Risk versus reward is a concept that I am constantly pushing on my 7-year-old son. I think it’s a vital process in any decision we make in life.

And when it comes to investing, this is one of the most important thought processes you must go through.

For every trade you make and every dollar you invest, you should know what your risk is and what your target reward is.

I’m not talking about one-off, lucky trades that explode higher … but a realistic expectation of the reward you’re after.

The goal here is to never risk more than your expected reward.

And as long as you find trades where your reward exceeds the risk, there are opportunities worth taking.

I have such an opportunity for you today…

High Risks

In May 2015, I warned that it was not the time to own high-yield debt.

A high-risk company’s debt has high yields because the company may not have the funds to repay its bonds when they come due.

The Federal Reserve was in the process of raising interest rates then, and owning debt that had been in a strong rally was not a good idea.

I reiterated that call in October 2015, stating that high-yield bonds were still not worth the risk.

And I was right.

Take a look at when I made those calls (highlighted in yellow):

After I warned about the risk in May 2015, high-yield bonds, as tracked by the iShares iBoxx $ High Yield Corporate Bond ETF (NYSE Arca: HYG), tumbled more than 15%.

And today I am warning you again — you do not want to own high-yield debt.

Low Rewards

Much like back in 2015, the high-yield debt market simply doesn’t offer you an adequate risk-versus-reward scenario.

That’s because during 2016, high-yield debt made a comeback as prices rose and yields declined even further. This inverse relationship between yields and prices is critical to understanding why you don’t want to own high-yield debt today.

When dealing with high-yield debt, your risk is that the company will struggle to repay its bonds. The yield on the bonds should be adequate to compensate that risk, so that if you own a portfolio of these bonds and some are not able to pay, the yield from the others offsets that risk.

Right now, the yield on HYG is about 5.25%.

If we extend that out to call it an average for the high-yield debt market … that’s extremely low.

Prior to this period of low interest rates that followed the 2008 housing crisis, high-yield debt ranged between 7% to 10% — nearly double where it’s at now.

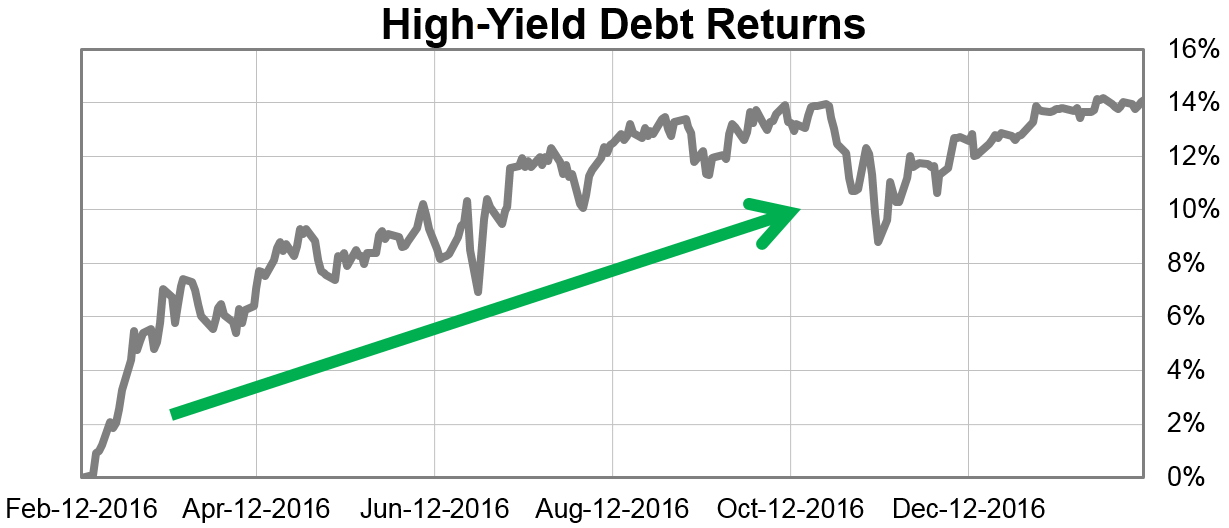

Take a look at the rally that high-yield debt saw in 2016…

There’s clearly some resistance that has slowed this rally at the 14% return mark. On HYG, that represents the $87.50 level.

If it can push through that level, bond prices could rise further … but their upside is capped due to the lack of reward being priced into these yields at the moment, and there isn’t much of a rally left.

Big Gains?

That’s why I’m expecting the opposite to happen.

From here, I could see yields nearly doubling — and that represents a downside opportunity of 20% or more.

Here’s how you can play it.

The ProShares Short High Yield ETF (NYSE Arca: SJB) is the inverse of the Markit iBoxx USD Liquid High Yield Index — the same index HYG is intended to replicate.

So as interest rates rise and that Markit iBoxx Index falls in value, SJB will rise in value.

This exchange-traded fund rose more than 10% from May of 2015 to early 2016. During this same time frame, the S&P 500 tumbled 13%.

So it offers a nice diversification to your portfolio … and now is the ideal time to own it.

Regards,

Chad Shoop, CMT

Editor, Pure Income