The market hammered oil in March, sending it 11% lower since the start of the year, while the rest of the market sits on gains.

To understand what’s going on in today’s oil market (and to suss out what will happen next), we need to go back a few years…

In 2014, most of the oil industry analysts got it wrong. The oil market is extremely complex and difficult to analyze. There are lots of moving parts, international influences and proprietary data that make the oil sector hard to predict.

And the largest unknown in the market continues to be Saudi Arabia.

Controlling the Flow of Oil

Saudi Arabia controls roughly 17% of the world’s oil production. For decades, the kingdom maintained a high oil price. It would reduce production when supply rose to keep the price up.

Back in April 2014, with the price of oil at $100 per barrel and heading higher, nobody predicted a crash. However, Saudi Arabia found itself in a bind. All those years of high oil prices nurtured new production all over the world. Oil that wasn’t economic to produce at $60, $70 or even $90 per barrel was making money with oil prices trading above $100 per barrel.

There is a lot of oil out there if the price gets high enough.

Saudi Arabia found itself fighting to maintain its market share and keep the price up. U.S. shale production flooded the market with high-quality crude oil, nearly doubling its 2008 levels. The U.S. was on track to become the world’s largest oil producer by 2015.

That was too much for the kingdom to stand. So when the opportunity arrived, it engaged in a little economic warfare.

In the summer of 2014, Chinese oil demand slowed. The industry looked up and realized that there was too much oil on the market. By December 2014, the price of oil fell 50%.

While U.S. shale production was prolific, it was also expensive. Companies tightened their belts and continued to drill, hoping Saudi Arabia would step in to correct the price. That was what the kingdom always did to protect oil prices.

That didn’t happen this time.

The Saudi Arabian Sucker Punch

Saudi Arabia acted quickly … but exactly opposite of what everyone expected. It lowered oil prices further by increasing production.

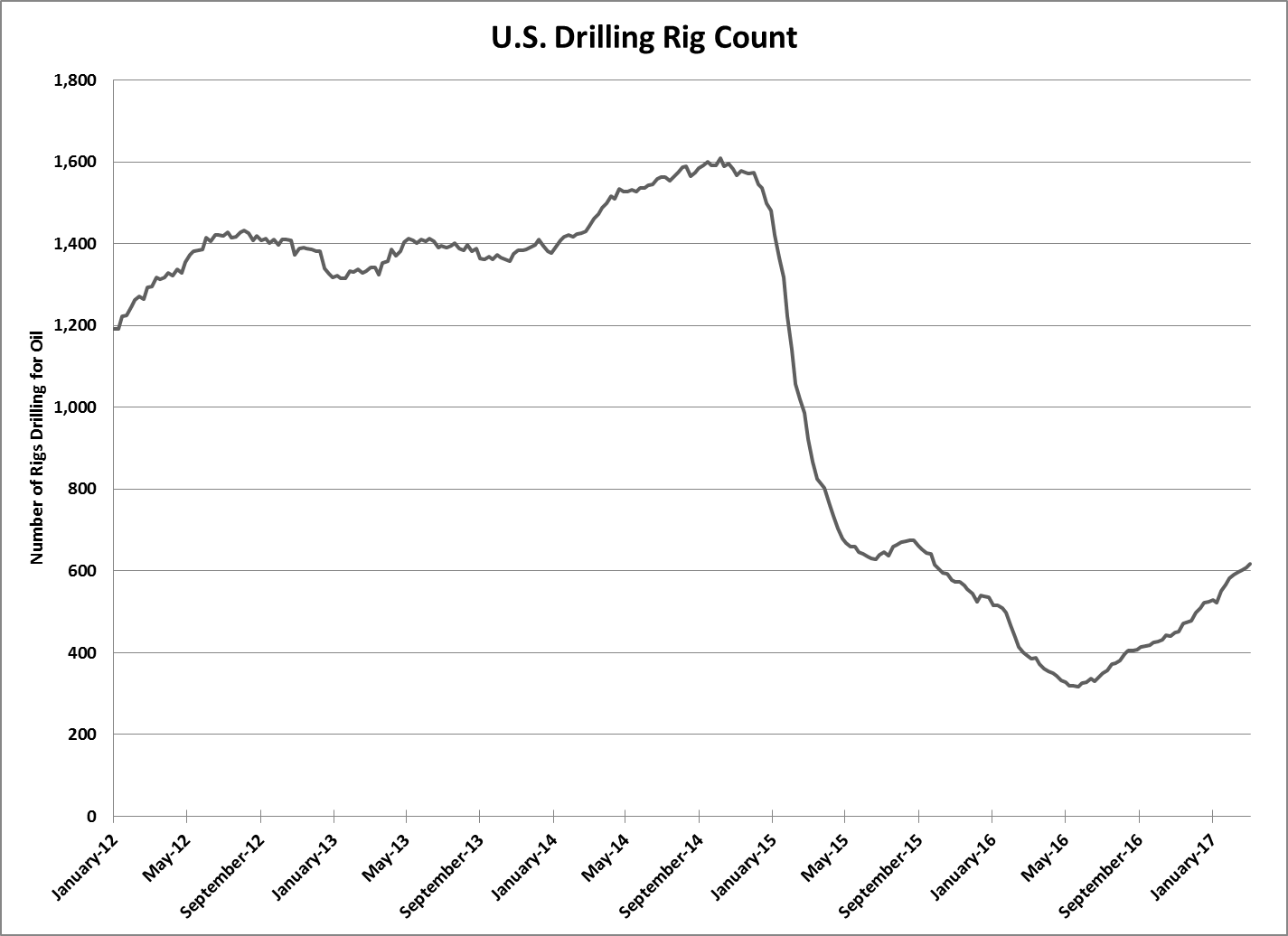

U.S. oil production peaked in May 2015 at 9.6 million barrels per day. By the end of 2015, oil prices had fallen another 50%, and the industry was in free fall. You can see what I mean by looking at this chart:

The number of rigs drilling oil wells collapsed. There were over 1,600 rigs drilling in October 2014, but there were just 316 by the end of May 2016. That’s an 80% cut in rigs.

The low oil prices crushed the industry, but not production. Companies had to continue to pump oil regardless of the cost just to keep cash coming in the door. It was a recipe for disaster.

By October 2016, 235 oil companies went bankrupt, and an estimated 350,000 jobs were lost in the oil industry. Another hundred companies sat on the brink.

Finally, by the end of 2016, Saudi Arabia and the other OPEC nations cut production. Oil prices stabilized around $50 per barrel. But that price makes it tough for Europe’s North Sea and Canada’s oil sands to produce oil profitably.

Tech Changes the Game

However, something funny happened in the U.S. during that period … a technological revolution of sorts.

You see, during the wild days of $100-per-barrel oil, shale wells weren’t efficient. They didn’t have to be. The wells produced such a gush of oil that they generated a ton of cash right away, and that forgives many economic sins.

When the price fell to $25 per barrel, it forced companies to cut everywhere. Drilling companies got leaner and cheaper. Service companies did too. Suddenly, the cost to drill a well was much cheaper, and fracking, or extracting oil and gas from rock by injecting high-pressure mixtures, also became less expensive.

In addition, some savvy engineers figured out that the old shale wells could be renewed. A shale well produces a lot of oil right away, then quickly dies — like a soda bottle that you shake before you open it. It turns out that if we refrack those wells, the production comes back, sometimes better than the original well.

U.S. oil production is back … if leaner than before. Companies are making money at $50 per barrel. That means we’ll see more oil supply weighing on the market, and U.S. shale production could ramp up quickly … even more than it did back in 2014.

Rising U.S. oil production is a problem for Saudi Arabia. The production cuts it put in place a few months ago are failing because the OPEC countries are cheating their quotas. Remember, countries such as Iraq and Iran get most of their cash from oil exports. As prices climb, it’s a huge temptation to sell just a little bit more. Pretty soon, the cuts aren’t quite as effective as they were.

That means there will be too much oil on the market by this summer … so oil prices will fall.

I expect to see oil prices head lower in the short term. It wouldn’t surprise me at all to see them drop to $40 per barrel. That means investors looking to add oil companies to their portfolios should hold off.

Good investing,

Matt Badiali

Senior Editor, Banyan Hill Publishing