Some things never change…

Mortgage fraud and lax lending standards helped spur the 2008 financial crisis. Remember the infamous NINJA loans of the era (as in “no income, no job or assets”)?

Like a bad horror movie, they’re baaack.

A decade after Lehman Brothers went bust, mortgage application fraud risk jumped 12.4% so far in 2018 compared to year-ago levels, say researchers at CoreLogic.

s

And the firm’s national mortgage application fraud index — which had been going sideways from 2011 through mid-2016 — recently hit a new record for this decade.

But unlike the pre-financial crisis era (stoked largely by brokers and lenders content to look the other way), today’s mortgage fraud comes with a twist.

Fake It to Make It

The first clue comes from a site recently shut down by investigators at the Federal Trade Commission (FTC): FakePayStubOnline.com.

The same guy who ran that site, said the FTC, also operated a host of other sites. They offered not just convincingly real pay stubs, but tax forms and bank statements (as well as “job verification services” that added yet another layer of fake proof if a lender needed more information).

A second clue comes from Fannie Mae. Earlier this year, the agency’s fraud investigators found a disturbing three-year trend: Dozens of employers kept popping up on an untold number of mortgage applications it reviewed in the Los Angeles area. Those employers turned out not to exist.

In August, the agency found nearly a dozen more potentially fake companies for San Jose area mortgage applications.

If it’s a major thing in California for the last three years, can the rest of the country be far behind?

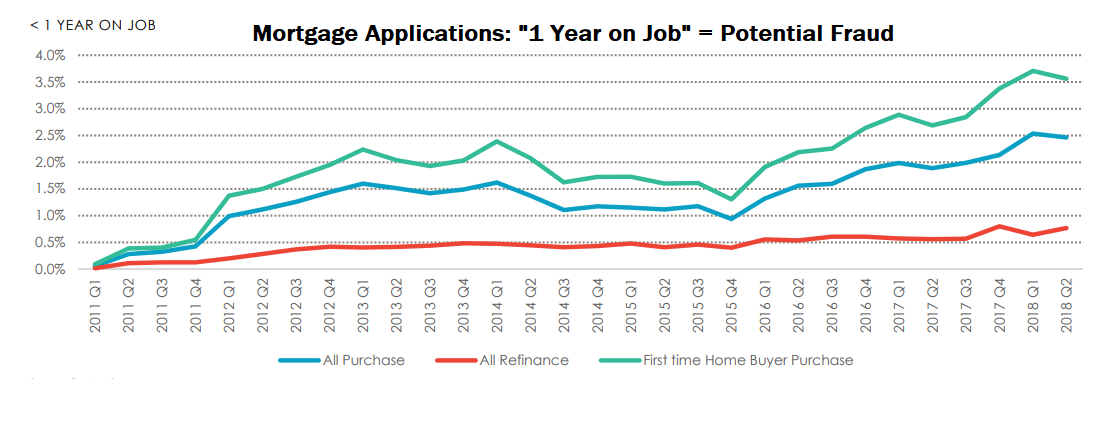

The third clue comes from CoreLogic’s researchers, who noted an interesting but obscure statistical trend: About 3.5% of mortgage applicants these days say they have one year or less on their current job — up from almost nil back in 2011.

(Source: CoreLogic)

Why’s that a big deal?

Figuring out Mortgage Fraud

It turns out the “one year on the job” mortgage application trend fits the typical fraud profile.

The applicant either has a new job (with the applicant giving himself a big fake pay raise from what he earned previously), or a supposedly high-paying first job out of college.

Either scenario, as CoreLogic points out, conveniently “removes the option for the lender to validate the income with the IRS.”

The scary thing? The FTC may have shut down FakePayStubsOnline.com. But if you search on Google, you find no shortage of firms offering to generate the same kinds of fake documents for a $5 fee.

Just fill in your personal info, a fake employer and a nice, big fake pay raise, and presto! The sites will even figure out your yearly earnings to date and other pesky calculations so it all looks legit.

White-Collar Crime

The big question is whether the rising levels of mortgage fraud are something that could actually sink the economy, like in 2008.

Aside from CoreLogic’s report, there’s not much else to go on. While the FBI continues to make plenty of arrests for this kind of white-collar crime, the last time the Bureau issued one of its voluminous “Year in Review” reports on mortgage fraud was in 2010.

But the current situation in Canada might give us a clue. Last year, investors in a Canadian lender, Home Capital Group, rushed to pull their deposits after the lender failed to disclose falsified mortgage applications.

And perhaps more ominously, S&P Global Ratings recently lowered a key measure of risk for Canadian banks “due to evidence of residential mortgage fraud … which could compound existing risks from the country’s hot housing market.”

Kind regards,

Jeff L. Yastine

Editor, Total Wealth Insider