years. Here’s a cover of a book called Bloodlands by Timothy Snyder:

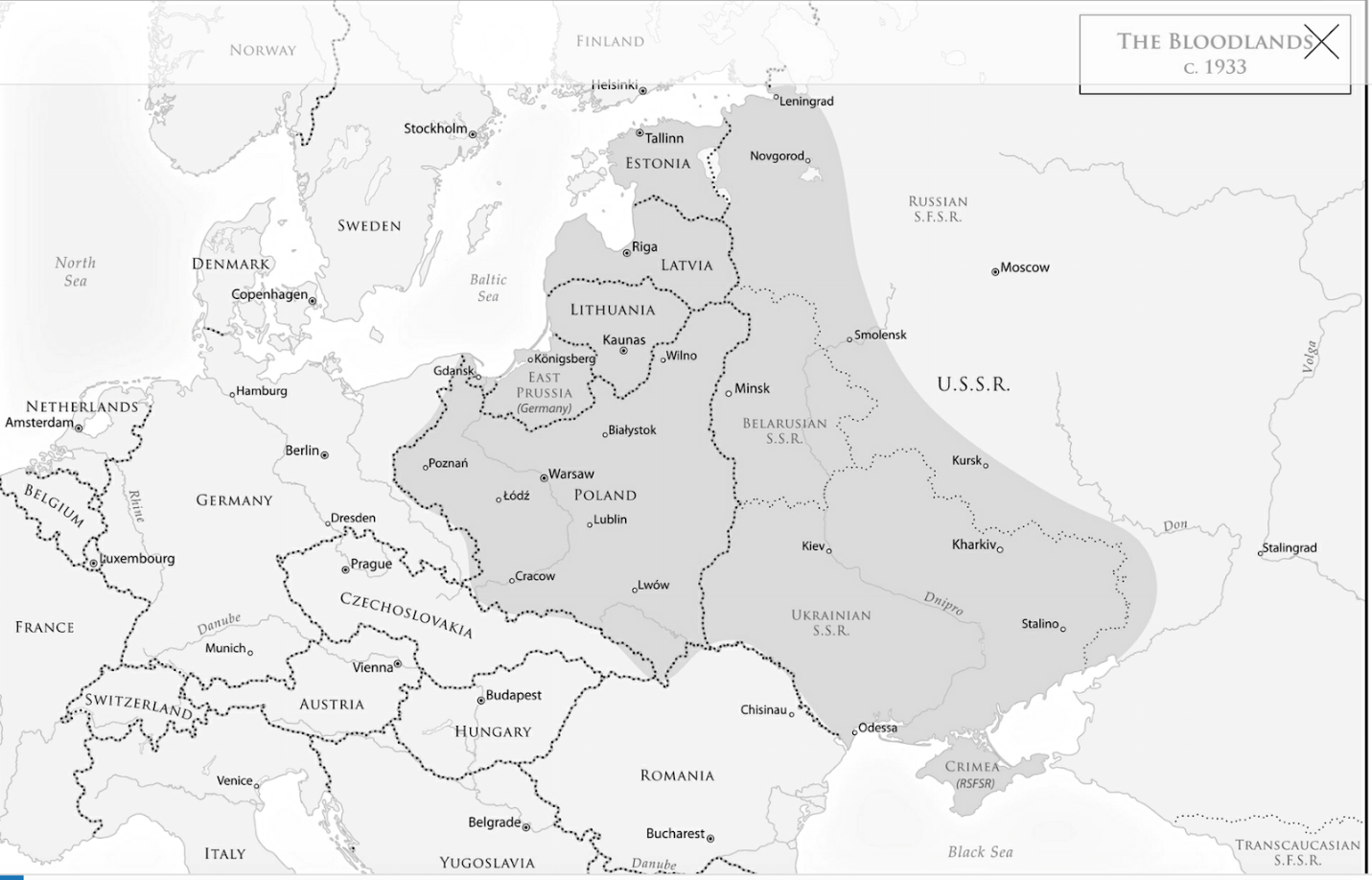

It’s probably one of the saddest and most disturbing things you can ever read, and it discusses what happened in this part of the world. Here’s a map that shows, roughly speaking, the area that historically Russia has always been concerned about.

Its western borderlands, and historically the Russians and the Germans in particular, have fought back and forth over these territories going back to the period of the Teutonic Knights in the Middle Ages. And one of the most terrible incidences of this whole thing was after Stalin and basically the Soviet Union came into existence, one of the things that Stalin realized was that he had to bring the Ukrainians to heel because they, even then, thought of themselves as not being Russian.

They thought of themselves as being Ukrainian, and they didn’t want to be under Moscow’s heel. They were happy to be part of the communist movement but they wanted their independence. Well, Stalin engineered a terrible, terrible famine called the Holodomor in the Ukraine, which killed over 12 million people. This happened in the decade before World War II in which the Nazis rolled over the Ukraine completely wiped out large swaths of the population. Again, millions and millions died. It was the site of many of the most bitter battles of World War II. So this particular patch of land has suffered just unbelievably in the last 100 years. And that is one of the reasons, I think, why the Ukrainians are so adamant that they will not accept this and that they will fight to the death basically to end up under Russia’s heel again.

Now, that’s just me jamming as a historian. I’ve been thinking about it constantly for the last 72 hours and I just had to share it with you. Now, what’s going on in the markets in response? Well, first thing I want to throw at you is kind of a funny little thing. Everybody talks about bitcoin and cryptos as being digital gold, as being safe havens. Forget that. Look at this chart:

This is what’s happened to bitcoin since the situation really ratcheted it up. Gold has been in an uptrend. On the other hand, bitcoin has just taken a huge dive. Palladium, as I mentioned earlier, has been up. So that just goes to prove, folks, I’ve become more and more convinced that I’m going to let my freak flag fly when it comes to crypto. I do not buy the crypto hype. I do not support them as investments and in a future video I will tell you why I believe that.

Going on to other impacts, Russia is well and truly… I won’t use the F word, but that’s pretty much where it is. This is the main Russian stock market index:

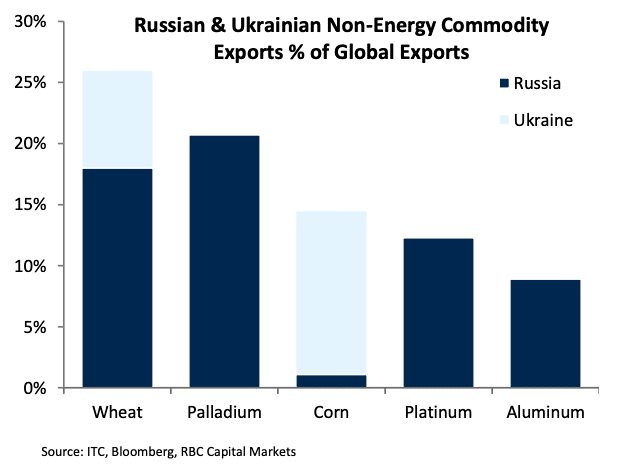

That is catastrophic. They are now below where they were at the beginning of the COVID crisis. So clearly the Russian oligarchs who are really the base of Putin’s support… In other words, he governs on behalf of a class of mega-rich Russian tycoons who got rich by picking at the remains of the Soviet communist state and all their economic assets. They are going to be hammered extremely hard. So that’s going to be an interesting thing to watch. But so are commodity markets. Here’s a chart that shows the Russian and Ukrainian non-energy commodity exports as a percentage of global exports of those commodities:

Between the two of them, Russia and Ukraine account for more than 25% of global wheat exports. Russia produces over 20% of palladium, as I argued last week. Ukraine itself, a major producer of corn. Platinum and aluminum, both major outputs of Russian mines. Now, what that means is, and I’m going to be speaking about this with my colleague Clint Lee next week, is that this is going to be a major, major thing to watch what happens to commodity markets for two reasons. One is obviously it’s going to present some opportunities. Maybe investing in commodity producers who benefit from these price rises. But on the other hand, it’s going to raise global prices for reasons that have nothing to do with interest rates and it’s also probably going to end up slowing the global economy. So we’re heading into a situation that I talked about a couple of weeks ago where the Federal Reserve is going to be raising interest rates going into a global slowdown caused by exogenous factors. That is the most dangerous scenario you can have for the economy, because if you’re raising interest rates to try to combat inflation, you’re trying to slow down the economy.

But if the economy is being slowed down by something else like a war in Europe and prices are going up because supply is affected by that, you can’t win, basically. And I think that’s going to be a big topic of discussion at the Federal Reserve bank this week, I predict. Now, what are likely further actions and what could that do to markets? Well, one thing a lot of people have talked about is cutting off Russia from the Swift system. The Swift system is a bank interchange system that allows, for example, me in South Africa… I was sending money from my US accounts to South Africa while I was there last three weeks. You use the Swift system. You enter Swift codes to identify the local banks. It’s run by an institution in Brussels that’s controlled by the world’s banks.

If Russia were cut off from this it would be impossible to send money in and out of Russia, at least to Western countries, at all. So in other words, Russia would not be able to bring money in and people would not be able to send money to Russia, for example to pay for natural gas or for petroleum or for oil or for any of the other major things that people buy from Russia including wheat, corn, et cetera. Now, if that would happen, that would essentially isolate Russia and leave them with no other option but to deal exclusively with other countries like China and others that have signed on to their own internal transfer system or interbank transfer system that they’ve developed. But if that were to happen, basically that would mean that the entire European energy economy would have to be completely cut off from one of its major sources of supply. Russia supplies something like 64% of the natural gas used in Europe, and that would end up causing an increase in natural gas prices and oil is not just temporarily but permanently.

For as long as Russia was locked out of the global payment system nobody could buy their products, which of course would devastate the Russian economy, make it impossible for them to continue their military activity, and basically force them to stop everything. But that would mean that gas and oil and other prices would go up to the extent that the global economy would go into an immediate horrific recession. So here you see this is the problem. This is a globalized economy. We’re all stuck in this together. So essentially we’re looking at a situation where, if you can imagine the analogy, it’s as if Hitler invaded Western Europe, France, the low countries, Norway, all the things that he did in May 1940, and yet the rest of the world kept trading with Germany simply because they had no option. Because if they didn’t trade with Germany, their economies would collapse.

Well, that’s the situation we’re now in the 21st century, folks. We have to continue this. And I can’t think of anything works, because if you don’t have the option of that kind of sanction to stop this sort of thing, what’s your other option? You go to war. But you can’t go to war with Russia because they’ve got nukes. So this is not a situation that is going to go away anytime soon. And with that in mind, let’s look at what happens or tends to happen in stock markets in situations like this. Here’s a chart that our new senior managing editor, Matt Collins, shared with me the other day.

It shows that during all major crises going back to the ’60, there is an initial pullback in the stock market but it doesn’t last. You can see the Vietnam War, the Gulf War, the Afghanistan War, the Iraq War, the Crimean Crisis. There’s an initial pullback in the early days of the conflict but then market bounces back. And buying the dip, which I predict we’re going to see… In fact we started seeing it yesterday on Thursday’s trade. While I was flying over Greenland and Iceland and all these other places on the way home I was watching markets. And initially there was this huge sell off, but then later in the day you began to see big buyers coming in and buying huge chunks of stocks that had been beaten down precisely because they’ve seen this chart or variations of it basically showing that panicking on the first day of a war is not a good thing to do because basically they are going to bounce back. Now, the one difference of course was the performance of the stock market after the Afghan War, and that’s because of the collapse of the dot com boom, which happened a little bit before that.

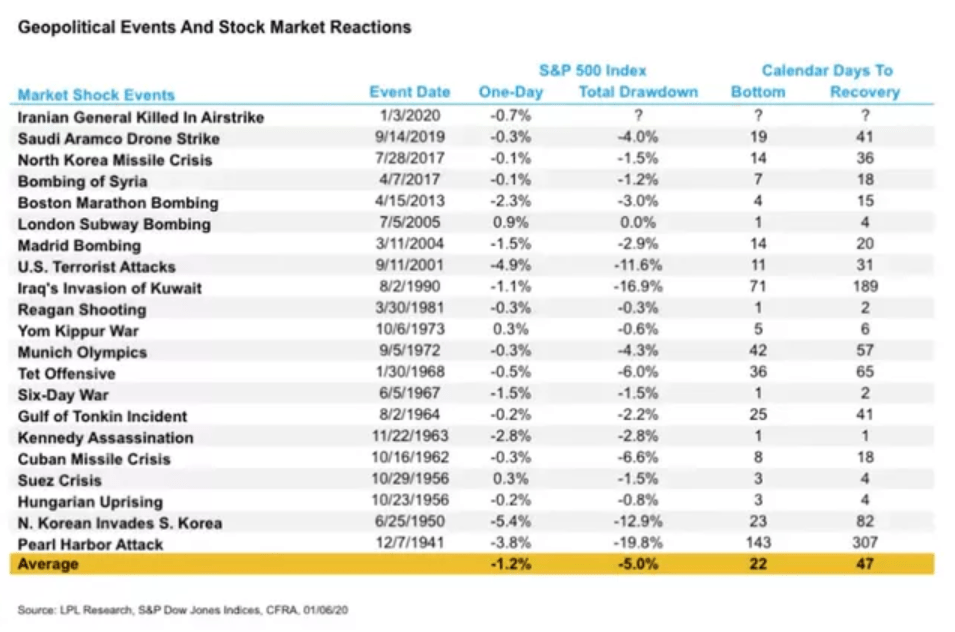

And the market was already declining but you can see that dip, and it did recover. So there was a big opportunity at the bottom of that dip to make some money in stocks. Now, here’s a chart that shows geopolitical events and market reactions.

It shows how many days on average it takes for the market to go to a bottom after a major geopolitical event, and then the days it takes to recover back. The average is 22 days to the bottom, the average total drawn is 5%, and the days to recover is about 47%. So here’s the thing: We could face another couple of weeks of drawdowns, and essentially that could lead to opportunities to buy at even better prices than we’re seeing now. But in a little over a month from now, historically speaking, we should end up seeing the market come back up.

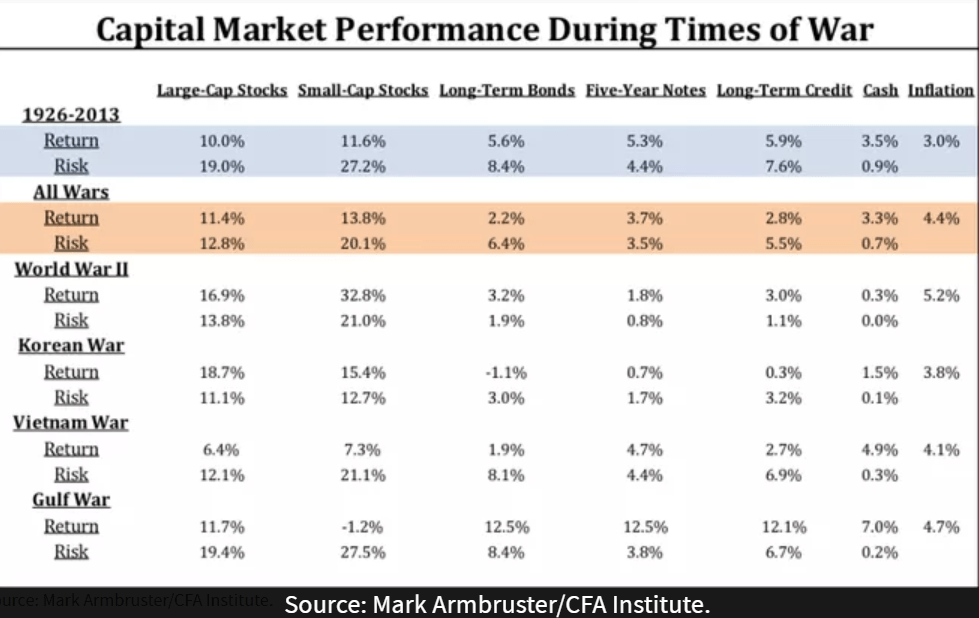

Now, the one example that doesn’t correspond to that is Iraq’s evasion of Kuwait in 1990. You can see it took 189 days to recover, but that’s because it happened in the middle of the world’s oil patch. Of course, again, the Pearl Harbor attack is a bit of an outlier but the general trend is that markets fall quickly and then rebound very quickly. So I would encourage you to keep that in mind as you play the stock market. Here’s a last chart I want to show you that shows the average return and average risk premium of capital markets around the world going back to 1926.

The average return during normal periods is about 10%. That’s basically annual percentage. The average risk premium is about 19%. But look at during war periods, and that’s for large caps. The return is actually better during wars for both large cap and small cap stocks, and the risk premium is actually lower than it is at normal times.

Why would that be? Well, I think the main thing is that what markets hate is uncertainty. When a war is expected and you don’t know when it’s going to happen, markets are uncertain and they sell off. Once the war starts, people know, well, there’s a war. And we know what countries are going to be doing. They’re going to be fighting the war. We know that fighting a war requires a lot of industrial production, and governments spend a lot of money on things which is generally good for business and good for the stock market. And so therefore the uncertainty is removed, the risk premium falls paradoxically during a war, and you make more money in stocks. Now, obviously that is not the case for countries that are losing wars.

But obviously at this point there’s no question that the United States and the other major Western powers at this stage, unless things go to horrific levels involving nukes and all of that, God forbid, we should actually ride this out I think, at a stock market level, very well. Again, I can’t repeat enough: That is not me, that I am laughing all the way to the bank at the expense of Ukrainians. I am personally horrified. If I could fly a Ukrainian flag I would simply because I feel that nobody, nobody deserves to see the images that were flashed yesterday around the internet of Russian helicopters going over civilian areas and civilian cities, firing rockets into buildings. And basically that is not acceptable under any circumstances.

Nevertheless, I’ve told you a couple of opportunities to look out for. On Monday, Clint Lee and I will go in depth to talk about some of the commodity plays. And some of them are commodity plays you would never imagine. There are things that come out of Ukraine and areas nearby like Belarus that nobody knows, and they could have major impacts on global stocks. Anyway, that’s me signing off. I hope things go better for the world over the weekend. If not, I’ll talk to you on Monday with Clint Lee and next week on Friday. Bye-bye.

Kind regards,

Ted Bauman

Editor, The Bauman Letter