Yesterday, President Biden announced a ban on Russian oil imports to the U.S.

The announcement boosted oil prices, now up a full 70% per barrel since the start of the year.

But what if that’s only the beginning?

Russia’s deputy prime minister warned that taking his country’s oil off the global market could send prices soaring to “$300 a barrel if not more.”

That would be another 127% increase from today’s price.

The same official went even further, threatening that Russia would respond to an oil embargo by cutting off the supply of natural gas to Europe entirely.

It’s just another escalation in the biggest supply-side shock to commodities we have seen in a generation.

The whole world is on edge, and one man appears to hold all the cards on the supply-side of the equation. And if Russian President Putin decided to follow through by withholding vital energy supplies, the impact would be felt immediately.

But what if the ascent in oil prices was stopped in its tracks?

Little attention has been levied to the demand side, where another man is about to slam on the brakes.

Sowing the Seeds of Demand Destruction

Federal Reserve Chairman Jerome Powell will take center stage with next week’s Federal Open Market Committee meeting.

Inflation is the central bank’s top concern, and the forces driving the Fed to act are only getting worse.

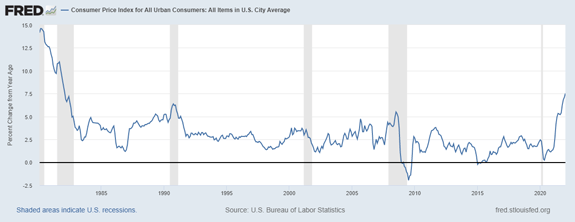

The surge in energy prices will surely accelerate the pain. This Thursday’s report on consumer price inflation is expected to show an increase of 7.9% compared to last year … the highest level in 40 years.

(Click here to view larger image.)

But that’s just for the month of February, meaning that it doesn’t really show the full impact of the unfolding energy crisis in Europe.

Not only that, but nonfarm payrolls jumped 678,000 in February … crushing expectations. So the Fed likely won’t be concerned about the current strength of the labor market.

That’s why strategists at Goldman Sachs and Bank of America have stuck by their call for as many as seven rate hikes just this year … despite the events unfolding on the global stage.

Here’s why they’ll be right and what it means for oil prices.

History Will Rhyme Again

Throughout history, the Fed has shown they will go to great lengths to tame inflation … even if that means torpedoing the economy along the way.

In order to stamp out price increases that built up in the 1970s, Paul Volcker hiked short-term rates from 9% to 19% in only six months … tipping the economy into recession and triggering a collapse in oil prices.

From 2004 to 2006, the Fed raised rates 17 times to cool off a red-hot housing market. The calamity that followed triggered the 2008 financial crisis. It also led to an unprecedented plunge in oil prices, which fell 74% in just six months.

This time will be no different if the Fed follows through as expected.

So, while the supply shock will support energy prices in the near term, eventually the weight of higher interest rates threatens to sink the economy and destroy demand for oil along with it.

Best regards,

Clint Lee

Research Analyst, The Bauman Letter

{kind=link}