The Nielsen Effect

For decades, Nielsen (NYSE: NLSN) ratings were the gold standard in traditional TV viewership and ratings. While TV is no longer traditional, Nielsen still knows its target audience and what ads best suit that audience.

And Roku (Nasdaq: ROKU), the king of the streaming TV market, just made a very important deal with the former TV champ.

Back in February, Macquarie analyst Tim Nollen discussed Nielsen’s role in the new Connected TV (CTV) market with Investor’s Business Daily. According to Nollen, Nielsen was developing CTV audience measurement and advertising tools.

The mention came at the end of a long interview on consolidation in the TV ad business and how ad spending was shifting toward CTV and away from traditional broadcast and cable TV markets.

Having a new set of tools for CTV is critical, according to Nollen:

It looks like Roku agreed on both the consolidation and the need for CTV ad tools. This morning, the streaming giant purchased Nielsen’s Advanced Video Advertising unit for an undisclosed amount.

Now, you might ask: Mr. Great Stuff, what’s so special about an old-world TV advertiser? Why would Roku be interested?

And you’d have a fair point … if we were only talking about TV ratings. But we’re talking about ad revenue. And the better you can target specific audiences with specific ads, the more you can charge for those ads.

Nielsen’s Advanced Video Ad unit specializes in something called dynamic ad insertion (DAI). To put it simply, DAI will allow Roku to scan and replace ads in streaming feeds with specifically targeted ads at the household level.

This is something that cable and broadcast TV operators would die for since it’d allow them to jack up the price of ads across the board and significantly increase revenue. But they don’t have DAI, and due to technology constraints, they never will.

This is what Roku and connected streaming TVs bring to the table.

But I hate commercials … with all the drugs and the side effects and the stuff I’ll never use!

Well, the good news is that, on Roku with DAI, you probably won’t see those Xeljanz ads anymore unless, you know, you’re in that target demographic. (*Warning: Take as directed. If Xeljanz starts to smoke, back away slowly and get help. Do not taunt Xeljanz.)

In addition to purchasing the DAI tech and Nielsen’s Advanced Video Ad unit, Roku also entered into a multiyear deal for inclusion in Nielsen One, a cross-media measuring solution.

In short, Roku just acquired the tools to specifically target streaming viewers with personalized ad content. This personalization will allow Roku to attract more CTV advertisers, charge more for targeted ads and bank even more revenue.

To put this deal in perspective: You know how Google became the king of online advertising by using your search data to offer up ads specific to you personally? DAI will allow Roku to do the same with CTV streaming.

Yes, I’m actually comparing Roku to Google. In fact, Roku is fast becoming the Google of the CTV streaming market. And if that doesn’t spark joy for ROKU bulls, I don’t know what will … other than this quick word from our sponsor!

Editor’s Note: Bigger than artificial intelligence, 5G and cybersecurity … COMBINED!

While electric vehicles are making the headlines, no one is talking about an even bigger mobility story: “MaaS.” A recent study predicts the fast-emerging $70 billion “mobility as a service” technology will blossom into a $1.8 trillion industry by 2028.

And one company that’s critical to this industry could emerge as the biggest winner as this tech goes mainstream. For more details behind this developing opportunity, click here now.

Good: To Everything, Zoom, Zoom, Zoom…

Many uncertainties surround the work-from-home market and the pandemic, but one thing is for certain: Zoom Video Communications (Nasdaq: ZM) absolutely crushed it in the fourth quarter.

Earnings surged to $1.22 per share, blowing past expectations for $0.87 per share. Revenue rocketed 369% to $882.5 million on the quarter, with full-year revenue up 326%.

Customers with more than 10 employees were up 33,400 at 467,000. Zoom also added 355 enterprise clients for a total of 1,644 — those are customers with annual revenue above $100,000. Even users on the cloud-based Zoom Phone platform spiked 269% to 10,700.

The video conferencing juggernaut went on to put current-quarter guidance ahead of Wall Street’s targets by about $100 million on revenue and $0.23 per share on earnings.

So, why did ZM’s early 7% rally fizzle out?

Because investors are concerned that this growth won’t hold up in a post-pandemic world. Sure, Zoom is knocking it out of the park right now. But what happens when the lockdowns end? What happens when everyone returns to the office?

Zoom will likely maintain its dominance in the videoconferencing market … but how big will that market be once everyone’s close enough to walk into the conference room or eager to take that company trip cross country?

That uncertainty, combined with a healthy dose of profit-taking, was more than enough to scuttle what was otherwise yet another stellar financial report from Zoom.

Better: Walmart Whacked

Stellar financial reports poured out onto the Street left and right today, and Target’s (NYSE: TGT) report is no different.

The company just posted a double beat, with earnings per share totaling $2.67, compared to expectations for $2.54. Revenue sprang up 21% to hit $28.34 billion, which topped analyst estimates for $27.48 billion.

It looks like a narrow beat, but 2020’s revenue growth (an insane $15 billion, all told) is greater than Target’s total sales growth over the past 11 years.

Wrapping up a killer holiday season, Target’s digital sales shot up 118% year over year and destroyed expectations — along with Walmart’s (NYSE: WMT) measly 69% digital surge. Comparable sales soared across every merchandise category.

That said … those year-over-year comparisons show a juiced-up Target propelled by pandemic shopping habits and a whole lotta stimmied-up spenders, which is far from Target’s normal environment.

Needless to say, Target gave no full-year guidance because — guess what? — consumer patterns are a little hard to predict right now. Though, management did lay out plans to blow a few billion opening new locations and remodeling others.

“Growth spending? We hate growth spending!” — Wall Street, probably. The stock rallied 3% before sinking 9% today after Target’s report came out. But, if the big red retailer’s current e-commerce dominance over Walmart continues, you can expect it to roar back from this slight setback.

Why? Because people buy TGT for much the same reason they shop at Target: It’s not Walmart.

Best: The Nio Style

Nio is “Best?” The stock fell nearly 10% today. How is that “Best?”

I know, right? I mean, Nio’s (NYSE: NIO) $0.14 per-share loss doubled the Street’s expectations for a loss of $0.07! Clearly, I must be joking.

But I checked with myself just to make sure … and nope, I’m not joking. I’d never lie to myself about money. Other things? Maybe. But not money.

You see, Nio did miss earnings expectations. But the real story is in the rest of the Chinese electric vehicle (EV) maker’s report. For one, revenue surged nearly 150% to $1.02 billion — beating the consensus estimate, too, I might add.

Furthermore, gross margins rose to 17.2%, up from -8.9% last year and 12.9% in the prior quarter. EV margin also climbed to 17.2% from -6% a year ago. Fourth-quarter deliveries spiked 111%. And Nio now sits on $6.5 billion in cash, nearly double its $3.3 billion hoard at the end of the third quarter.

And if that wasn’t enough, Nio expects first-quarter deliveries to land between 20,000 and 50,000 EVs — up 434% year over year and 18% from the fourth quarter. It also expects revenue to soar 451% from last year to reach between $1.13 billion and $1.16 billion.

I don’t know about you, but when stacked against all of those double- and triple-digit percentage increases, it seems kinda silly to smack NIO stock lower because earnings losses were higher than expected.

I mean, after all, Nio is a new and growing company. Clearly, that spending — while higher than expected — is paying off in spades.

Furthermore, remember that Nio is expanding into Europe this year. So, don’t be surprised if more spending is on the way. The bottom line here is that if you’re a NIO bull, these knee-jerk dips in the stock are going to be buying opportunities until Wall Street gets its head on straight.

So, how about those, um … checks notes … Golden Globes this weekend?

Did any of you tune in on Sunday? Anyone? Am I the only one who had no idea these were on, to begin with? (Also, drop me a line here so I don’t just ramble into the void.)

I know some of you might think: TV awards? In my Great Stuff?

It’s more likely than you think because this ain’t our first award show rodeo around here. We’ve long covered their slow, gasping demise … along with the rest of cable TV (see above). And it’s not just because this gives me another chance to profess my love for streaming; that’s a bonus.

Ratings are in for the most recent Golden Globe ceremony — the first virtual one, might I add, pandemic-prompted pajamas and all. Overall viewership was no bueno, dropping 70% for a record low of just 5.4 million viewers.

Frankly, our Quote of the Week should surprise absolutely none of you (I hope).

Sure, you could argue that watching the Golden Globes take place over Zoom was a mitigating factor in the poor ratings, and I agree. But the not-so-gradual decline in award show viewership is more obvious with each passing year.

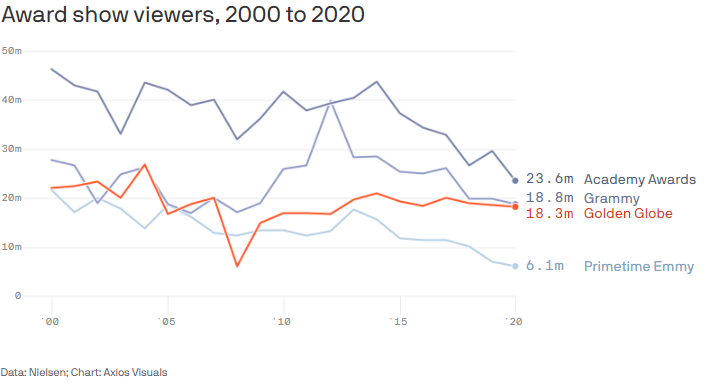

Here’s a visual for you. Bonus chart of the week, woot!

See the point where all four started to nosedive around 2013 or 2014? Right around the time that Netflix had cemented its digital dominance, Hulu started to threaten said dominance and the streaming floodgates were truly blown open?

Funny how that all lines up. These award shows are an artifact of another age — one that appreciated inauthentic back-patting and nepotism under a stale showbiz glamor veneer.

In the dark ages before on-demand TV and 2 million cable channels, there was literally nothing else on. And even once we got those 2 million cable channels … nothing else was on. Today, CTV and streaming prove that if you give us something even remotely interesting, we’ll watch anything over awards shows.

And check out that source tag in the chart: Nielsen data, once again. When it comes to the continued move away from cord-cutting, Nielsen’s data-sleuthing might, mixed with Roku’s convenience, will make one potently profitable pairing.

Anyway, I didn’t just come here today to beat the “cable is dead!” horse even further. I want your thoughts — your own individual experience, whether you’re an award show diehard or you cut the cable cord over a decade ago.

Do you have any interest in the dying embers of cable TV? Are you a fellow cord-cutter like us here at Great Stuff? Or hey, are you just around for the free streaming picks?

Write us at GreatStuffToday@BanyanHill.com with your own personal tales concerning cable cabals, TV withdrawals and all your sick ROKU gains, of course. You may just see your email in this Thursday’s edition of Reader Feedback!

Finally, remember what Mr. Great Stuff always says: Like Stuff? Share Stuff! So be sure to share ‘Stuff with your friends, family and everyone right down your email list. Send it all!

And don’t forget that you can always check out Great Stuff on the web (click here) or follow us on social media: Facebook, Instagram and Twitter.

Until next time, stay Great!

Joseph Hargett

Editor, Great Stuff